Anda mungkin juga menyukai

- Mas Final Preboard Batch 90 PDFDokumen22 halamanMas Final Preboard Batch 90 PDFBinibining KoreaBelum ada peringkat

- Standard CostingDokumen14 halamanStandard CostingRoselyn LumbaoBelum ada peringkat

- (Set D) (MC) Chapter 19 - Cost Behavior and Cost-Volume-Profit Analysis Examination Question and AnswersDokumen2 halaman(Set D) (MC) Chapter 19 - Cost Behavior and Cost-Volume-Profit Analysis Examination Question and AnswersJohn Carlos DoringoBelum ada peringkat

- FMDokumen10 halamanFMKei YeeBelum ada peringkat

- Module 36.1 Quizzer 2 - Subsequent To Date of Acquisition: PendonDokumen3 halamanModule 36.1 Quizzer 2 - Subsequent To Date of Acquisition: PendonJoshua Daarol0% (1)

- Calculating variable and fixed costs for units producedDokumen12 halamanCalculating variable and fixed costs for units producedashibhallau100% (1)

- Quizzer-Cost-Behavior - Docx Regression Analysis Least SquaresDokumen1 halamanQuizzer-Cost-Behavior - Docx Regression Analysis Least SquareslastjohnBelum ada peringkat

- ConsignmentDokumen9 halamanConsignmentVishal GattaniBelum ada peringkat

- Mas 1.2.3 Assessment For-PostingDokumen7 halamanMas 1.2.3 Assessment For-PostingJustine CruzBelum ada peringkat

- PDF Document 3Dokumen13 halamanPDF Document 3Nina0% (1)

- Polytechnic University of The Philippines College of AccountancyDokumen11 halamanPolytechnic University of The Philippines College of AccountancyRonel CacheroBelum ada peringkat

- Absorption vs Variable Costing Activity 2Dokumen2 halamanAbsorption vs Variable Costing Activity 2Gill Riguera100% (1)

- Standard Costing and Variance Analysis ProblemsDokumen4 halamanStandard Costing and Variance Analysis ProblemsJoann RiveroBelum ada peringkat

- Ejercicio 1 - 2 Cost Accounting TuraboDokumen2 halamanEjercicio 1 - 2 Cost Accounting TuraboAnniehopelessBelum ada peringkat

- CF Quiz AprilDokumen5 halamanCF Quiz Aprilsumeet9surana9744100% (1)

- Job CostingDokumen19 halamanJob CostingSteven HouBelum ada peringkat

- Prelim Exam PDFDokumen6 halamanPrelim Exam PDFPaw VerdilloBelum ada peringkat

- Peter Senen overhead calculations and journal entriesDokumen5 halamanPeter Senen overhead calculations and journal entriesAccounting Files0% (1)

- Chap 8 Responsibility AccountingDokumen51 halamanChap 8 Responsibility AccountingXel Joe BahianBelum ada peringkat

- Advanced Financial Accounting Midterm: For Questions 2-4Dokumen13 halamanAdvanced Financial Accounting Midterm: For Questions 2-4Mister MysteriousBelum ada peringkat

- ExamDokumen8 halamanExamahmed arfanBelum ada peringkat

- KAYE ALEXIS B. DAYAG (BSAIS 2A) ACTIVITY-BASED COSTINGDokumen3 halamanKAYE ALEXIS B. DAYAG (BSAIS 2A) ACTIVITY-BASED COSTINGAlexis Kaye DayagBelum ada peringkat

- Center For Review and Special Studies - : Practical Accounting 1/theory of Accounts M. B. GuiaDokumen13 halamanCenter For Review and Special Studies - : Practical Accounting 1/theory of Accounts M. B. GuiaWilsonBelum ada peringkat

- Financial Statement Analysis Tools for ACC C 204Dokumen18 halamanFinancial Statement Analysis Tools for ACC C 204Hannah JoyBelum ada peringkat

- Standard Costing and Flexible Budget 10Dokumen5 halamanStandard Costing and Flexible Budget 10Lhorene Hope DueñasBelum ada peringkat

- Not Sure What This Is, Could Be ch08Dokumen29 halamanNot Sure What This Is, Could Be ch08ryukenBelum ada peringkat

- Acct 3Dokumen25 halamanAcct 3Diego Salazar100% (1)

- PINTO - Razmen R. (MASECO MT EXAM)Dokumen4 halamanPINTO - Razmen R. (MASECO MT EXAM)Razmen Ramirez PintoBelum ada peringkat

- CH 5 LS Practice HW QUIZDokumen25 halamanCH 5 LS Practice HW QUIZDenise Jane RoqueBelum ada peringkat

- Exercise Workbook For Student 7: SAP B1 On Cloud - BASICDokumen41 halamanExercise Workbook For Student 7: SAP B1 On Cloud - BASICAngelica DalisayBelum ada peringkat

- (Set F) (MC) Chapter 19 - Cost Behavior and Cost-Volume-Profit Analysis Examination Question and AnswersDokumen4 halaman(Set F) (MC) Chapter 19 - Cost Behavior and Cost-Volume-Profit Analysis Examination Question and AnswersJohn Carlos DoringoBelum ada peringkat

- Managerial Accounting Chapter 9 Study Guide Key PointsDokumen13 halamanManagerial Accounting Chapter 9 Study Guide Key Pointsppantin0430Belum ada peringkat

- Test Bank For Principles of Cost Accounting, 16th EditionDokumen56 halamanTest Bank For Principles of Cost Accounting, 16th EditionFornierBelum ada peringkat

- Instalment DISDokumen4 halamanInstalment DISRenelyn David100% (1)

- JOINT COST ALLOCATIONDokumen17 halamanJOINT COST ALLOCATIONChristian Blanza LlevaBelum ada peringkat

- MS-Q1 Concepts - Behavior.cvp - Ac ANSDokumen5 halamanMS-Q1 Concepts - Behavior.cvp - Ac ANSSteff LeeBelum ada peringkat

- Mas ReviewDokumen4 halamanMas ReviewCarl AngeloBelum ada peringkat

- AFAR Assessment 2Dokumen5 halamanAFAR Assessment 2JoshelBuenaventuraBelum ada peringkat

- 2010-03-22 081114 PribumDokumen10 halaman2010-03-22 081114 PribumAndrea RobinsonBelum ada peringkat

- Diamond Motors installment sales profits analysisDokumen4 halamanDiamond Motors installment sales profits analysisGoal Digger Squad VlogBelum ada peringkat

- Study ProbesDokumen48 halamanStudy ProbesRose VeeBelum ada peringkat

- Revenue Recognition: Installment ContractDokumen11 halamanRevenue Recognition: Installment ContractJean Ysrael MarquezBelum ada peringkat

- Quiz4-Responsibilityacctg TP BalscoreDokumen5 halamanQuiz4-Responsibilityacctg TP BalscoreRambell John RodriguezBelum ada peringkat

- Management Advisory Services Activity Cost and CVP Analysis MSQDokumen9 halamanManagement Advisory Services Activity Cost and CVP Analysis MSQMa Teresa B. CerezoBelum ada peringkat

- Responsibility Accounting and Transfer Pricing: Variable Costing & Segmented ReportingDokumen8 halamanResponsibility Accounting and Transfer Pricing: Variable Costing & Segmented ReportingJonailyn YR PeraltaBelum ada peringkat

- Cash 2018 1 Q PDFDokumen4 halamanCash 2018 1 Q PDFLorraine Mae RobridoBelum ada peringkat

- Do It Yourself (DIY #1)Dokumen9 halamanDo It Yourself (DIY #1)acctg2012100% (1)

- Cost allocation methods and break-even analysis questionsDokumen11 halamanCost allocation methods and break-even analysis questionssarahbeeBelum ada peringkat

- MAS - 1416 Profit Planning - CVP AnalysisDokumen24 halamanMAS - 1416 Profit Planning - CVP AnalysisAzureBlazeBelum ada peringkat

- Mas 9000 EconomicsDokumen10 halamanMas 9000 EconomicsAljur SalamedaBelum ada peringkat

- MidtermExam CostingDokumen9 halamanMidtermExam CostingUnknownBelum ada peringkat

- Exam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)Dokumen29 halamanExam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)jhean dabatosBelum ada peringkat

- Advanced Accounting ExamDokumen10 halamanAdvanced Accounting ExamMendoza Ron NixonBelum ada peringkat

- FAR - Final Preboard CPAR 92Dokumen14 halamanFAR - Final Preboard CPAR 92joyhhazelBelum ada peringkat

- Kuis Perbaikan UTS AKbi 2016-2017Dokumen6 halamanKuis Perbaikan UTS AKbi 2016-2017Rizal Sukma PBelum ada peringkat

- Test Bank Advanced Accounting 3e by Jeter 06 ChapterDokumen22 halamanTest Bank Advanced Accounting 3e by Jeter 06 ChapterNicolas ErnestoBelum ada peringkat

- Variable Costing: A Decision-Making Perspective: True-False StatementsDokumen8 halamanVariable Costing: A Decision-Making Perspective: True-False StatementsJanina Marie GarciaBelum ada peringkat

- Assessment No. 3 MAS-03 Absorption and Variable Costing Part 1. Multiple Choice Theory: Choose The Letter of The Best AnswerDokumen10 halamanAssessment No. 3 MAS-03 Absorption and Variable Costing Part 1. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauBelum ada peringkat

- 05 Absorption Vs Variable Costing Answer KEYDokumen3 halaman05 Absorption Vs Variable Costing Answer KEYJemBelum ada peringkat

- Strategic Cost Management Coordinated Quiz 1Dokumen7 halamanStrategic Cost Management Coordinated Quiz 1Kim TaehyungBelum ada peringkat

- The Trans-Pacific Partnership (Trade of Goods)Dokumen6 halamanThe Trans-Pacific Partnership (Trade of Goods)Daniel John Cañares LegaspiBelum ada peringkat

- Candidates For Internship Program For 1st Term AY 2015-2016Dokumen1 halamanCandidates For Internship Program For 1st Term AY 2015-2016Daniel John Cañares LegaspiBelum ada peringkat

- Gen Banking LawDokumen11 halamanGen Banking LawDaniel John Cañares LegaspiBelum ada peringkat

- Bank Secrecy LawDokumen2 halamanBank Secrecy LawDaniel John Cañares LegaspiBelum ada peringkat

- IntelDokumen11 halamanIntelDaniel John Cañares LegaspiBelum ada peringkat

- Table of Contents - Tech DraftDokumen2 halamanTable of Contents - Tech DraftDaniel John Cañares LegaspiBelum ada peringkat

- Certificate of Recognition: Charrevie M. TingsonDokumen2 halamanCertificate of Recognition: Charrevie M. TingsonDaniel John Cañares LegaspiBelum ada peringkat

- PCAOB Auditing Standards Chapter 5Dokumen35 halamanPCAOB Auditing Standards Chapter 5Daniel John Cañares Legaspi100% (1)

- BEHASCIDokumen2 halamanBEHASCIDaniel John Cañares LegaspiBelum ada peringkat

- Santa Rosa Science and Technology High School Values Education ExamDokumen1 halamanSanta Rosa Science and Technology High School Values Education ExamPrinces Paula Mendoza BalanayBelum ada peringkat

- City University of PasayDokumen2 halamanCity University of PasayDaniel John Cañares LegaspiBelum ada peringkat

- SOE Week Sportsfest 2014 Schedule November 24-28Dokumen2 halamanSOE Week Sportsfest 2014 Schedule November 24-28Daniel John Cañares LegaspiBelum ada peringkat

- Scatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Dokumen6 halamanScatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Daniel John Cañares LegaspiBelum ada peringkat

- Stra ManDokumen137 halamanStra ManDaniel John Cañares LegaspiBelum ada peringkat

- Introduction of The CompanyDokumen7 halamanIntroduction of The CompanyDaniel John Cañares LegaspiBelum ada peringkat

- Data DictionaryDokumen4 halamanData DictionaryDaniel John Cañares LegaspiBelum ada peringkat

- Chapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDokumen12 halamanChapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDaniel John Cañares LegaspiBelum ada peringkat

- Phoenix Wright Ace Attorney Trials and TribulationDokumen54 halamanPhoenix Wright Ace Attorney Trials and TribulationjinzoningenBelum ada peringkat

- CentralizeDokumen2 halamanCentralizeDaniel John Cañares LegaspiBelum ada peringkat

- Partnership ReviewerDokumen21 halamanPartnership ReviewerDaniel John Cañares Legaspi100% (1)

- Prinmar SurveyDokumen1 halamanPrinmar SurveyDaniel John Cañares LegaspiBelum ada peringkat

- October 2014 CPALE TopnotchersDokumen2 halamanOctober 2014 CPALE TopnotchersRockacerBelum ada peringkat

- Resume FormatDokumen2 halamanResume FormatJessicaGonzalesBelum ada peringkat

- PhotoshootDokumen1 halamanPhotoshootDaniel John Cañares LegaspiBelum ada peringkat

- Del Mundo Q and ADokumen2 halamanDel Mundo Q and ADaniel John Cañares LegaspiBelum ada peringkat

- 23 Marcon, Louise Margarette 24 Millar, AllyssaDokumen2 halaman23 Marcon, Louise Margarette 24 Millar, AllyssaDaniel John Cañares LegaspiBelum ada peringkat

- Rgf-Glossary of Terms-Chapter 14-Withholding TaxesDokumen1 halamanRgf-Glossary of Terms-Chapter 14-Withholding TaxesanggandakonohBelum ada peringkat

- Chapter 6Dokumen2 halamanChapter 6Daniel John Cañares LegaspiBelum ada peringkat

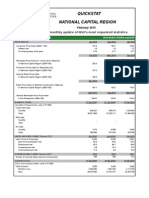

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDokumen3 halamanQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiBelum ada peringkat

- GST BILL Highlights of Draft Model GST LawDokumen6 halamanGST BILL Highlights of Draft Model GST LawS Sinha RayBelum ada peringkat

- EM416 Cost of QualityDokumen24 halamanEM416 Cost of QualityYao SsengssBelum ada peringkat

- Siklus Akuntansi Pada PT Adi JayaDokumen11 halamanSiklus Akuntansi Pada PT Adi Jayafitrianura04Belum ada peringkat

- Toa 25 Cash To Accrual Correction of ErrorsDokumen3 halamanToa 25 Cash To Accrual Correction of Errorsmae tuazonBelum ada peringkat

- Effects of Supervision On Tax ComplianceDokumen5 halamanEffects of Supervision On Tax ComplianceSyehabudin ZmBelum ada peringkat

- Reviewer - Cash & Cash EquivalentsDokumen5 halamanReviewer - Cash & Cash EquivalentsMaria Kathreena Andrea Adeva100% (1)

- Radha Sridhar - 2 - 2019-2020Dokumen2 halamanRadha Sridhar - 2 - 2019-2020Radha SridharBelum ada peringkat

- Hermès H1 2014 Sales Up 8%, Net Income Rises 8Dokumen1 halamanHermès H1 2014 Sales Up 8%, Net Income Rises 8ArcharvindBelum ada peringkat

- Combine PDF Dari TugasDokumen62 halamanCombine PDF Dari TugasAloysius Derry BenediktusBelum ada peringkat

- EFM4, CH 05, Slides, 07-02-18Dokumen44 halamanEFM4, CH 05, Slides, 07-02-18Ainun Nisa NBelum ada peringkat

- Annual-Report-13-14 AOP PDFDokumen38 halamanAnnual-Report-13-14 AOP PDFkhurram_66Belum ada peringkat

- Internship ReportDokumen48 halamanInternship ReportIftekhar Abid FahimBelum ada peringkat

- Pension and Other Retirement BenifitsDokumen8 halamanPension and Other Retirement BenifitsVikas GuptaBelum ada peringkat

- Mindtree Shareholders Report Q2 FY23Dokumen6 halamanMindtree Shareholders Report Q2 FY23Punith DGBelum ada peringkat

- Contract of Architect-ClientDokumen14 halamanContract of Architect-ClientShe Timbancaya100% (1)

- Presentation Part 1Dokumen78 halamanPresentation Part 1charbelBelum ada peringkat

- Zakat as a Powerful Tool for Poverty Relief in Islamic NationsDokumen11 halamanZakat as a Powerful Tool for Poverty Relief in Islamic NationsPurnama Putra0% (1)

- Universal Standards On Social Performance ManagementDokumen21 halamanUniversal Standards On Social Performance ManagementTherese MarieBelum ada peringkat

- Ross 2012Dokumen179 halamanRoss 2012JadBelum ada peringkat

- Alternative Choices and DecisionsDokumen29 halamanAlternative Choices and DecisionsAman BansalBelum ada peringkat

- Full Download Financial Accounting 17th Edition Williams Test BankDokumen35 halamanFull Download Financial Accounting 17th Edition Williams Test Bankmcalljenaevippro100% (42)

- Smart Waste Management: MGT 1022 Lean Start Up ManagementDokumen28 halamanSmart Waste Management: MGT 1022 Lean Start Up Managementsabharish varshan410Belum ada peringkat

- Elements Statement of Comprehensive IncomeDokumen16 halamanElements Statement of Comprehensive IncomeLushelle JiBelum ada peringkat

- Midterm F13 Partial Final f13 For Posting Fall 14 7Dokumen13 halamanMidterm F13 Partial Final f13 For Posting Fall 14 7Miruna CiteaBelum ada peringkat

- Structural Rates 2015Dokumen3 halamanStructural Rates 2015Raghu Ram100% (1)

- Pag Ibig 1Dokumen2 halamanPag Ibig 1Fervi Louie Jalop Bongco0% (1)

- Certificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)Dokumen52 halamanCertificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)jeanieBelum ada peringkat

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDokumen35 halamanChapter Five: The Financial Statements of Banks and Their Principal Competitorsعبدالله ماجد المطارنه100% (1)

- Pro Excel Financial Modeling - Company Business Model - (CBM)Dokumen393 halamanPro Excel Financial Modeling - Company Business Model - (CBM)Tanzeel Ur Rahman GazdarBelum ada peringkat

- Financial Accounting Course IntroductionDokumen4 halamanFinancial Accounting Course IntroductionApolloniousBelum ada peringkat