Anda mungkin juga menyukai

- 22mbr002-Sapm Mini ProjectDokumen23 halaman22mbr002-Sapm Mini ProjectABUBAKAR SIDIQ M 22MBR002Belum ada peringkat

- Regional Rural Banks of India: Evolution, Performance and ManagementDari EverandRegional Rural Banks of India: Evolution, Performance and ManagementBelum ada peringkat

- QT AssignmentDokumen24 halamanQT AssignmentAnika VarkeyBelum ada peringkat

- Camels Analysis of HDFC BankDokumen31 halamanCamels Analysis of HDFC Bankasifbhaiyat33% (3)

- Crisil Yearbook On The Indian Debt Market 2015.unlockedDokumen114 halamanCrisil Yearbook On The Indian Debt Market 2015.unlockedPRATIK JAINBelum ada peringkat

- Project Report: School of Business Oct 2012Dokumen29 halamanProject Report: School of Business Oct 2012aman7190hunkBelum ada peringkat

- Bajaj Finance Limited Q2 FY15 Presentation: 14 October 2014Dokumen33 halamanBajaj Finance Limited Q2 FY15 Presentation: 14 October 2014adi99123Belum ada peringkat

- Name: Kirti-S-DodejaDokumen15 halamanName: Kirti-S-DodejaMUKESH MANWANIBelum ada peringkat

- Yes BankDokumen30 halamanYes BankVivek PrakashBelum ada peringkat

- Financial Statement Analysis AssignmentDokumen19 halamanFinancial Statement Analysis AssignmentNajihah AdnanBelum ada peringkat

- Management Round Table 12 13Dokumen13 halamanManagement Round Table 12 13Rahul SaikiaBelum ada peringkat

- Bank and NBFC Mehal PDFDokumen38 halamanBank and NBFC Mehal PDFPrasun AgarwalBelum ada peringkat

- Swagat 2010 2011 Training BookletDokumen108 halamanSwagat 2010 2011 Training Bookletbitus92Belum ada peringkat

- Small Scale Industries ProjectDokumen64 halamanSmall Scale Industries ProjectDon Rocker100% (2)

- ICICI Group: Strategy & Performance: September 2011Dokumen42 halamanICICI Group: Strategy & Performance: September 2011helloashokBelum ada peringkat

- Executive SummaryDokumen84 halamanExecutive SummaryNeha SharmaBelum ada peringkat

- Banking and Insurance - Assignment: TopicDokumen16 halamanBanking and Insurance - Assignment: TopicVinay SharmaBelum ada peringkat

- 1939IIBF Vision April 2012Dokumen8 halaman1939IIBF Vision April 2012Shambhu KumarBelum ada peringkat

- Pubali Bnak LTDDokumen11 halamanPubali Bnak LTDZiaul HuqBelum ada peringkat

- Project On UCO Bank FinalDokumen69 halamanProject On UCO Bank FinalMilind Singh100% (1)

- NPA of Indian BanksDokumen27 halamanNPA of Indian BanksShristi GuptaBelum ada peringkat

- Idbi Bank: Presented By: Chetan Goel Meenakshi Surbhi Agarwal Pallavi TikooDokumen15 halamanIdbi Bank: Presented By: Chetan Goel Meenakshi Surbhi Agarwal Pallavi TikooChetan GoelBelum ada peringkat

- Eco ProjectDokumen28 halamanEco ProjectpraveentitareBelum ada peringkat

- Annual Report 2015Dokumen219 halamanAnnual Report 2015Hammad AhmadBelum ada peringkat

- Credit ManagementDokumen503 halamanCredit ManagementGudavalli John Raja Abhishek100% (1)

- Performance Analysis Mba ProjectDokumen64 halamanPerformance Analysis Mba ProjectShanmukhaSharmaBelum ada peringkat

- Annual Report 2009 10 EnglishDokumen106 halamanAnnual Report 2009 10 Englishrabi_shah_2Belum ada peringkat

- M.Phil. Student, MDU Rohtak Associate Professor, Dept. of Commerce Govt. College, BhiwaniDokumen2 halamanM.Phil. Student, MDU Rohtak Associate Professor, Dept. of Commerce Govt. College, BhiwaniAmandeep Singh MankuBelum ada peringkat

- ExtraDokumen12 halamanExtraSujit Kumar YadavBelum ada peringkat

- Monetary Policy of IndiaDokumen5 halamanMonetary Policy of IndiaSudesh SharmaBelum ada peringkat

- Final ReportDokumen52 halamanFinal ReportIshwar ChhedaBelum ada peringkat

- ICICI Bank - ProjectDokumen17 halamanICICI Bank - ProjectTejasvi KatiraBelum ada peringkat

- 2014 09 Clsa Conference PresentationDokumen67 halaman2014 09 Clsa Conference PresentationTara Ann CoelhoBelum ada peringkat

- Commercial Bank in India: Public Sector Private Sector Foreign SectorDokumen13 halamanCommercial Bank in India: Public Sector Private Sector Foreign SectorAshish SharmaBelum ada peringkat

- Ratio Analysis of HDFC FINALDokumen10 halamanRatio Analysis of HDFC FINALJAYKISHAN JOSHI100% (2)

- ICICI Bank Annual Report FY2010Dokumen196 halamanICICI Bank Annual Report FY2010Naresh RvBelum ada peringkat

- HDFC May12 07 All LoanDokumen52 halamanHDFC May12 07 All Loanjohn_muellorBelum ada peringkat

- Table of Content: HDFC BankDokumen23 halamanTable of Content: HDFC BankSyedBelum ada peringkat

- Analysis of Business Environment of Top 5 Banks - PPT 2.Ppt 1Dokumen16 halamanAnalysis of Business Environment of Top 5 Banks - PPT 2.Ppt 1Shanky DargeBelum ada peringkat

- Posted: Sat Feb 03, 2007 1:58 PM Post Subject: Causes For Non-Performing Assets in Public Sector BanksDokumen13 halamanPosted: Sat Feb 03, 2007 1:58 PM Post Subject: Causes For Non-Performing Assets in Public Sector BanksSimer KaurBelum ada peringkat

- Initiating Coverage Report - YES BankDokumen35 halamanInitiating Coverage Report - YES Bankarnabmoitra11Belum ada peringkat

- International Financial Statement AnalysisDari EverandInternational Financial Statement AnalysisPenilaian: 1 dari 5 bintang1/5 (1)

- CamelDokumen10 halamanCamelSimki JainBelum ada peringkat

- Idbi McomDokumen82 halamanIdbi McomShweta GuptaBelum ada peringkat

- Yes Bank Equity AnalysisDokumen4 halamanYes Bank Equity AnalysisShaloo MinzBelum ada peringkat

- Equity Research: (Series IV) 10th August 2012Dokumen18 halamanEquity Research: (Series IV) 10th August 2012kgsbppBelum ada peringkat

- Jan Mar 2007 BulletinDokumen17 halamanJan Mar 2007 BulletinAyeshaJangdaBelum ada peringkat

- An Insight On The Financials of The 3 Largest Public Sector Bank in India Presented By: Group 8 Section A Mba-Jan 13Dokumen22 halamanAn Insight On The Financials of The 3 Largest Public Sector Bank in India Presented By: Group 8 Section A Mba-Jan 13Mohit BatraBelum ada peringkat

- UntitledDokumen376 halamanUntitledpoobalanipbBelum ada peringkat

- NRB Regulation of Bank. Group BBBBBBBBBBBBBBDokumen37 halamanNRB Regulation of Bank. Group BBBBBBBBBBBBBBMohan BanjaraBelum ada peringkat

- Assignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryDokumen9 halamanAssignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryRohit VermaBelum ada peringkat

- Debt Recovery ManagementDokumen15 halamanDebt Recovery Managementpranjalamishra100% (1)

- Banking, Financial Services and Insurance: Unnati Sector PresentationDokumen48 halamanBanking, Financial Services and Insurance: Unnati Sector PresentationPradeep VarshneyBelum ada peringkat

- Credit Management of BankDokumen83 halamanCredit Management of BankNil DasBelum ada peringkat

- Reliance Money ProjectDokumen52 halamanReliance Money ProjectShreya AgarwalBelum ada peringkat

- CAMEL AnalysisDokumen11 halamanCAMEL AnalysisChirag AbrolBelum ada peringkat

- Benchmarking: Practices and Tools For Achieving International Standards in Banking Sector To Overcome The Economic CrisisDokumen29 halamanBenchmarking: Practices and Tools For Achieving International Standards in Banking Sector To Overcome The Economic Crisissadik953Belum ada peringkat

- The Handbook of Global Corporate TreasuryDari EverandThe Handbook of Global Corporate TreasuryPenilaian: 4 dari 5 bintang4/5 (1)

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Dari EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Belum ada peringkat

- Emerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaDari EverandEmerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaBelum ada peringkat

- Solar Farm Business Plan ExampleDokumen34 halamanSolar Farm Business Plan Examplejackson jimBelum ada peringkat

- BBA Major ProjectDokumen40 halamanBBA Major ProjectDeepak Bhatia100% (5)

- A Corporate BondDokumen2 halamanA Corporate BondMuhammad KhurramBelum ada peringkat

- Characteristics of The Islamic EconomyDokumen3 halamanCharacteristics of The Islamic EconomyJuliyana Jamal100% (3)

- Employees' Provident Fund Scheme: (0.18 %)Dokumen9 halamanEmployees' Provident Fund Scheme: (0.18 %)Shubhabrata BanerjeeBelum ada peringkat

- Annual Report PPFDokumen71 halamanAnnual Report PPFBhuvanesh Narayana SamyBelum ada peringkat

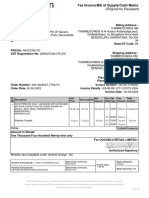

- InvoiceDokumen2 halamanInvoiceTHIMMEGOWDA H MBelum ada peringkat

- Ratio & RateDokumen2 halamanRatio & RateWilliam RyandinataBelum ada peringkat

- Unit Test 5Dokumen6 halamanUnit Test 5Madalina Fira0% (1)

- Problem 10Dokumen2 halamanProblem 10novyBelum ada peringkat

- Audit of Property, Plant and Equipment: Auditing ProblemsDokumen5 halamanAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanBelum ada peringkat

- Accounting Midterm ExamDokumen3 halamanAccounting Midterm ExamJhon OrtizBelum ada peringkat

- Saima Jabeen AkhandaDokumen70 halamanSaima Jabeen AkhandaAhnaf AhmedBelum ada peringkat

- Deber 3Dokumen5 halamanDeber 3MartinBelum ada peringkat

- Money-Time Relationships: PrinciplesDokumen32 halamanMoney-Time Relationships: Principlesimran_chaudhryBelum ada peringkat

- Coca ColaDokumen13 halamanCoca Colaramonese100% (2)

- Sundiang Notes - InsuranceDokumen70 halamanSundiang Notes - InsuranceJeperson Marco100% (9)

- Complete Annual Report 2006Dokumen70 halamanComplete Annual Report 2006sunny_fzBelum ada peringkat

- Perpetual - Financial StatementsDokumen4 halamanPerpetual - Financial StatementsJeon Cyrone CuachonBelum ada peringkat

- PRED 3210 Chapter 4Dokumen8 halamanPRED 3210 Chapter 4Jheny PalamaraBelum ada peringkat

- SK Illustrative Problems - For All SessionsDokumen6 halamanSK Illustrative Problems - For All SessionsLea Mae JenBelum ada peringkat

- Galgotias University Vishwajeet Singh S/O Kuldeep SinghDokumen1 halamanGalgotias University Vishwajeet Singh S/O Kuldeep SinghAashika SinghBelum ada peringkat

- Derivatives and Risk ManagementDokumen5 halamanDerivatives and Risk ManagementabhishekrameshnagBelum ada peringkat

- BA Tutorial Schedule Spring 2021Dokumen8 halamanBA Tutorial Schedule Spring 2021Usama JavaidBelum ada peringkat

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokumen1 halamanTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)raviBelum ada peringkat

- Miga Professionals Program PDFDokumen2 halamanMiga Professionals Program PDFPaul Ivan Beppe a Yombo Paul IvanBelum ada peringkat

- ACCT2102 - G-I - 2018-19 - Ch.3 - 12-13 FebDokumen4 halamanACCT2102 - G-I - 2018-19 - Ch.3 - 12-13 FebAlfieBelum ada peringkat

- AFS SolutionsDokumen19 halamanAFS SolutionsRolivhuwaBelum ada peringkat

- Commerzbank AG: Issuer Rating ReportDokumen12 halamanCommerzbank AG: Issuer Rating ReportvaishnaviBelum ada peringkat

- Application For Tata Genuine Parts Distributorship For Commercial VehiclesDokumen17 halamanApplication For Tata Genuine Parts Distributorship For Commercial VehiclesNayaz UddinBelum ada peringkat