Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- PetitionersspeechDokumen8 halamanPetitionersspeechAnirudh AroraBelum ada peringkat

- Respondents 1. The Representation of People's Act (Third Amendment) Ordinance 2014 Does Not Violate Art 14 of Constitution of IndiaDokumen7 halamanRespondents 1. The Representation of People's Act (Third Amendment) Ordinance 2014 Does Not Violate Art 14 of Constitution of IndiaAnirudh AroraBelum ada peringkat

- DdaDokumen2 halamanDdaAnirudh AroraBelum ada peringkat

- Respondents 1. The Representation of People's Act (Third Amendment) Ordinance 2014 Does Not Violate Art 14 of Constitution of IndiaDokumen7 halamanRespondents 1. The Representation of People's Act (Third Amendment) Ordinance 2014 Does Not Violate Art 14 of Constitution of IndiaAnirudh AroraBelum ada peringkat

- Well-Known TM Under Draft Trademark (Amendment) Rules, 2015Dokumen3 halamanWell-Known TM Under Draft Trademark (Amendment) Rules, 2015Anirudh AroraBelum ada peringkat

- Well-Known TM Under Draft Trademark (Amendment) Rules, 2015Dokumen3 halamanWell-Known TM Under Draft Trademark (Amendment) Rules, 2015Anirudh AroraBelum ada peringkat

- PetitionersspeechDokumen8 halamanPetitionersspeechAnirudh AroraBelum ada peringkat

- Imp Case Laws PDFDokumen6 halamanImp Case Laws PDFAnirudh AroraBelum ada peringkat

- Prevention of Corruption Act - Assana KumariDokumen4 halamanPrevention of Corruption Act - Assana KumariAnirudh AroraBelum ada peringkat

- Listening Sample Task - Plan Map Diagram LabellingDokumen3 halamanListening Sample Task - Plan Map Diagram LabellingAdhi ThyanBelum ada peringkat

- Eviction of Tenant On Non Payment of RentDokumen33 halamanEviction of Tenant On Non Payment of RentRahul BishnoiBelum ada peringkat

- Concepts in Disaster Management: Acec YashadaDokumen37 halamanConcepts in Disaster Management: Acec YashadamaheshBelum ada peringkat

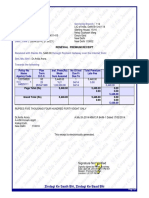

- Renewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchDokumen1 halamanRenewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchAnirudh AroraBelum ada peringkat

- PREVENTION OF CORRUPTION ACT - Assana KumariDokumen3 halamanPREVENTION OF CORRUPTION ACT - Assana KumariAnirudh AroraBelum ada peringkat

- 1062914 (1)Dokumen2 halaman1062914 (1)Anirudh AroraBelum ada peringkat

- Registration of TrademarkDokumen21 halamanRegistration of TrademarkAnirudh AroraBelum ada peringkat

- Applicability of Section 185 in The Companies ActDokumen9 halamanApplicability of Section 185 in The Companies ActdeepisainiBelum ada peringkat

- Disaster ManagementDokumen31 halamanDisaster ManagementAnirudh AroraBelum ada peringkat

- Certificate ColDokumen2 halamanCertificate ColAnirudh AroraBelum ada peringkat

- 11night LHR ZRHDokumen7 halaman11night LHR ZRHAnirudh AroraBelum ada peringkat

- Justice Through Mediation in IndiaDokumen11 halamanJustice Through Mediation in IndiaAnirudh AroraBelum ada peringkat

- Conflict AnirudhDokumen28 halamanConflict AnirudhAnirudh AroraBelum ada peringkat

- IprDokumen32 halamanIprAnirudh AroraBelum ada peringkat

- Clinical CoverDokumen8 halamanClinical CoverAnirudh AroraBelum ada peringkat

- Conflict AnirudhDokumen28 halamanConflict AnirudhAnirudh AroraBelum ada peringkat

- 1 PBDokumen9 halaman1 PBAnirudh AroraBelum ada peringkat

- Child Aduction: Conflict of LawsDokumen36 halamanChild Aduction: Conflict of LawsAnirudh AroraBelum ada peringkat

- Certificate ColDokumen2 halamanCertificate ColAnirudh AroraBelum ada peringkat

- Indian Express Newspapers ... Vs Union of India & Ors. Etc. Etc On 6 December, 1984Dokumen62 halamanIndian Express Newspapers ... Vs Union of India & Ors. Etc. Etc On 6 December, 1984Anirudh AroraBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Arroyo v. de VeneciaDokumen16 halamanArroyo v. de VeneciaNigel AlinsugBelum ada peringkat

- Administrative Circular Ej Vej SeminarDokumen2 halamanAdministrative Circular Ej Vej SeminarTess LegaspiBelum ada peringkat

- Tweets PDFDokumen181 halamanTweets PDFJaya KohliBelum ada peringkat

- Fernando vs. COADokumen7 halamanFernando vs. COAedelyn rivasBelum ada peringkat

- Pesca Vs Pesca G.R. No. 136921 Case DigestDokumen2 halamanPesca Vs Pesca G.R. No. 136921 Case DigestGringo BarrogaBelum ada peringkat

- US vs. Pedro Lahoylahoy, G.R. No. L-12453, July 15, 1918Dokumen4 halamanUS vs. Pedro Lahoylahoy, G.R. No. L-12453, July 15, 1918Kier Christian Montuerto InventoBelum ada peringkat

- This Confirms Receipt of Your Submission With The Following Details Subject To Validation by BIRDokumen1 halamanThis Confirms Receipt of Your Submission With The Following Details Subject To Validation by BIRPatrickHidalgoBelum ada peringkat

- Payroll FAQ For Santa EmployeesDokumen1 halamanPayroll FAQ For Santa EmployeesLeigh ScottBelum ada peringkat

- Sual, PangasinanDokumen2 halamanSual, PangasinanSunStar Philippine NewsBelum ada peringkat

- District Consumer Disputes Redressal Forum-I, U.T. ChandigarhDokumen3 halamanDistrict Consumer Disputes Redressal Forum-I, U.T. Chandigarhv_singh28Belum ada peringkat

- Snc. LEGAL ETHICS Case DigestDokumen22 halamanSnc. LEGAL ETHICS Case Digestnikol crisangBelum ada peringkat

- 60-Day Limited Period For Changes To Existing Elections Under The Federal Flexible Spending Account Program FSAFEDSDokumen4 halaman60-Day Limited Period For Changes To Existing Elections Under The Federal Flexible Spending Account Program FSAFEDSFedSmith Inc.100% (1)

- Anti Corruption Branch of Delhi Has Jurisdiction To Entertain and Act On Complaint Against Delhi Police Officer or Official Under Prevention of Corruption Act: Delhi HCDokumen37 halamanAnti Corruption Branch of Delhi Has Jurisdiction To Entertain and Act On Complaint Against Delhi Police Officer or Official Under Prevention of Corruption Act: Delhi HCLive LawBelum ada peringkat

- SIP1018 Kotak - CDRDokumen1 halamanSIP1018 Kotak - CDRNikesh MewaraBelum ada peringkat

- People v. CarlosDokumen4 halamanPeople v. CarlosRe doBelum ada peringkat

- Capital Insurance Vs RonquilloDokumen2 halamanCapital Insurance Vs RonquilloAnonymous 5MiN6I78I0Belum ada peringkat

- GWOP FormatDokumen7 halamanGWOP FormatSreenivasareddy TatireddyBelum ada peringkat

- Islamic Directorate of The Philippines v. CADokumen6 halamanIslamic Directorate of The Philippines v. CAbearzhugBelum ada peringkat

- People VS BatinDokumen2 halamanPeople VS Batinvincent nifas100% (2)

- Board of Trustees of University of Illinois v. United StatesDokumen4 halamanBoard of Trustees of University of Illinois v. United StatesScribd Government DocsBelum ada peringkat

- AP Creamy Layer InformationDokumen4 halamanAP Creamy Layer InformationSuji MudirajBelum ada peringkat

- UNITED STATES of America v. Dorothea DARAIO, AppellantDokumen16 halamanUNITED STATES of America v. Dorothea DARAIO, AppellantScribd Government DocsBelum ada peringkat

- Construing Urban Space As Public' inDokumen14 halamanConstruing Urban Space As Public' inArun FizardoBelum ada peringkat

- Case in Graft and Corruption G.R. No. 238815-WPS OfficeDokumen5 halamanCase in Graft and Corruption G.R. No. 238815-WPS OfficeJaneth RagasaBelum ada peringkat

- Robern Development Corp V People's Landless AssociationDokumen1 halamanRobern Development Corp V People's Landless AssociationLaura R. Prado-LopezBelum ada peringkat

- ADNM LAW UNIT 1 CASE Kriti PDFDokumen3 halamanADNM LAW UNIT 1 CASE Kriti PDFguytdyBelum ada peringkat

- Jain Chain v. ITODokumen14 halamanJain Chain v. ITOAvar LambaBelum ada peringkat

- The Laws of Cricket The Preamble - The Spirit ofDokumen3 halamanThe Laws of Cricket The Preamble - The Spirit ofapi-19711076Belum ada peringkat

- Simon Commission:: Nehru ReportDokumen3 halamanSimon Commission:: Nehru Reportsidikmailspronet100% (1)

- Organs of The United NationsDokumen8 halamanOrgans of The United NationsmosesalsBelum ada peringkat