Anda mungkin juga menyukai

- Spurwing Greens Community FlyerDokumen2 halamanSpurwing Greens Community FlyerJeremy EricksonBelum ada peringkat

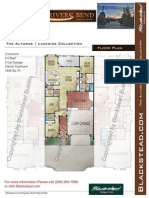

- Alturas at Lakeside CollectionDokumen1 halamanAlturas at Lakeside CollectionJeremy EricksonBelum ada peringkat

- AlderDokumen1 halamanAlderJeremy EricksonBelum ada peringkat

- CE Community Flyer 1-21-2012Dokumen2 halamanCE Community Flyer 1-21-2012Jeremy EricksonBelum ada peringkat

- Highlight Video Creation Worksheet You Can Also Email ToDokumen3 halamanHighlight Video Creation Worksheet You Can Also Email ToJeremy EricksonBelum ada peringkat

- Ada Resale Market Report Jan 8th 2010Dokumen4 halamanAda Resale Market Report Jan 8th 2010Jeremy EricksonBelum ada peringkat

- Mortgagee Letter 2010-02Dokumen2 halamanMortgagee Letter 2010-02Jeremy EricksonBelum ada peringkat

- Ada New Construction Market Report Jan 2010Dokumen9 halamanAda New Construction Market Report Jan 2010Jeremy EricksonBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- PremiumReceipt 03128410 1638813565Dokumen1 halamanPremiumReceipt 03128410 1638813565Arpit GulhaneBelum ada peringkat

- Chapter 1 & 2 (PPT) - Introduction To Monetary Policy and Central BankingDokumen22 halamanChapter 1 & 2 (PPT) - Introduction To Monetary Policy and Central BankingCARMELA SUMAYOPBelum ada peringkat

- Tata Consultancy Services Payslip JAN2023Dokumen1 halamanTata Consultancy Services Payslip JAN2023Mainak BhattacharjeeBelum ada peringkat

- Class Xii CH 7 MCQ AccountancyDokumen16 halamanClass Xii CH 7 MCQ AccountancyhanaBelum ada peringkat

- Internship Rahul SBLDokumen75 halamanInternship Rahul SBLMùkésh RôyBelum ada peringkat

- 01activity Borrowing WorkbookDokumen12 halaman01activity Borrowing WorkbookMatthewBelum ada peringkat

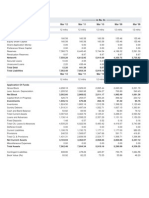

- Balance Sheet and P&L of CiplaDokumen2 halamanBalance Sheet and P&L of CiplaPratik AhluwaliaBelum ada peringkat

- Lecture-11 Compound Interest)Dokumen2 halamanLecture-11 Compound Interest)Aditya SahaBelum ada peringkat

- Simple and Compound Interest: Concept of Time and Value OfmoneyDokumen11 halamanSimple and Compound Interest: Concept of Time and Value OfmoneyUnzila AtiqBelum ada peringkat

- PAWNSHOPSDokumen1 halamanPAWNSHOPSBianca SiguenzaBelum ada peringkat

- Customer AttendanceDokumen3 halamanCustomer Attendancejsl2001Belum ada peringkat

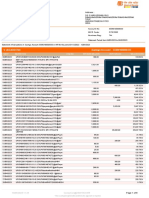

- OpTransactionHistoryUX510 05 2023Dokumen8 halamanOpTransactionHistoryUX510 05 2023Jagadeesh SuraBelum ada peringkat

- Mortgage ReviewerDokumen5 halamanMortgage ReviewerRosalia L. Completano LptBelum ada peringkat

- Yuson Vs Atty Vitan Dacion en PagsDokumen2 halamanYuson Vs Atty Vitan Dacion en PagsVen BuenaobraBelum ada peringkat

- Some Thoughts On The Failure of Silicon Valley Bank 3-12-2023Dokumen4 halamanSome Thoughts On The Failure of Silicon Valley Bank 3-12-2023Subash NehruBelum ada peringkat

- Pension Mathematics With Numerical Illustrations: Second EditionDokumen13 halamanPension Mathematics With Numerical Illustrations: Second EditionG.k. FlorentBelum ada peringkat

- CERTIFICATE For Claiming Deduction Under Section 24 (B) & 80C (2) (Xviii) of INCOME TAX ACT, 1961Dokumen1 halamanCERTIFICATE For Claiming Deduction Under Section 24 (B) & 80C (2) (Xviii) of INCOME TAX ACT, 1961Raman SharmaBelum ada peringkat

- Chap 020Dokumen76 halamanChap 020NitinBelum ada peringkat

- 1099-R Copy B: CORRECTED (If Checked)Dokumen6 halaman1099-R Copy B: CORRECTED (If Checked)Dave MBelum ada peringkat

- PRO0xxx FG Pension V4 BrochureDokumen8 halamanPRO0xxx FG Pension V4 Brochurecoinage capitalBelum ada peringkat

- Commissions and Interests: Lesson 1: InterestDokumen9 halamanCommissions and Interests: Lesson 1: InterestAxl Fitzgerald BulawanBelum ada peringkat

- T3 - ABFA1153 (Extra)Dokumen3 halamanT3 - ABFA1153 (Extra)LOO YU HUANGBelum ada peringkat

- Dispute FormDokumen1 halamanDispute Formuzair muhdBelum ada peringkat

- Rules On Gross Income TaxationDokumen15 halamanRules On Gross Income TaxationEar TanBelum ada peringkat

- A Study On Plastic MoneyDokumen43 halamanA Study On Plastic MoneyxcvBelum ada peringkat

- Retirement PlansDokumen10 halamanRetirement PlansGene'sBelum ada peringkat

- Text 1Dokumen11 halamanText 1Ray Joshua Angcan BalingkitBelum ada peringkat

- SAF11646 SalarySlip August 2023Dokumen1 halamanSAF11646 SalarySlip August 2023akashBelum ada peringkat

- Payment Method: Bank Transfer, Account Number: 50100498022296, Bank Name:HDFCDokumen1 halamanPayment Method: Bank Transfer, Account Number: 50100498022296, Bank Name:HDFCBADI APPALARAJUBelum ada peringkat

- Real Estate MortgageDokumen4 halamanReal Estate MortgageJoy TagleBelum ada peringkat