Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- San Luis v. San Luis (SPECPRO)Dokumen1 halamanSan Luis v. San Luis (SPECPRO)mileyBelum ada peringkat

- Syllabus - Introduction To Modern Asian History - Cornell 2013Dokumen7 halamanSyllabus - Introduction To Modern Asian History - Cornell 2013MitchBelum ada peringkat

- Jagannath HoraDokumen8 halamanJagannath Horarasiya490% (1)

- SC upholds conviction of man for attempted estafa through falsification of Philippine sweepstakes ticketDokumen4 halamanSC upholds conviction of man for attempted estafa through falsification of Philippine sweepstakes ticketKat JolejoleBelum ada peringkat

- CRPC ProcedureDokumen357 halamanCRPC ProcedureNagaraj Kumble92% (13)

- An Astrobiographical Sketchof DR BVRaman by KNRao Part 1 BWDokumen16 halamanAn Astrobiographical Sketchof DR BVRaman by KNRao Part 1 BWRavindra Kumar Kaul100% (1)

- Ferrer VS BautistaDokumen3 halamanFerrer VS BautistaClaudine Christine A. VicenteBelum ada peringkat

- NirayanaDokumen6 halamanNirayanarasiya49Belum ada peringkat

- Ureta V Ureta Case DigestDokumen2 halamanUreta V Ureta Case Digesthistab100% (4)

- Sample Employee Information FormDokumen1 halamanSample Employee Information Formrasiya49Belum ada peringkat

- रषटरय जगरण 2 - 7 - 21Dokumen16 halamanरषटरय जगरण 2 - 7 - 21rasiya49Belum ada peringkat

- MacpDokumen1 halamanMacprasiya49Belum ada peringkat

- Medical Collages ListDokumen19 halamanMedical Collages Listrasiya49Belum ada peringkat

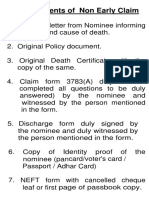

- Non Early Death Claim RequirementsDokumen8 halamanNon Early Death Claim Requirementsrasiya49Belum ada peringkat

- Epf ActDokumen18 halamanEpf ActPraveen KumarBelum ada peringkat

- Partnership Deed FormatDokumen4 halamanPartnership Deed FormatPranathi DivakarBelum ada peringkat

- Entity PDFDokumen1 halamanEntity PDFrasiya49Belum ada peringkat

- Enlistment Rules 2013Dokumen67 halamanEnlistment Rules 2013abhijithavalBelum ada peringkat

- Biology - Quiz-11Dokumen53 halamanBiology - Quiz-11rasiya49Belum ada peringkat

- Experiece of 3Dokumen25 halamanExperiece of 3rasiya49Belum ada peringkat

- AA Enterprises Attandance SheetDokumen1 halamanAA Enterprises Attandance Sheetrasiya49Belum ada peringkat

- People as the Key ResourceDokumen13 halamanPeople as the Key ResourceNeelankshi GuptaBelum ada peringkat

- Update KYC detailsDokumen2 halamanUpdate KYC detailsrasiya49Belum ada peringkat

- New Features in PL7Dokumen29 halamanNew Features in PL7binaywatchBelum ada peringkat

- People as the Key ResourceDokumen13 halamanPeople as the Key ResourceNeelankshi GuptaBelum ada peringkat

- Detail of Bill PaymentInfo17-May-2015 Lic GurgaonDokumen2 halamanDetail of Bill PaymentInfo17-May-2015 Lic Gurgaonrasiya49Belum ada peringkat

- Tarpana SanskritDokumen9 halamanTarpana SanskritnavinnaithaniBelum ada peringkat

- On-Line Payment ReceiptDokumen1 halamanOn-Line Payment Receiptrasiya49Belum ada peringkat

- Draw Result DDA2010Dokumen1.021 halamanDraw Result DDA2010RealEstate-Property-Delhi-NCRBelum ada peringkat

- PTRNDMC For 2015-16 Hindi EnglishDokumen15 halamanPTRNDMC For 2015-16 Hindi Englishrasiya49Belum ada peringkat

- Power Tariff GurgaonDokumen5 halamanPower Tariff Gurgaonrasiya49Belum ada peringkat

- Draw Result DDA2010Dokumen1.021 halamanDraw Result DDA2010RealEstate-Property-Delhi-NCRBelum ada peringkat

- OD40612028644 InvoiceDokumen1 halamanOD40612028644 Invoicerasiya49Belum ada peringkat

- CVC Guidelines Regarding IntimationDokumen2 halamanCVC Guidelines Regarding Intimationrasiya49Belum ada peringkat

- Cic Order Dt. 13.10.20140001Dokumen2 halamanCic Order Dt. 13.10.20140001rasiya49Belum ada peringkat

- Madhur Joshi's Horoscope0001Dokumen22 halamanMadhur Joshi's Horoscope0001rasiya49Belum ada peringkat

- AHAI Statement On Coach Tom "Chico" AdrahtasDokumen1 halamanAHAI Statement On Coach Tom "Chico" AdrahtasAdam HarringtonBelum ada peringkat

- Class 10 English First Flight - Nelson Mandela - Long Walk To FreedomDokumen9 halamanClass 10 English First Flight - Nelson Mandela - Long Walk To FreedomShivam YadavBelum ada peringkat

- Slovenians, Non-Slovenians... by Irena SumiDokumen18 halamanSlovenians, Non-Slovenians... by Irena SumiSlovenian Webclassroom Topic ResourcesBelum ada peringkat

- Court of Appeals Jurisdiction Over Habeas Corpus Cases Involving Child CustodyDokumen6 halamanCourt of Appeals Jurisdiction Over Habeas Corpus Cases Involving Child CustodyMary Divina FranciscoBelum ada peringkat

- 2017 Judgement 20-Mar-2018Dokumen89 halaman2017 Judgement 20-Mar-2018vakilchoubeyBelum ada peringkat

- Annotated BibliographyDokumen8 halamanAnnotated Bibliographyapi-301364293Belum ada peringkat

- (A284) Jacob v. SandiganbayanDokumen19 halaman(A284) Jacob v. Sandiganbayanms aBelum ada peringkat

- Universal Declaration of Human RightsDokumen2 halamanUniversal Declaration of Human Rightsdverso36Belum ada peringkat

- Demapiles Vs COMELECDokumen2 halamanDemapiles Vs COMELECKelly EstradaBelum ada peringkat

- Accomplice Liability Summary PDFDokumen9 halamanAccomplice Liability Summary PDFMissy MeyerBelum ada peringkat

- Establishing Hedge Funds in The Cayman Islands - An Alternative View - Asia Fund Manager - Julian Stockley-SmithDokumen3 halamanEstablishing Hedge Funds in The Cayman Islands - An Alternative View - Asia Fund Manager - Julian Stockley-SmithJPFundsGroupBelum ada peringkat

- 2 Gr-No-221697-Poe-V-Comelec-Pres-Candidacy-CaseDokumen12 halaman2 Gr-No-221697-Poe-V-Comelec-Pres-Candidacy-CaseEllen DebutonBelum ada peringkat

- Boehmer Et Al (2004)Dokumen39 halamanBoehmer Et Al (2004)Mobile Legend Live streaming indonesiaBelum ada peringkat

- Charlton Hestons RhetoricDokumen10 halamanCharlton Hestons RhetoricJay LainoBelum ada peringkat

- Expert & Non-Testifying Witnesses ChartDokumen1 halamanExpert & Non-Testifying Witnesses ChartRonnie Barcena Jr.Belum ada peringkat

- GD Topics For SSBDokumen7 halamanGD Topics For SSBHaq se NationalistBelum ada peringkat

- Evidence Part 1 PDFDokumen7 halamanEvidence Part 1 PDFattytheaBelum ada peringkat

- Japanese Militarism: Empire, Manchuria, AxisDokumen1 halamanJapanese Militarism: Empire, Manchuria, AxisEllaBelum ada peringkat

- Difference Between FERA and FEMADokumen3 halamanDifference Between FERA and FEMAshikshaBelum ada peringkat

- Equity EssayDokumen8 halamanEquity EssayTeeruVarasuBelum ada peringkat

- Implementing Labor Code Rules on Termination of EmploymentDokumen9 halamanImplementing Labor Code Rules on Termination of EmploymentKurt Francis Romel SolonBelum ada peringkat

- Legal Ethics Bar Exam ReviewDokumen10 halamanLegal Ethics Bar Exam ReviewRob BankyBelum ada peringkat

- Kenya School of Law Act SummaryDokumen21 halamanKenya School of Law Act SummaryTrish Wachuka Gichane0% (1)

- 04th August Labour LawDokumen7 halaman04th August Labour LawJasmine KBelum ada peringkat