Anda mungkin juga menyukai

- Bautista v Sarmiento Burden of Proof Criminal CaseDokumen1 halamanBautista v Sarmiento Burden of Proof Criminal CaseleeashleeBelum ada peringkat

- 24 Camp John Hay Development Corp. v. CBAA, 706 SCRA 547Dokumen2 halaman24 Camp John Hay Development Corp. v. CBAA, 706 SCRA 547Raymond MedinaBelum ada peringkat

- Validity of Municipal Tax Ordinance and Issuance of Writ of Preliminary InjunctionDokumen3 halamanValidity of Municipal Tax Ordinance and Issuance of Writ of Preliminary InjunctionSarah BuendiaBelum ada peringkat

- National Power Corporation vs. City of Cabanatuan FactsDokumen6 halamanNational Power Corporation vs. City of Cabanatuan FactsSuzyBelum ada peringkat

- Province of Batangas v. RomuloDokumen1 halamanProvince of Batangas v. RomuloYieMaghirangBelum ada peringkat

- 11 Southern Cross Cement Corporation v. Cement Manufacturers Association of The Philippines, Et Al.Dokumen8 halaman11 Southern Cross Cement Corporation v. Cement Manufacturers Association of The Philippines, Et Al.Tricia MontoyaBelum ada peringkat

- Cir V CA Adminlaw DigestDokumen1 halamanCir V CA Adminlaw Digestdats_idjiBelum ada peringkat

- Cir v. CA, Cta, Admu - G.R. No. 115349Dokumen3 halamanCir v. CA, Cta, Admu - G.R. No. 115349Krisha Marie Tan BuelaBelum ada peringkat

- Admin Law Compiled Class Digests 2 PDFDokumen38 halamanAdmin Law Compiled Class Digests 2 PDFMark Evan GarciaBelum ada peringkat

- RAMOS vs. BAROTDokumen1 halamanRAMOS vs. BAROTJulioBelum ada peringkat

- Pbcom V CirDokumen2 halamanPbcom V CirVianca MiguelBelum ada peringkat

- 047 BUNALES Lim Hoa Ting vs. Central Bank of The PhilippinesDokumen2 halaman047 BUNALES Lim Hoa Ting vs. Central Bank of The PhilippinesCarissa Cruz100% (3)

- Rhom Apollo vs. CIRDokumen1 halamanRhom Apollo vs. CIRKia BiBelum ada peringkat

- CTA Ruling Upheld on Invalid BIR Interpretation of Fermented Liquor Tax RateDokumen2 halamanCTA Ruling Upheld on Invalid BIR Interpretation of Fermented Liquor Tax RatePeanutButter 'n JellyBelum ada peringkat

- San Miguel Corp vs. AvelinoDokumen1 halamanSan Miguel Corp vs. AvelinoCarlota Nicolas VillaromanBelum ada peringkat

- 003 CIR Vs CA (D)Dokumen2 halaman003 CIR Vs CA (D)Kendi Lu Macabaya FernandezBelum ada peringkat

- Philippine Bank of Communications v. CIR, G.R. No. 112024Dokumen3 halamanPhilippine Bank of Communications v. CIR, G.R. No. 112024Bibi JumpolBelum ada peringkat

- Roxas v. RaffertyDokumen2 halamanRoxas v. RaffertySophiaFrancescaEspinosaBelum ada peringkat

- Borja Vs GellaDokumen4 halamanBorja Vs Gelladwight yuBelum ada peringkat

- Paseo Realty and Dev't. Corp. v. CA, 309 SCRA 402Dokumen2 halamanPaseo Realty and Dev't. Corp. v. CA, 309 SCRA 402Jo DevisBelum ada peringkat

- PLDT vs. NLRC (673 Scra 676) Case DigestDokumen4 halamanPLDT vs. NLRC (673 Scra 676) Case DigestCarlota Nicolas VillaromanBelum ada peringkat

- ERC Vs CA - Case DigestDokumen2 halamanERC Vs CA - Case DigestJoanna CusiBelum ada peringkat

- Philippine Bank of Communications V. Cir G.R. No. 112024 January 28, 1999 Quisumbing, JDokumen2 halamanPhilippine Bank of Communications V. Cir G.R. No. 112024 January 28, 1999 Quisumbing, JbrendamanganaanBelum ada peringkat

- 27 CIR V La Tondena G.R. No. L-10431Dokumen1 halaman27 CIR V La Tondena G.R. No. L-10431Emmanuel Alejandro YrreverreIiiBelum ada peringkat

- CIR Vs CTA DigestDokumen2 halamanCIR Vs CTA DigestAbilene Joy Dela Cruz83% (6)

- Hilado V Collector of Internal RevenueDokumen2 halamanHilado V Collector of Internal RevenueErnest Levanza83% (6)

- Baliwag Transit vs. CADokumen2 halamanBaliwag Transit vs. CACaroline A. LegaspinoBelum ada peringkat

- ABS-CBN v CTA Retroactive Application of Tax CircularDokumen2 halamanABS-CBN v CTA Retroactive Application of Tax Circularkjhenyo218502Belum ada peringkat

- PLDT Franchise Tax Exemption Rejected by Supreme CourtDokumen1 halamanPLDT Franchise Tax Exemption Rejected by Supreme CourtAlan GultiaBelum ada peringkat

- Philippine Bank of Communications v. CIRDokumen3 halamanPhilippine Bank of Communications v. CIRDaLe AparejadoBelum ada peringkat

- Definition, Distinction and Classification: The Law On Public OfficersDokumen34 halamanDefinition, Distinction and Classification: The Law On Public OfficersBam SantosBelum ada peringkat

- Tax Case Digest: PB Com V. CIR (1999) : G.R. No. 112024Dokumen2 halamanTax Case Digest: PB Com V. CIR (1999) : G.R. No. 112024RexBelum ada peringkat

- LORENZO Vs POSADAS G.R. No. L-43082 June 18, 1937Dokumen3 halamanLORENZO Vs POSADAS G.R. No. L-43082 June 18, 1937Francise Mae Montilla Mordeno100% (3)

- Planteras, Jr. vs. People (Full Text, Word Version)Dokumen15 halamanPlanteras, Jr. vs. People (Full Text, Word Version)Emir MendozaBelum ada peringkat

- Supreme Court Rules on VAT Law ConstitutionalityDokumen4 halamanSupreme Court Rules on VAT Law ConstitutionalityMarkBelum ada peringkat

- Edna Diago Lhuillier V. British Airways: G.R. No. 171092, March 15, 2010Dokumen3 halamanEdna Diago Lhuillier V. British Airways: G.R. No. 171092, March 15, 2010JeNovaBelum ada peringkat

- SMART VS. NTC; G.R. No. 151908 PARTIES Dispute Over NTC Billing RulesDokumen2 halamanSMART VS. NTC; G.R. No. 151908 PARTIES Dispute Over NTC Billing RulesJacinto Jr Jamero100% (6)

- SMART COMMUNICATIONS, INC. ET AL. v. NTC - DigestDokumen2 halamanSMART COMMUNICATIONS, INC. ET AL. v. NTC - DigestMark Genesis Rojas100% (1)

- CIR v. FortuneDokumen2 halamanCIR v. FortunedelayinggratificationBelum ada peringkat

- Special Penal Laws PDFDokumen22 halamanSpecial Penal Laws PDFTori PeigeBelum ada peringkat

- Case British American Tobacco V CamachoDokumen4 halamanCase British American Tobacco V CamachoMary Joy NavajaBelum ada peringkat

- CASE #12 Manzanaris v. People G.R. No. L-64750 Principle: Actus Non Facit Reum, Nisi Mens Sit ReaDokumen3 halamanCASE #12 Manzanaris v. People G.R. No. L-64750 Principle: Actus Non Facit Reum, Nisi Mens Sit ReaCarmel Grace KiwasBelum ada peringkat

- Administrative Law Cases 4Dokumen23 halamanAdministrative Law Cases 4jerryarmsBelum ada peringkat

- Anti-Graft League of The Philippines v. San Juan: FactsDokumen1 halamanAnti-Graft League of The Philippines v. San Juan: FactsLloyd LiwagBelum ada peringkat

- Case Digest Iron Steel Vs CADokumen2 halamanCase Digest Iron Steel Vs CAEbbe Dy100% (1)

- Tuason Vs PosadasDokumen1 halamanTuason Vs PosadasRTC-OCC Olongapo CityBelum ada peringkat

- Smietanka, Collector of Internal Revenue v. First Trust & Savings Bank, 257 U.S. 602 (1921)Dokumen4 halamanSmietanka, Collector of Internal Revenue v. First Trust & Savings Bank, 257 U.S. 602 (1921)Scribd Government DocsBelum ada peringkat

- Benefits Received Theory in Inheritance TaxationDokumen2 halamanBenefits Received Theory in Inheritance TaxationPatrick Anthony Llasus-NafarreteBelum ada peringkat

- Lopez vs. City of ManilaDokumen2 halamanLopez vs. City of ManilaDeniel Salvador B. MorilloBelum ada peringkat

- #75 - DUMAPIS, Et - Al. V. LEPANTODokumen2 halaman#75 - DUMAPIS, Et - Al. V. LEPANTOKê MilanBelum ada peringkat

- Board of Trustees of GSIS v. VelascoDokumen3 halamanBoard of Trustees of GSIS v. VelascoMaribel Nicole Lopez100% (1)

- CIR v. BPIDokumen2 halamanCIR v. BPIIshBelum ada peringkat

- CIR v. San Miguel CorporationDokumen1 halamanCIR v. San Miguel CorporationKym AlgarmeBelum ada peringkat

- Cawad V AbadDokumen2 halamanCawad V AbadClarence Protacio100% (1)

- VRB Tax Authority and Municipal Boundary Changes ChallengedDokumen9 halamanVRB Tax Authority and Municipal Boundary Changes ChallengedErick Jay InokBelum ada peringkat

- 1.hilado v. CIR, 100 Phil 288Dokumen1 halaman1.hilado v. CIR, 100 Phil 288Jo DevisBelum ada peringkat

- People Vs GalagacDokumen10 halamanPeople Vs GalagacBea CapeBelum ada peringkat

- 100 Defined Terms in Public International LawDokumen14 halaman100 Defined Terms in Public International LawErmi YamaBelum ada peringkat

- Abakada Guro Party List vs. Ermita (G.R. No. 168056, September 1, 2005)Dokumen4 halamanAbakada Guro Party List vs. Ermita (G.R. No. 168056, September 1, 2005)Jennilyn Gulfan YaseBelum ada peringkat

- VAT rate hike duty lies with PresidentDokumen4 halamanVAT rate hike duty lies with PresidentMichael DonascoBelum ada peringkat

- Dolo Causante v. Incidente - Ferro Chemicals v. Antonio M. GarciaDokumen47 halamanDolo Causante v. Incidente - Ferro Chemicals v. Antonio M. Garciakjhenyo218502Belum ada peringkat

- Castillo Poli Saño v. COMELECDokumen4 halamanCastillo Poli Saño v. COMELECkjhenyo218502Belum ada peringkat

- 7 Steps To Getting A Mayor's Permit - Business Registration - Full SuiteDokumen13 halaman7 Steps To Getting A Mayor's Permit - Business Registration - Full Suitekjhenyo218502100% (1)

- Dangerously Neglecting Courtroom Realities: Citing LiteratureDokumen2 halamanDangerously Neglecting Courtroom Realities: Citing Literaturekjhenyo218502Belum ada peringkat

- Spes Form 5 - Employment ContractDokumen1 halamanSpes Form 5 - Employment Contractkjhenyo218502Belum ada peringkat

- November27 PeoplevsVelasco RemDokumen4 halamanNovember27 PeoplevsVelasco Remkjhenyo218502Belum ada peringkat

- MA Public Records Request GuideDokumen1 halamanMA Public Records Request Guidekjhenyo218502Belum ada peringkat

- Belo vs. Guevarra - A Landmark Case For Facebook Privacy in PH - Newsbytes PhilippinesDokumen4 halamanBelo vs. Guevarra - A Landmark Case For Facebook Privacy in PH - Newsbytes Philippineskjhenyo218502Belum ada peringkat

- Sample of Employment Contact PT EngDokumen3 halamanSample of Employment Contact PT EngjaciemBelum ada peringkat

- Inheritance Claim of Illegitimate ChildDokumen11 halamanInheritance Claim of Illegitimate Childkjhenyo218502Belum ada peringkat

- Standard Contract - HouseholdDokumen3 halamanStandard Contract - HouseholdJoshuaLavegaAbrinaBelum ada peringkat

- Article I - Name That Corporation - BusinessMirrorDokumen3 halamanArticle I - Name That Corporation - BusinessMirrorkjhenyo218502Belum ada peringkat

- TaxRev - Marubeni v. CIR (1989) (NON-Resident Foreign Corporation)Dokumen16 halamanTaxRev - Marubeni v. CIR (1989) (NON-Resident Foreign Corporation)kjhenyo218502Belum ada peringkat

- Civ1Rev - Ayala Investment v. CA (Art. 121, Family Code)Dokumen13 halamanCiv1Rev - Ayala Investment v. CA (Art. 121, Family Code)kjhenyo218502Belum ada peringkat

- Political - Hermano Oil v. TRBDokumen16 halamanPolitical - Hermano Oil v. TRBkjhenyo218502Belum ada peringkat

- TaxRev - CIR v. Liquigaz Philippines (A VOID FDDA Does NOT Render The Assessment Void)Dokumen42 halamanTaxRev - CIR v. Liquigaz Philippines (A VOID FDDA Does NOT Render The Assessment Void)kjhenyo218502Belum ada peringkat

- Civ1Rev - Garrido v. Javier (Prescriptive Period of Civil Liability Arising From Criminal Offense)Dokumen5 halamanCiv1Rev - Garrido v. Javier (Prescriptive Period of Civil Liability Arising From Criminal Offense)kjhenyo218502Belum ada peringkat

- Taxrev - Cepalco v. City of CdoDokumen26 halamanTaxrev - Cepalco v. City of Cdokjhenyo218502Belum ada peringkat

- CivRev2 - Samar Mining Co. v. Northern LoydDokumen7 halamanCivRev2 - Samar Mining Co. v. Northern Loydkjhenyo218502Belum ada peringkat

- TaxRev - PLDT v. City of Davao (WITHDRAWAL of Exemption From Local Franchise Tax)Dokumen23 halamanTaxRev - PLDT v. City of Davao (WITHDRAWAL of Exemption From Local Franchise Tax)kjhenyo218502Belum ada peringkat

- TaxRev - BDO v. RPDokumen76 halamanTaxRev - BDO v. RPkjhenyo218502Belum ada peringkat

- CA Affirms No Express Prohibition to Collate Donated PropertiesDokumen5 halamanCA Affirms No Express Prohibition to Collate Donated Propertieskjhenyo218502Belum ada peringkat

- Supreme Court Rules Conjugal Properties Not Liable for Husband's Corporate Surety AgreementDokumen13 halamanSupreme Court Rules Conjugal Properties Not Liable for Husband's Corporate Surety Agreementkjhenyo218502Belum ada peringkat

- Civ1Rev - Victoriano v. CA (Laches May DEFEAT Registered Owner)Dokumen6 halamanCiv1Rev - Victoriano v. CA (Laches May DEFEAT Registered Owner)kjhenyo218502Belum ada peringkat

- Civ1Rev - Nera v. Rimando (In The Presence of Subscribing Witnesses To A Will)Dokumen4 halamanCiv1Rev - Nera v. Rimando (In The Presence of Subscribing Witnesses To A Will)kjhenyo218502Belum ada peringkat

- RENE A.V. SAGUISAG Vs EXECUTIVE SECRETARY PA QUITO N. OCHOA, JR. (G.R. No. 212426)Dokumen118 halamanRENE A.V. SAGUISAG Vs EXECUTIVE SECRETARY PA QUITO N. OCHOA, JR. (G.R. No. 212426)Armstrong BosantogBelum ada peringkat

- Civ1Rev - People v. Bayotas (Death of Accused Pending Appeal of Conviction)Dokumen17 halamanCiv1Rev - People v. Bayotas (Death of Accused Pending Appeal of Conviction)kjhenyo218502Belum ada peringkat

- Inheritance Claim of Illegitimate ChildDokumen11 halamanInheritance Claim of Illegitimate Childkjhenyo218502Belum ada peringkat

- SpecPro - Ceruila v. DelantarDokumen3 halamanSpecPro - Ceruila v. Delantarkjhenyo218502Belum ada peringkat

- Specpro - Ilusorio V Ilusorio-BildnerDokumen6 halamanSpecpro - Ilusorio V Ilusorio-Bildnerkjhenyo218502Belum ada peringkat

- Invoice: Ayub Printers and ComposersDokumen1 halamanInvoice: Ayub Printers and ComposersHabib Ur REHMANBelum ada peringkat

- UDA Consultant RFPDokumen31 halamanUDA Consultant RFPASHUTOSHBelum ada peringkat

- Solved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedDokumen1 halamanSolved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedAnbu jaromiaBelum ada peringkat

- BHL FY19 Annual ReportDokumen94 halamanBHL FY19 Annual ReportFoysal NobinBelum ada peringkat

- Sindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFDokumen64 halamanSindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFrohail51Belum ada peringkat

- Summary of Fund Perf - Sept 2012 LIFE ACCOUNTDokumen4 halamanSummary of Fund Perf - Sept 2012 LIFE ACCOUNTJohn SmithBelum ada peringkat

- Basis of Malaysian Income TaxDokumen6 halamanBasis of Malaysian Income TaxhisyamstarkBelum ada peringkat

- Fairtrading - Nsw.gov - Au-Levies and Capital Works Funds PDFDokumen4 halamanFairtrading - Nsw.gov - Au-Levies and Capital Works Funds PDFKris VenkatBelum ada peringkat

- Business Pearson Unit 2Dokumen25 halamanBusiness Pearson Unit 2HasanBelum ada peringkat

- Kohat Cement Company LTD: Profit and Loss Account For The Year Ended On . Rupees in (''000'') Gross Sales 1958321 2800130Dokumen54 halamanKohat Cement Company LTD: Profit and Loss Account For The Year Ended On . Rupees in (''000'') Gross Sales 1958321 2800130Sohail AdnanBelum ada peringkat

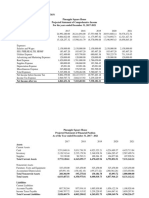

- Five-Year Financial Projection Pineapple Square House Projected Statement of Comprehensive Income For The Years Ended December 31, 2017-2021Dokumen4 halamanFive-Year Financial Projection Pineapple Square House Projected Statement of Comprehensive Income For The Years Ended December 31, 2017-2021Rey PordalizaBelum ada peringkat

- 2017-An Ordinance Enacting The Revised Pasig Revenue CodeDokumen194 halaman2017-An Ordinance Enacting The Revised Pasig Revenue CodeRandy PaderesBelum ada peringkat

- GST and Mutual Funds in India: A Case StudyDokumen6 halamanGST and Mutual Funds in India: A Case StudyIAEME PublicationBelum ada peringkat

- CFAP 1 AFR Winter 2021Dokumen5 halamanCFAP 1 AFR Winter 2021Taqweem KhanBelum ada peringkat

- Kone Elevators CaseDokumen2 halamanKone Elevators Casealok_jallanBelum ada peringkat

- BComPart-03 2021317111449Dokumen32 halamanBComPart-03 2021317111449Hemmu sahuBelum ada peringkat

- PAYROLL - ProblemDokumen3 halamanPAYROLL - Problemshaipink2000Belum ada peringkat

- Case DigestDokumen70 halamanCase Digestattycpajfcc100% (1)

- Business Financials MRFDokumen13 halamanBusiness Financials MRFarshdhirBelum ada peringkat

- Band 5 EssaysDokumen18 halamanBand 5 Essays曾迦圆Belum ada peringkat

- Taxation and Fiscal PoliciesDokumen279 halamanTaxation and Fiscal PoliciesFun DietBelum ada peringkat

- Supreme Court: Sycip, Salazar and Associates For Petitioners. Office of The Solicitor General For RespondentDokumen8 halamanSupreme Court: Sycip, Salazar and Associates For Petitioners. Office of The Solicitor General For RespondentMamerto Egargo Jr.Belum ada peringkat

- Tax Rates for CorporationsDokumen14 halamanTax Rates for CorporationsMendoza Khlareese AndreaBelum ada peringkat

- ICSE Economics3Dokumen6 halamanICSE Economics3Ritesh SinghBelum ada peringkat

- HHGHGHGDokumen5 halamanHHGHGHGBran TuazonBelum ada peringkat

- 2017 11 Economics Sample Paper 02 Ans Ot8ebDokumen5 halaman2017 11 Economics Sample Paper 02 Ans Ot8ebramukolakiBelum ada peringkat

- Galvin Report Pt4Dokumen18 halamanGalvin Report Pt4MunnkeymannBelum ada peringkat

- BIR Rule on Taxing Clubs OverturnedDokumen2 halamanBIR Rule on Taxing Clubs OverturnedLucky JavellanaBelum ada peringkat

- Basic Rental Analysis WorksheetDokumen8 halamanBasic Rental Analysis WorksheetGleb petukhovBelum ada peringkat

- Eisner V Macomber DigestDokumen1 halamanEisner V Macomber DigestKTBelum ada peringkat