Anda mungkin juga menyukai

- Section 58 in The Indian Partnership Act, 1932Dokumen2 halamanSection 58 in The Indian Partnership Act, 1932shivashankari86Belum ada peringkat

- PF DeclarationDokumen2 halamanPF Declarationshivashankari86Belum ada peringkat

- Pushpaka Loan Scheme PDFDokumen2 halamanPushpaka Loan Scheme PDFVeeru MudirajBelum ada peringkat

- Std02 III MSSS TM 3Dokumen9 halamanStd02 III MSSS TM 3shivashankari86Belum ada peringkat

- Pranav Kumar ScienceDokumen6 halamanPranav Kumar Scienceshivashankari86Belum ada peringkat

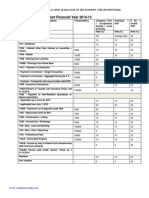

- Tds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #SimpletaxindiaDokumen11 halamanTds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #Simpletaxindiashivashankari86Belum ada peringkat

- Assessment of Charitable Trust and InstitutionDokumen51 halamanAssessment of Charitable Trust and InstitutionukalBelum ada peringkat

- Tnpsc+Group+IV 2008Dokumen15 halamanTnpsc+Group+IV 2008vinoknkBelum ada peringkat

- TNPSC Question OMR-ModelDokumen1 halamanTNPSC Question OMR-Modelshivashankari86Belum ada peringkat

- Budget 2014-15 Key Highlights-Income-Tax, Service Tax DownloadDokumen3 halamanBudget 2014-15 Key Highlights-Income-Tax, Service Tax Downloadshivashankari86Belum ada peringkat

- History 9 TNPSC Exam Question Answer Download ModelDokumen18 halamanHistory 9 TNPSC Exam Question Answer Download ModelMathan NaganBelum ada peringkat

- Tds Rate Chart Fy 2014-15 Ay 2015-16Dokumen26 halamanTds Rate Chart Fy 2014-15 Ay 2015-16shivashankari86Belum ada peringkat

- Regn. No.: The Employees' Deposit Linked Insurance Scheme 1976Dokumen2 halamanRegn. No.: The Employees' Deposit Linked Insurance Scheme 1976Tilak RajBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- TAX ProjectDokumen3 halamanTAX ProjectJames Ibrahim AlihBelum ada peringkat

- 0055450928Dokumen1 halaman0055450928chandramouliyadavBelum ada peringkat

- 5 Quezon City VS Abs CBNDokumen4 halaman5 Quezon City VS Abs CBNSuzyBelum ada peringkat

- Taguig City Ordinance No. 004-07Dokumen4 halamanTaguig City Ordinance No. 004-07henson montalvoBelum ada peringkat

- Special Journals - Quiz 36Dokumen8 halamanSpecial Journals - Quiz 36Joana TrinidadBelum ada peringkat

- AIRTEL Tariff Guide Poster A1Dokumen1 halamanAIRTEL Tariff Guide Poster A1KENNEDY MKBelum ada peringkat

- Payroll Dec With 13th MonthDokumen8 halamanPayroll Dec With 13th MonthchippaiUSABelum ada peringkat

- CTS, Neft, RTGSDokumen24 halamanCTS, Neft, RTGSSakthiBelum ada peringkat

- COP 6th RA PDFDokumen1 halamanCOP 6th RA PDFshahid alamBelum ada peringkat

- F6 PIT AnswersDokumen18 halamanF6 PIT AnswersHuỳnh TrungBelum ada peringkat

- PEZA NotesDokumen25 halamanPEZA NotesJane BiancaBelum ada peringkat

- GROUP 10 (Corporation Income Taxation - Regular Corporation)Dokumen16 halamanGROUP 10 (Corporation Income Taxation - Regular Corporation)Denmark David Gaspar NatanBelum ada peringkat

- CIR v. PLDTDokumen3 halamanCIR v. PLDTHoney BiBelum ada peringkat

- Benefits and Impact of The Proposed Tax Reform To The People and The GovernmentDokumen12 halamanBenefits and Impact of The Proposed Tax Reform To The People and The GovernmentGretchen CanedoBelum ada peringkat

- Od 329347391899682100Dokumen2 halamanOd 32934739189968210099rakeshghotiyaBelum ada peringkat

- Wirex Investment Opportunity 05042019Dokumen7 halamanWirex Investment Opportunity 05042019vsBelum ada peringkat

- Statement of Axis Account No:914010049504553 For The Period (From: 23-01-2019 To: 02-09-2020)Dokumen4 halamanStatement of Axis Account No:914010049504553 For The Period (From: 23-01-2019 To: 02-09-2020)Chandrani ChatterjeeBelum ada peringkat

- Hampton Machine Tool CaseDokumen7 halamanHampton Machine Tool CaseChaitanya80% (10)

- New Income Tax Calculator For Old & New Tax Regime For Salaried EmployeeDokumen4 halamanNew Income Tax Calculator For Old & New Tax Regime For Salaried EmployeeKiran KumarBelum ada peringkat

- Monthly Payroll Barangay OfficialsDokumen2 halamanMonthly Payroll Barangay OfficialsRosalie Sareno Alvior100% (5)

- Acct11 1hwDokumen3 halamanAcct11 1hwRonald James Siruno MonisBelum ada peringkat

- Contractor BillDokumen4 halamanContractor BillMuhammad RiazBelum ada peringkat

- Charitable Contributions: Publication 526Dokumen26 halamanCharitable Contributions: Publication 526jBelum ada peringkat

- Chaseo: Beginning BalanceDokumen1 halamanChaseo: Beginning BalanceAvalina LindaBelum ada peringkat

- Acct Statement - XX6782 - 23012024Dokumen5 halamanAcct Statement - XX6782 - 23012024Thejesh tejuBelum ada peringkat

- Syllabus - Law 129B Taxation 2 (Lucenario)Dokumen24 halamanSyllabus - Law 129B Taxation 2 (Lucenario)Renz RuizBelum ada peringkat

- NAME - PER - Unit 2: 8.4 Checkbook NotesDokumen3 halamanNAME - PER - Unit 2: 8.4 Checkbook Notesapi-556843268Belum ada peringkat

- CRN5594681450Dokumen3 halamanCRN5594681450amitdesai92Belum ada peringkat

- 2022 AllSlipsDokumen3 halaman2022 AllSlipsAshley LehmanBelum ada peringkat

- Payroll ExercisesDokumen1 halamanPayroll ExercisesMerry Grace EsquivelBelum ada peringkat