Anda mungkin juga menyukai

- South Asia Subregional Economic Cooperation: Trade Facilitation Strategic Framework 2014-2018Dari EverandSouth Asia Subregional Economic Cooperation: Trade Facilitation Strategic Framework 2014-2018Belum ada peringkat

- Yeow Teck Chai and Ooi Chooi Im - The Development of Free Industrial ZonesThe Malaysian ExperienceDokumen24 halamanYeow Teck Chai and Ooi Chooi Im - The Development of Free Industrial ZonesThe Malaysian ExperienceEileen ChuBelum ada peringkat

- Kastam FormDokumen2 halamanKastam FormSathyaRajan RajendrenBelum ada peringkat

- Taxation Suggested Solution: LessDokumen9 halamanTaxation Suggested Solution: LesskannadhassBelum ada peringkat

- IV. Tariff and Customs Code of 1978, As AmendedDokumen57 halamanIV. Tariff and Customs Code of 1978, As AmendedCarrie CrossBelum ada peringkat

- Appeal Tax Procedure (Malaysia)Dokumen2 halamanAppeal Tax Procedure (Malaysia)Zati TyBelum ada peringkat

- Import Duty Exemption GuideDokumen21 halamanImport Duty Exemption GuideThong Kin MunBelum ada peringkat

- Ba2463d Assignment2Dokumen36 halamanBa2463d Assignment2Aqilah PeiruzBelum ada peringkat

- CBW Handouts by Jimmy T. Maban II LCBDokumen38 halamanCBW Handouts by Jimmy T. Maban II LCBCorazon Ona100% (1)

- HRDF SchemeDokumen36 halamanHRDF SchemeLiza Liza ZahariBelum ada peringkat

- SPFSA - 2016 - I - Kertas - 8 - Pelaksanaan & Pengurusan Kontrak Konsesi Perkhidmatan Sokongan Hospital (BPK KKM)Dokumen22 halamanSPFSA - 2016 - I - Kertas - 8 - Pelaksanaan & Pengurusan Kontrak Konsesi Perkhidmatan Sokongan Hospital (BPK KKM)sufiBelum ada peringkat

- GST in MalaysiaDokumen15 halamanGST in MalaysiaIzzuddin YussofBelum ada peringkat

- Eo 463, 805, 160Dokumen8 halamanEo 463, 805, 160Chisa MamowalasBelum ada peringkat

- Guide For Business: Using The First Protocol: Go To For More InformationDokumen24 halamanGuide For Business: Using The First Protocol: Go To For More InformationTravis OpizBelum ada peringkat

- Week 5 Lecture Handout - LecturerDokumen5 halamanWeek 5 Lecture Handout - LecturerRavinesh PrasadBelum ada peringkat

- SENARAI KLINIK NUR SEJAHTERA LPPKN JOHOR DAN SELURUH MALAYSIADokumen12 halamanSENARAI KLINIK NUR SEJAHTERA LPPKN JOHOR DAN SELURUH MALAYSIAHwee Been TeoBelum ada peringkat

- Akta Eksais 1976Dokumen105 halamanAkta Eksais 1976KZ Hashim33% (3)

- For The Full Essay Please WHATSAPP 010-2504287Dokumen11 halamanFor The Full Essay Please WHATSAPP 010-2504287Simon RajBelum ada peringkat

- ASEAN 2025 Forging Ahead Together FinalDokumen136 halamanASEAN 2025 Forging Ahead Together FinalPortCalls100% (1)

- CustomsDokumen27 halamanCustomslorennethBelum ada peringkat

- Customs Legislation and Procedures Course Volume 1 Revised Final Version 2 - 2019Dokumen105 halamanCustoms Legislation and Procedures Course Volume 1 Revised Final Version 2 - 2019Memory Shonge RutsitoBelum ada peringkat

- Sindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFDokumen64 halamanSindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFrohail51Belum ada peringkat

- Petronas Approved Medical Examiner List 2017 (Latest Updated Version)Dokumen4 halamanPetronas Approved Medical Examiner List 2017 (Latest Updated Version)Zulfadli RaniBelum ada peringkat

- Basic Distinction in The Tax Treatment of A Resident or Non-Resident Individual Is As FollowsDokumen10 halamanBasic Distinction in The Tax Treatment of A Resident or Non-Resident Individual Is As FollowsGwen93Belum ada peringkat

- Eco 415Dokumen4 halamanEco 415Verne Skeete Jr.100% (1)

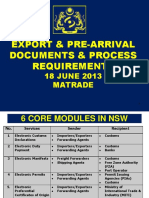

- EXPORT & PRE-ARRIVAL DOCUMENTS & PROCESS REQUIREMENTSDokumen30 halamanEXPORT & PRE-ARRIVAL DOCUMENTS & PROCESS REQUIREMENTSsubrascBelum ada peringkat

- Logbook Aisyah Athirah Abdul RazabDokumen28 halamanLogbook Aisyah Athirah Abdul Razabauni fildzahBelum ada peringkat

- Custom Degree ADokumen76 halamanCustom Degree Awengy044Belum ada peringkat

- Malaysia XportDokumen14 halamanMalaysia XportNoly IthninBelum ada peringkat

- Cottage Industries and VATDokumen8 halamanCottage Industries and VATAdib TasnimBelum ada peringkat

- Indian Business Environment Foreign Trade Policy of IndiaDokumen28 halamanIndian Business Environment Foreign Trade Policy of IndiaReshma RavichandranBelum ada peringkat

- RA 7844 Export Development Act of 1994Dokumen21 halamanRA 7844 Export Development Act of 1994Crislene CruzBelum ada peringkat

- Key Policy Areas That Can Spur Industrialization in KenyaDokumen4 halamanKey Policy Areas That Can Spur Industrialization in KenyaPaul MachariaBelum ada peringkat

- Malaysia Country Tax Guide 2012Dokumen18 halamanMalaysia Country Tax Guide 2012Nicholas AngBelum ada peringkat

- Chap II Foreign Trade PolicyDokumen13 halamanChap II Foreign Trade PolicyNitin SinghalBelum ada peringkat

- Overview of CCCIDokumen7 halamanOverview of CCCIMasood PervezBelum ada peringkat

- Forign Trade Procedure and DocumentationDokumen68 halamanForign Trade Procedure and DocumentationDinesh.KBelum ada peringkat

- CH 1 FocmpDokumen26 halamanCH 1 Focmpjemalseid241Belum ada peringkat

- Iii. Trade Policies and Practices by Measure (1) I: Mauritius WT/TPR/S/198/Rev.1Dokumen38 halamanIii. Trade Policies and Practices by Measure (1) I: Mauritius WT/TPR/S/198/Rev.1Nanda MunisamyBelum ada peringkat

- EcoZone TaxationDokumen10 halamanEcoZone TaxationjanewightBelum ada peringkat

- Foreign Trade Policy,: Export Promotion Schemes and Drawback (Impact of GST) ATDokumen25 halamanForeign Trade Policy,: Export Promotion Schemes and Drawback (Impact of GST) ATSATYANARAYANA MOTAMARRIBelum ada peringkat

- Business Regulations & Support SystemDokumen68 halamanBusiness Regulations & Support SystemAiniBelum ada peringkat

- India's Foreign Trade Policy 2015-20 AnalyzedDokumen5 halamanIndia's Foreign Trade Policy 2015-20 AnalyzedKartik KhandelwalBelum ada peringkat

- India's Foreign Trade Policy: Mba (Ib)Dokumen29 halamanIndia's Foreign Trade Policy: Mba (Ib)nithinsdnBelum ada peringkat

- Exim Policy: An Assignment Report OnDokumen13 halamanExim Policy: An Assignment Report OnRavi VermaBelum ada peringkat

- Export Development Act of 1994Dokumen6 halamanExport Development Act of 1994Pia Verna Irish ToraynoBelum ada peringkat

- The Role of Customs DepartmentDokumen19 halamanThe Role of Customs DepartmentMohd Zu SyimalaienBelum ada peringkat

- Department of Trade and IndustryDokumen47 halamanDepartment of Trade and IndustryCzerina Gene Dela CruzBelum ada peringkat

- Name - Adekunle Adesuyi MATRIC NO - 225724 Course Code - Mba 720 Course Title - Business Policy and Strategy AssignmentDokumen5 halamanName - Adekunle Adesuyi MATRIC NO - 225724 Course Code - Mba 720 Course Title - Business Policy and Strategy AssignmentRichard AdekunleBelum ada peringkat

- RA 7844 - Export Development ActDokumen6 halamanRA 7844 - Export Development ActMong AliBelum ada peringkat

- Year Book 2019 20Dokumen86 halamanYear Book 2019 20Muhammad AtifBelum ada peringkat

- SMEDA Business Guide Series: Procedure For Claiming Duty DrawbacksDokumen27 halamanSMEDA Business Guide Series: Procedure For Claiming Duty DrawbacksAnas AnsariBelum ada peringkat

- Group 5 Researrch ProposalDokumen20 halamanGroup 5 Researrch ProposalEnat EndawokeBelum ada peringkat

- Tax Audit Project Yuviy 190020045 MazarsDokumen17 halamanTax Audit Project Yuviy 190020045 MazarsChristinBelum ada peringkat

- Import Export ManagementDokumen130 halamanImport Export ManagementNishita ShahBelum ada peringkat

- Make in India 12BEI0044Dokumen27 halamanMake in India 12BEI0044Kunal KaushikBelum ada peringkat

- PolicyDokumen10 halamanPolicyadpBelum ada peringkat

- GENRALIZED Info For Epz in PakistanDokumen6 halamanGENRALIZED Info For Epz in PakistanAli AhmadBelum ada peringkat

- Comesa Investment OpportunitiesDokumen6 halamanComesa Investment OpportunitiesFeisal AhmedBelum ada peringkat

- Chapter 7 Business Regulation and Support SystemDokumen62 halamanChapter 7 Business Regulation and Support SystemMohd Fazri BanjarBelum ada peringkat

- Concept ProjectDokumen4 halamanConcept ProjectFatimah Abdul HamidBelum ada peringkat

- Study at Cardiff UniversityDokumen25 halamanStudy at Cardiff Universitycikfatimah92Belum ada peringkat

- Table of Content: No PagesDokumen2 halamanTable of Content: No PagesFatimah Abdul HamidBelum ada peringkat

- EXREC CLUB ORGANIZATION AND MEMBERS 2014Dokumen1 halamanEXREC CLUB ORGANIZATION AND MEMBERS 2014Fatimah Abdul HamidBelum ada peringkat

- FDokumen28 halamanFFatimah Abdul HamidBelum ada peringkat

- 01 Jolley Land Transportation SectorDokumen28 halaman01 Jolley Land Transportation SectorFatimah Abdul HamidBelum ada peringkat

- Agents Official DocumentDokumen15 halamanAgents Official DocumentFatimah Abdul HamidBelum ada peringkat

- Concept ProjectDokumen4 halamanConcept ProjectFatimah Abdul HamidBelum ada peringkat

- Teaching Plan - Jan 2013Dokumen6 halamanTeaching Plan - Jan 2013Fatimah Abdul HamidBelum ada peringkat

- ACADEMIC GUIDELINES SUBJECT REGISTRATION FEBRUARY 2014 SEMESTERDokumen3 halamanACADEMIC GUIDELINES SUBJECT REGISTRATION FEBRUARY 2014 SEMESTERFatimah Abdul HamidBelum ada peringkat

- Office Layout Floor Plan GuideDokumen1 halamanOffice Layout Floor Plan GuideFatimah Abdul HamidBelum ada peringkat

- Office Layout Floor Plan GuideDokumen1 halamanOffice Layout Floor Plan GuideFatimah Abdul HamidBelum ada peringkat

- QUIZ 2 (10%) - : INSTRUCTION: Answer ALL QuestionsDokumen1 halamanQUIZ 2 (10%) - : INSTRUCTION: Answer ALL QuestionsFatimah Abdul HamidBelum ada peringkat

- Time Table My ClassDokumen1 halamanTime Table My ClassFatimah Abdul HamidBelum ada peringkat

- Event Schedule Planner 2014Dokumen1 halamanEvent Schedule Planner 2014Fatimah Abdul HamidBelum ada peringkat

- Event Schedule Planner 2014Dokumen1 halamanEvent Schedule Planner 2014Fatimah Abdul HamidBelum ada peringkat

- Some People Says That Time Is MoneyDokumen1 halamanSome People Says That Time Is MoneyFatimah Abdul HamidBelum ada peringkat

- Elasticity CHP 4Dokumen37 halamanElasticity CHP 4Fatimah Abdul HamidBelum ada peringkat

- Bel 311Dokumen1 halamanBel 311Fatimah Abdul HamidBelum ada peringkat

- Male Breast Cancer Treatment Options ReferenceDokumen1 halamanMale Breast Cancer Treatment Options ReferenceFatimah Abdul HamidBelum ada peringkat

- 921 F.2d 1330 21 Fed.R.Serv.3d 1196, 65 Ed. Law Rep. 32: United States Court of Appeals, Third CircuitDokumen14 halaman921 F.2d 1330 21 Fed.R.Serv.3d 1196, 65 Ed. Law Rep. 32: United States Court of Appeals, Third CircuitScribd Government DocsBelum ada peringkat

- Anti Ragging NoticesDokumen3 halamanAnti Ragging NoticesAmit KumarBelum ada peringkat

- Administratrix's claim for rent denied as temporary license expiredDokumen6 halamanAdministratrix's claim for rent denied as temporary license expiredPutri NabilaBelum ada peringkat

- Laws Thermodynamics LectureDokumen7 halamanLaws Thermodynamics Lecturexx_aleksa_hrvatska_xxBelum ada peringkat

- Photometry Training EnglishDokumen79 halamanPhotometry Training EnglishkholisenangBelum ada peringkat

- Ramos v. CA - GR No. L-31897 PDFDokumen3 halamanRamos v. CA - GR No. L-31897 PDFLawrence EsioBelum ada peringkat

- Third Party Debt CollectionDokumen2 halamanThird Party Debt CollectionShannon Collum100% (14)

- Supreme Authority at Earth Law and Proclamation + Chief Justice Sharon Ann Peart JohnsonDokumen5 halamanSupreme Authority at Earth Law and Proclamation + Chief Justice Sharon Ann Peart Johnsonshasha ann beyBelum ada peringkat

- Income Tax ProclamationDokumen31 halamanIncome Tax ProclamationhenybamBelum ada peringkat

- Tiger Chicks (TA Progressive Poultry LTD) V Tembo and Ors (Appeal 6 of 2020) 2020 ZMSC 160 (23 December 2020)Dokumen45 halamanTiger Chicks (TA Progressive Poultry LTD) V Tembo and Ors (Appeal 6 of 2020) 2020 ZMSC 160 (23 December 2020)James ChimbalaBelum ada peringkat

- Alkalmazottáramlástan Week4 EngDokumen13 halamanAlkalmazottáramlástan Week4 EngTAWFIQ RAHMAN100% (1)

- Adan Salazar v. United States, 991 F.2d 786, 1st Cir. (1993)Dokumen6 halamanAdan Salazar v. United States, 991 F.2d 786, 1st Cir. (1993)Scribd Government DocsBelum ada peringkat

- 138 SandhyaDokumen13 halaman138 SandhyaS&S LegalBelum ada peringkat

- Eticket Receipt: Kaniti/Durga Srinivas MRDokumen2 halamanEticket Receipt: Kaniti/Durga Srinivas MRsri_dk12940% (1)

- Petition For A Decree of Nullity: Absence of Canonical FormDokumen1 halamanPetition For A Decree of Nullity: Absence of Canonical FormMelissa Benesisto CamposanoBelum ada peringkat

- State of Maine Rules of Civil Procedure For 2012Dokumen652 halamanState of Maine Rules of Civil Procedure For 2012Charlton ButlerBelum ada peringkat

- Fajardo acquitted of illegal possessionDokumen2 halamanFajardo acquitted of illegal possessionAlbert CaranguianBelum ada peringkat

- Human Rights AssignmentDokumen9 halamanHuman Rights AssignmentKriti KrishnaBelum ada peringkat

- Government of Andhra PradeshDokumen3 halamanGovernment of Andhra PradeshsatyaBelum ada peringkat

- International Labour Law Report on ILO Convention 187Dokumen17 halamanInternational Labour Law Report on ILO Convention 187Uday singh cheemaBelum ada peringkat

- Attempted Homicide Colinares vs. PeopleDokumen2 halamanAttempted Homicide Colinares vs. PeopleAubrey AquinoBelum ada peringkat

- Regulations of The UEFA Futsal Champions LeagueDokumen64 halamanRegulations of The UEFA Futsal Champions Leaguesebastian ferrer vargasBelum ada peringkat

- 88 Onslow Gardens Other-1434564Dokumen38 halaman88 Onslow Gardens Other-1434564Desmond WilliamsBelum ada peringkat

- Adams v. School Board of St. Johns County, FloridaDokumen150 halamanAdams v. School Board of St. Johns County, Floridastreiff at redstateBelum ada peringkat

- Ans 1Dokumen2 halamanAns 1bhupendra barhatBelum ada peringkat

- Astm D 4702 - 03Dokumen6 halamanAstm D 4702 - 03phaindikaBelum ada peringkat

- Photographer Terms and ConditionsDokumen9 halamanPhotographer Terms and ConditionsPaul Jacobson100% (1)

- REPUBLIC ACT NO. 7076 CREATES PEOPLE'S SMALL-SCALE MINING PROGRAMDokumen10 halamanREPUBLIC ACT NO. 7076 CREATES PEOPLE'S SMALL-SCALE MINING PROGRAMJey RhyBelum ada peringkat

- OMAN - New Companies Commercial Law UpdatesDokumen15 halamanOMAN - New Companies Commercial Law UpdatesSalman YaqubBelum ada peringkat

- 1 Garcia vs. Executive Secretary (GR No. 101273)Dokumen7 halaman1 Garcia vs. Executive Secretary (GR No. 101273)yra crisostomoBelum ada peringkat