Anda mungkin juga menyukai

- Exam Prep for:: Business Analysis and Valuation Using Financial Statements, Text and CasesDari EverandExam Prep for:: Business Analysis and Valuation Using Financial Statements, Text and CasesBelum ada peringkat

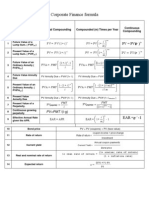

- CorpFinance Cheat Sheet v2.2Dokumen2 halamanCorpFinance Cheat Sheet v2.2subtle69100% (4)

- Corporate Finance Formula SheetDokumen4 halamanCorporate Finance Formula Sheetogsunny100% (3)

- Kelly's Finance Cheat Sheet V6Dokumen2 halamanKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

- CheatSheet (Finance)Dokumen1 halamanCheatSheet (Finance)Guan Yu Lim100% (3)

- Corporate Finance - FormulasDokumen3 halamanCorporate Finance - FormulasAbhijit Pandit100% (1)

- Cheat Sheet Final - FMVDokumen3 halamanCheat Sheet Final - FMVhanifakih100% (2)

- Corporate Finance FormulasDokumen3 halamanCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Corporate FinanceDokumen19 halamanCorporate FinanceBilal Shahid100% (4)

- Corporate Finance - Berk DeMarzo- Test Bank Chapter 19 - 百度文库Dokumen26 halamanCorporate Finance - Berk DeMarzo- Test Bank Chapter 19 - 百度文库TaanzBelum ada peringkat

- CFA Formula Cheat SheetDokumen9 halamanCFA Formula Cheat SheetChingWa ChanBelum ada peringkat

- Chapter 1 Strategic Management ProcessDokumen2 halamanChapter 1 Strategic Management Processnightmonkey215100% (2)

- Corporate Finance OutlineDokumen45 halamanCorporate Finance Outlinemweaveruga100% (5)

- Fnce 100 Final Cheat SheetDokumen2 halamanFnce 100 Final Cheat SheetToby Arriaga100% (2)

- FIN6215-Cheat Sheet BigDokumen3 halamanFIN6215-Cheat Sheet BigJojo Kittiya100% (1)

- Allen Lane Case Write UpDokumen2 halamanAllen Lane Case Write UpAndrew Choi100% (1)

- CFADokumen74 halamanCFAShuyang ZhengBelum ada peringkat

- Equity ValuationDokumen2.424 halamanEquity ValuationMuteeb Raina0% (1)

- Maximise Firm Value with Corporate Finance PrinciplesDokumen4 halamanMaximise Firm Value with Corporate Finance PrinciplesLynetteBelum ada peringkat

- Financial Accounting: Tools For Business Decision-Making, Third Canadian EditionDokumen6 halamanFinancial Accounting: Tools For Business Decision-Making, Third Canadian Editionapi-19743565100% (1)

- Summary - Corporate Finance Beck DeMarzoDokumen54 halamanSummary - Corporate Finance Beck DeMarzoAlejandra100% (2)

- Finance Cheat SheetDokumen4 halamanFinance Cheat SheetRudolf Jansen van RensburgBelum ada peringkat

- Solution Manual For Corporate Finance 4th Edition by BerkDokumen3 halamanSolution Manual For Corporate Finance 4th Edition by Berka38476880414% (7)

- Cheat Sheet Corporate - FinanceDokumen2 halamanCheat Sheet Corporate - FinanceAnna BudaevaBelum ada peringkat

- CheatDokumen1 halamanCheatIshmo KueedBelum ada peringkat

- Corporate FinanceDokumen24 halamanCorporate Financeapi-3719687100% (3)

- LBO Valuation Model PDFDokumen101 halamanLBO Valuation Model PDFAbhishek Singh100% (3)

- Private Equity Case StudyDokumen11 halamanPrivate Equity Case StudyAmineBekkalBelum ada peringkat

- Comparable Companies TemplateDokumen23 halamanComparable Companies Templatesandeep chaurasiaBelum ada peringkat

- Investment Banking: Valuation, Leveraged Buyouts, and Mergers & AcquisitionsDokumen22 halamanInvestment Banking: Valuation, Leveraged Buyouts, and Mergers & Acquisitionsaleaf92100% (1)

- CFA Level 1 Study Guide: Corporate FinanceDokumen343 halamanCFA Level 1 Study Guide: Corporate Financed-fbuser-32825803100% (12)

- Corporate Finance - Beny W2011Dokumen38 halamanCorporate Finance - Beny W2011cparka12Belum ada peringkat

- Precedent TransactionsDokumen14 halamanPrecedent Transactionslondoner4545100% (3)

- Corporate Finance Test Bank and Solutions ManualDokumen8 halamanCorporate Finance Test Bank and Solutions Manualnaxipo18% (22)

- LBO DELL Presentation Case StudyDokumen20 halamanLBO DELL Presentation Case StudyJoseph TanBelum ada peringkat

- Equity Research Company UpdateDokumen16 halamanEquity Research Company Updateapi-26204863100% (1)

- Financial Modeling Fundamentals - More Advanced 3-Statement ProjectionsDokumen10 halamanFinancial Modeling Fundamentals - More Advanced 3-Statement ProjectionsPrashantKBelum ada peringkat

- FinClub - 57th Batch Interview Question BankDokumen16 halamanFinClub - 57th Batch Interview Question BankAKSHAY PANWARBelum ada peringkat

- Work Sample - M&A Private Equity Buyside AdvisingDokumen20 halamanWork Sample - M&A Private Equity Buyside AdvisingsunnybrsraoBelum ada peringkat

- Equity Valuation DCF, WACC and APVDokumen64 halamanEquity Valuation DCF, WACC and APVstf2xBelum ada peringkat

- SOTP ValuationDokumen26 halamanSOTP ValuationRishabh KesharwaniBelum ada peringkat

- BF2201 Cheat Sheet FinalsDokumen2 halamanBF2201 Cheat Sheet Finalssiewhong93100% (1)

- Corporate FinanceDokumen410 halamanCorporate Financedavidrill100% (2)

- Chapter 1 - Updated-1 PDFDokumen29 halamanChapter 1 - Updated-1 PDFj000diBelum ada peringkat

- BUS 330 Exam 1 - Fall 2012 (B) - SolutionDokumen14 halamanBUS 330 Exam 1 - Fall 2012 (B) - SolutionTao Chun LiuBelum ada peringkat

- Practice Worksheet Solutions - IBFDokumen13 halamanPractice Worksheet Solutions - IBFsusheel kumarBelum ada peringkat

- TCCB REVISIONDokumen44 halamanTCCB REVISION21070119Belum ada peringkat

- Shares and Bonds Are Float in ?: (A) Money MarketDokumen16 halamanShares and Bonds Are Float in ?: (A) Money MarketMurad AliBelum ada peringkat

- Relationship between MPS and MPCDokumen31 halamanRelationship between MPS and MPCJay SmithBelum ada peringkat

- Common Stock ValuationDokumen40 halamanCommon Stock ValuationAhsan IqbalBelum ada peringkat

- BCM Corporate Finance IDokumen10 halamanBCM Corporate Finance IquynhnannieBelum ada peringkat

- 61556Dokumen31 halaman61556Jay SmithBelum ada peringkat

- Typical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetDokumen7 halamanTypical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetSylvan EversBelum ada peringkat

- Cost of CapitalDokumen39 halamanCost of CapitalEkta JaiswalBelum ada peringkat

- Chuong 1 Introduction 2013 SDokumen82 halamanChuong 1 Introduction 2013 Samericus_smile7474Belum ada peringkat

- 1349 1Dokumen6 halaman1349 1Noaman AkbarBelum ada peringkat

- MEC210 - Lecture 04 - 241Dokumen32 halamanMEC210 - Lecture 04 - 241Mina NasserBelum ada peringkat

- Valuation of SharesDokumen6 halamanValuation of SharesMargaret Socceroos KuiBelum ada peringkat

- HW 7Dokumen3 halamanHW 7Bandar Al-FaisalBelum ada peringkat

- Impact of Merger On Financial Performance of Nepalese Commercial BankDokumen4 halamanImpact of Merger On Financial Performance of Nepalese Commercial BankShrestha Photo studioBelum ada peringkat

- PPE Multiple Choice TestDokumen4 halamanPPE Multiple Choice TestRonna Mae ColminasBelum ada peringkat

- Accounting Ppe Quizzes PractoceDokumen1 halamanAccounting Ppe Quizzes PractoceMA. ANGELICA DARL DOMINGO CHAVEZBelum ada peringkat

- Ping An Insurance Stock ValuationDokumen11 halamanPing An Insurance Stock ValuationNile Alric Allado100% (1)

- Chapter 4 Financial Management IV BbaDokumen3 halamanChapter 4 Financial Management IV BbaSuchetana AnthonyBelum ada peringkat

- SBI@ Your Door StepDokumen2 halamanSBI@ Your Door StepDynamic LevelsBelum ada peringkat

- Parliamentary Committee Report Lok Sabha On Companies Bill 2011Dokumen111 halamanParliamentary Committee Report Lok Sabha On Companies Bill 2011anielnair5695Belum ada peringkat

- PTFC Redevelopment Corporation SEC Form 17-ADokumen261 halamanPTFC Redevelopment Corporation SEC Form 17-AqrqrqrqrqrqrqrqrqrBelum ada peringkat

- Mutual FundDokumen50 halamanMutual FundOmkar SutarBelum ada peringkat

- Total Current Liabilities: Balance Sheet of Pidilite Industries - in Rs. Cr.Dokumen4 halamanTotal Current Liabilities: Balance Sheet of Pidilite Industries - in Rs. Cr.Vishal GargBelum ada peringkat

- Muhammad Thoriq Nabawi Tugas 3 Chapter 1 BusinessDokumen9 halamanMuhammad Thoriq Nabawi Tugas 3 Chapter 1 BusinessThoriq NabawiBelum ada peringkat

- Advanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Dokumen23 halamanAdvanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Oyebisi OpeyemiBelum ada peringkat

- Fabm 1-PTDokumen12 halamanFabm 1-PTMaxene YbañezBelum ada peringkat

- Entrep 12 GASDokumen2 halamanEntrep 12 GASCamille ManlongatBelum ada peringkat

- Financial Performance AnalysisDokumen18 halamanFinancial Performance AnalysisVineet SwamiBelum ada peringkat

- Business PlanDokumen33 halamanBusiness PlanMarxy PanaguitonBelum ada peringkat

- Shipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Dokumen22 halamanShipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Luis Enrique LavayenBelum ada peringkat

- Faculty of Business, Finance & Information TechnologyDokumen13 halamanFaculty of Business, Finance & Information TechnologyNurBelum ada peringkat

- DLPCDokumen49 halamanDLPCthestorydotieBelum ada peringkat

- Contoh Soal - Ch15Dokumen52 halamanContoh Soal - Ch15Nurhanifah SoedarsBelum ada peringkat

- Basic Accounting TermsDokumen17 halamanBasic Accounting TermsNEONTechBelum ada peringkat

- Safari - Jul 12, 2019 at 2:32 PM PDFDokumen1 halamanSafari - Jul 12, 2019 at 2:32 PM PDFNick SitarasBelum ada peringkat

- ACTG Prelim ExamDokumen11 halamanACTG Prelim ExamRecruitment JMSStaffingBelum ada peringkat

- Questions FinanceDokumen3 halamanQuestions Financeanish narayanBelum ada peringkat

- Credit Risk Assessment 1 May 2011Dokumen5 halamanCredit Risk Assessment 1 May 2011Basilio MaliwangaBelum ada peringkat

- BW ControversyDokumen5 halamanBW ControversyJacquelyn RamosBelum ada peringkat

- Ratio Analysis About S.R. Steel IndustriesDokumen51 halamanRatio Analysis About S.R. Steel IndustriesshaileshBelum ada peringkat

- Faculty: Ms. Luvnica Rastogi Amity International Business School Imp WebsiteDokumen40 halamanFaculty: Ms. Luvnica Rastogi Amity International Business School Imp WebsiteRishad kBelum ada peringkat

- Promlem Solving Problem 1: Property, Plant and Equipment (Answer Key)Dokumen27 halamanPromlem Solving Problem 1: Property, Plant and Equipment (Answer Key)Rica Regoris100% (1)

- Jurnal Keuangan Saham Di Bursa EfekDokumen18 halamanJurnal Keuangan Saham Di Bursa Efeksaeful bakhriBelum ada peringkat