Anda mungkin juga menyukai

- CFA Formula Cheat SheetDokumen9 halamanCFA Formula Cheat SheetChingWa ChanBelum ada peringkat

- 0 - AFAR.002 Partnership Dissolution and Liquidation - 2106158851 PDFDokumen9 halaman0 - AFAR.002 Partnership Dissolution and Liquidation - 2106158851 PDFIan RanilopaBelum ada peringkat

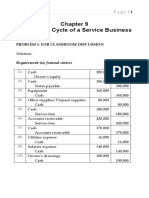

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDokumen52 halamanSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- CFAS 06 PAS 8 Accounting Policies Estimates and ErrorsDokumen4 halamanCFAS 06 PAS 8 Accounting Policies Estimates and ErrorsJanine WayanBelum ada peringkat

- Accounting Policies and ErrorsDokumen32 halamanAccounting Policies and ErrorsTia Li100% (1)

- CFA Level I Formula SheetDokumen27 halamanCFA Level I Formula SheetAnonymous P1xUTHstHT100% (4)

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018Dari EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Belum ada peringkat

- Accounting Policies Changes in Accounting Estimates and Errors IAS 8Dokumen16 halamanAccounting Policies Changes in Accounting Estimates and Errors IAS 8Akash RanaBelum ada peringkat

- MFRS 108 Changes in Accounting PoliciesDokumen21 halamanMFRS 108 Changes in Accounting Policiesnatasha thaiBelum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen21 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsEshetie Mekonene AmareBelum ada peringkat

- Adjusting Entries - Sample Problem With AnswerDokumen19 halamanAdjusting Entries - Sample Problem With AnswerMaDine 19100% (3)

- ACCA F7 Combined Technical Articles D16Dokumen92 halamanACCA F7 Combined Technical Articles D16Ivan Ivanov100% (1)

- Mathematical EconomicsDokumen80 halamanMathematical EconomicsChuzenBelum ada peringkat

- Mercury AthleticDokumen13 halamanMercury Athleticarnabpramanik100% (1)

- Exercise CH3Dokumen10 halamanExercise CH3loveshareBelum ada peringkat

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Dokumen33 halamanReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydBelum ada peringkat

- Indian Accounting Standard (Ind AS) 8 - Taxguru - inDokumen11 halamanIndian Accounting Standard (Ind AS) 8 - Taxguru - inaaosarlbBelum ada peringkat

- Indian Accounting Standard (Ind AS) 8: Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen19 halamanIndian Accounting Standard (Ind AS) 8: Accounting Policies, Changes in Accounting Estimates and ErrorsAnkush GoelBelum ada peringkat

- Ias No.8Dokumen41 halamanIas No.8rafikaBelum ada peringkat

- Nepal Accounting Standards On Accounting Policies, Changes in Accounting Estimates & ErrorsDokumen25 halamanNepal Accounting Standards On Accounting Policies, Changes in Accounting Estimates & Errorsshama_rana20036778Belum ada peringkat

- Exp Posure D Draft: A Accounti Ing Stan Ndard (A AS) 5 (Re Evised)Dokumen15 halamanExp Posure D Draft: A Accounti Ing Stan Ndard (A AS) 5 (Re Evised)ratiBelum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen14 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsSuresh Reddy SannapureddyBelum ada peringkat

- Ias 8Dokumen9 halamanIas 8Muhammad SaeedBelum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen15 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsPriya JandialBelum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen25 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsAshish agrawalBelum ada peringkat

- IAS 8 Diana Maruf AnasDokumen24 halamanIAS 8 Diana Maruf AnasLamis ShalabiBelum ada peringkat

- Lkas 8 Accounting Policies Changes in Accounting Estimates and ErrorsDokumen18 halamanLkas 8 Accounting Policies Changes in Accounting Estimates and ErrorsW V C JAYAMINIBelum ada peringkat

- Ias8 PDFDokumen3 halamanIas8 PDFNozipho MpofuBelum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen9 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsMaruf HossainBelum ada peringkat

- Ias 8 EnglezaDokumen9 halamanIas 8 EnglezaTatiana LupuBelum ada peringkat

- IAS8Dokumen2 halamanIAS8Atif RehmanBelum ada peringkat

- IAS 8 Accounting Policies, Changes In: Accounting Estimates and ErrorsDokumen2 halamanIAS 8 Accounting Policies, Changes In: Accounting Estimates and ErrorsAKINYEMI ADISA KAMORUBelum ada peringkat

- 21.0 NAS 8 - SetPasswordDokumen9 halaman21.0 NAS 8 - SetPasswordDhruba AdhikariBelum ada peringkat

- Accounting For Changes and ErrorsDokumen7 halamanAccounting For Changes and ErrorsMeludyBelum ada peringkat

- Chapter 5 PAS 8 Accounting Policies, Changes in Accouting Estimates and ErrorsDokumen12 halamanChapter 5 PAS 8 Accounting Policies, Changes in Accouting Estimates and ErrorsSimon RavanaBelum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen18 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsSineth NeththasingheBelum ada peringkat

- Module 014 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen9 halamanModule 014 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and Errorsman ibeBelum ada peringkat

- LKAS 8 Accounting Policies (New)Dokumen33 halamanLKAS 8 Accounting Policies (New)Kogularamanan NithiananthanBelum ada peringkat

- Pas 8 Cfas PDFDokumen6 halamanPas 8 Cfas PDFAndreaaAAaa TagleBelum ada peringkat

- Accounting Policy and Estimate IAS 8Dokumen6 halamanAccounting Policy and Estimate IAS 8OLAWALE AFOLABI TIMOTHYBelum ada peringkat

- Ias 8 Accounting Policies Changes in Accounting Estimates and Errors SummaryDokumen5 halamanIas 8 Accounting Policies Changes in Accounting Estimates and Errors SummaryWilmar AbriolBelum ada peringkat

- Change in Accounting Policy, Estimates and Error PAS 8Dokumen17 halamanChange in Accounting Policy, Estimates and Error PAS 8RBelum ada peringkat

- As-1 Disclosure of Accounting PoliciesDokumen7 halamanAs-1 Disclosure of Accounting PoliciesPrakash_Tandon_583Belum ada peringkat

- As 8 Alc PoliciesDokumen50 halamanAs 8 Alc PoliciesAkhil AkhyBelum ada peringkat

- IAS8Dokumen2 halamanIAS8chehirBelum ada peringkat

- IAS-8 Accounting Policies, Change in Accounting Estimates and Errors ObjectiveDokumen6 halamanIAS-8 Accounting Policies, Change in Accounting Estimates and Errors ObjectiveAbdullah Al Amin MubinBelum ada peringkat

- Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen27 halamanIas 8 Accounting Policies, Changes in Accounting Estimates and ErrorsMK RKBelum ada peringkat

- 74888bos60524 cp4 U1Dokumen50 halaman74888bos60524 cp4 U1Bala Guru Prasad TadikamallaBelum ada peringkat

- NAS 8 - Best SummaryDokumen5 halamanNAS 8 - Best Summarysitoulamanish100Belum ada peringkat

- 8 Policy, Estimate, ErrorDokumen16 halaman8 Policy, Estimate, ErrorChelsea Anne VidalloBelum ada peringkat

- Accounting Standard 1Dokumen7 halamanAccounting Standard 1api-3828505Belum ada peringkat

- Chapter 11 Accounting Policies PDFDokumen8 halamanChapter 11 Accounting Policies PDFAthena LansangBelum ada peringkat

- IND AS 8 Raw PDFDokumen41 halamanIND AS 8 Raw PDFrajesh reddyBelum ada peringkat

- Ind As On Measurement Based On Accounting PoliciesDokumen38 halamanInd As On Measurement Based On Accounting Policiespulkitddude_24114888Belum ada peringkat

- Accounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesDokumen5 halamanAccounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesSuhasini GummeBelum ada peringkat

- Ias 8Dokumen47 halamanIas 8অরূপ মিস্ত্রী বলেছেনBelum ada peringkat

- Ibtisam MurtazaDokumen4 halamanIbtisam MurtazaMR ABelum ada peringkat

- Disclosure of Accounting PoliciesDokumen8 halamanDisclosure of Accounting Policiesabdullah0331Belum ada peringkat

- Finance Project PrintDokumen23 halamanFinance Project PrintYash ParekhBelum ada peringkat

- Document 2Dokumen8 halamanDocument 2sohamBelum ada peringkat

- FRS 18, Accounting PoliciesDokumen8 halamanFRS 18, Accounting PoliciesveemaswBelum ada peringkat

- Accounting Policy Options in IFRSDokumen11 halamanAccounting Policy Options in IFRSSaiful Iksan PratamaBelum ada peringkat

- Accounting Standard (AS) 1: (Issued 1979)Dokumen7 halamanAccounting Standard (AS) 1: (Issued 1979)anoop_mishra1986Belum ada peringkat

- Disclosure of Accounting PoliciesDokumen7 halamanDisclosure of Accounting PoliciesgimmyjoyBelum ada peringkat

- IFA II Chap - 5 2016Dokumen15 halamanIFA II Chap - 5 2016teddymaru7Belum ada peringkat

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokumen29 halamanAccounting Policies, Changes in Accounting Estimates and ErrorsSheda AshrafBelum ada peringkat

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsDari EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsBelum ada peringkat

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsDari EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsBelum ada peringkat

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18Dari EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18Belum ada peringkat

- Block 4 MS 91 Unit 2Dokumen25 halamanBlock 4 MS 91 Unit 2Anonymous P1xUTHstHTBelum ada peringkat

- Block-4 MS-91 Unit-4 PDFDokumen24 halamanBlock-4 MS-91 Unit-4 PDFAnonymous P1xUTHstHTBelum ada peringkat

- Unit 14 Strategy and Social Responsibility: ObjectivesDokumen13 halamanUnit 14 Strategy and Social Responsibility: ObjectivesAnonymous P1xUTHstHTBelum ada peringkat

- Block 3 MS 91 Unit 1Dokumen11 halamanBlock 3 MS 91 Unit 1Anonymous P1xUTHstHTBelum ada peringkat

- Block 4 MS 91 Unit 5Dokumen11 halamanBlock 4 MS 91 Unit 5Anonymous P1xUTHstHTBelum ada peringkat

- Guide Utilisation Calculatrice Ang PDFDokumen17 halamanGuide Utilisation Calculatrice Ang PDFFLORAILEENBelum ada peringkat

- Finance Reading List PHDDokumen8 halamanFinance Reading List PHDAnonymous P1xUTHstHTBelum ada peringkat

- Noncurrent AssetsDokumen90 halamanNoncurrent Assetsfira tuapetelBelum ada peringkat

- CJ - Credit SuiseDokumen24 halamanCJ - Credit Suisebackup tringuyenBelum ada peringkat

- Chap 17 Intercompany Sales of InventoryDokumen71 halamanChap 17 Intercompany Sales of InventoryPhrexilyn PajarilloBelum ada peringkat

- Acct 310 Final Exam (Umuc)Dokumen10 halamanAcct 310 Final Exam (Umuc)OmarNiemczykBelum ada peringkat

- Chapter 5Dokumen53 halamanChapter 5임재영Belum ada peringkat

- ICARE First Preboard AFARDokumen17 halamanICARE First Preboard AFARaceBelum ada peringkat

- Fasb 143 PDFDokumen2 halamanFasb 143 PDFRenesikxs0% (1)

- Hala Arrabi Managerial Finance Assignment Chapter 3-Part 1 Multiple Choice QuestionsDokumen3 halamanHala Arrabi Managerial Finance Assignment Chapter 3-Part 1 Multiple Choice QuestionsMohamad Haytham ElturkBelum ada peringkat

- Accounting Chapter 2Dokumen56 halamanAccounting Chapter 2hnhBelum ada peringkat

- Monthly Reports ETCDokumen22 halamanMonthly Reports ETCwnicoloffBelum ada peringkat

- Sandip Voltas ReportDokumen43 halamanSandip Voltas ReportsandipBelum ada peringkat

- Marvin Barro - Week 1Dokumen24 halamanMarvin Barro - Week 1jakBelum ada peringkat

- KHIND Annual Report MalaysiaDokumen77 halamanKHIND Annual Report MalaysiakokueiBelum ada peringkat

- Financial Analysis Part 4Dokumen9 halamanFinancial Analysis Part 4Llyod Francis LaylayBelum ada peringkat

- Q1 LAS 4 FABM2 12 Week 2 3Dokumen7 halamanQ1 LAS 4 FABM2 12 Week 2 3Flare ColterizoBelum ada peringkat

- Flat CargoDokumen26 halamanFlat CargoSherry Yong PkTianBelum ada peringkat

- LKFS BR 31 March 0908 (Final)Dokumen116 halamanLKFS BR 31 March 0908 (Final)wdr80Belum ada peringkat

- Pembahasan Contoh Soal Matrikulasi Day 2Dokumen5 halamanPembahasan Contoh Soal Matrikulasi Day 2valdaBelum ada peringkat

- ch20 (改)Dokumen21 halamanch20 (改)林義哲Belum ada peringkat

- QRDokumen5 halamanQRnateBelum ada peringkat

- CFAS Chap 4Dokumen16 halamanCFAS Chap 4Jansen Alonzo Bordey100% (1)

- Financial Statements 1Dokumen19 halamanFinancial Statements 1bhawnaBelum ada peringkat

- Solutions Guide: Please Reword The Answers To Essay Type Parts So As To Guarantee That Your Answer Is An Original. Do Not Submit As Your OwnDokumen6 halamanSolutions Guide: Please Reword The Answers To Essay Type Parts So As To Guarantee That Your Answer Is An Original. Do Not Submit As Your OwnSkarlz ZyBelum ada peringkat

- Poppy Petals Activity Periodic InventoryDokumen18 halamanPoppy Petals Activity Periodic InventoryPhil-Wave Boat Builder Co. Ltd.Belum ada peringkat