Anda mungkin juga menyukai

- The Foreigner Audition Information KitDokumen2 halamanThe Foreigner Audition Information KitjnatchBelum ada peringkat

- Understanding Death Through the Life SpanDokumen52 halamanUnderstanding Death Through the Life SpanKaren HernandezBelum ada peringkat

- OCFINALEXAM2019Dokumen6 halamanOCFINALEXAM2019DA FT100% (1)

- Pratt & Whitney Engine Training ResourcesDokumen5 halamanPratt & Whitney Engine Training ResourcesJulio Abanto50% (2)

- Global High Temperature Grease Market ReportDokumen6 halamanGlobal High Temperature Grease Market ReportHari PurwadiBelum ada peringkat

- International History 1900-99Dokumen5 halamanInternational History 1900-99rizalmusthofa100% (1)

- Officers Ias Academy: (India's Only Academy Run by An IAS Officer) Economic Outlook, Prospects, and Policy ChallengesDokumen22 halamanOfficers Ias Academy: (India's Only Academy Run by An IAS Officer) Economic Outlook, Prospects, and Policy ChallengesArvind HarikrishnanBelum ada peringkat

- Grant Thornton Analaysis-Budget 2013-14Dokumen39 halamanGrant Thornton Analaysis-Budget 2013-14Kazmi Uzair SultanBelum ada peringkat

- Expenditure Management CommissionDokumen36 halamanExpenditure Management CommissionaronBelum ada peringkat

- BudgetDokumen3 halamanBudgetqewqdwfeBelum ada peringkat

- Economic Survey 2015 SummaryDokumen41 halamanEconomic Survey 2015 SummaryMohit JangidBelum ada peringkat

- Budget Recommendations NationalDokumen5 halamanBudget Recommendations NationalAyushRajBelum ada peringkat

- Di New Pattern BFPDokumen245 halamanDi New Pattern BFPDeepak LohiaBelum ada peringkat

- Present State of Goods and Services Tax (GST) Reform in IndiaDokumen24 halamanPresent State of Goods and Services Tax (GST) Reform in IndiaResuf AhmedBelum ada peringkat

- Envisioning Tax Policy: For Accelerated Development in IndiaDokumen22 halamanEnvisioning Tax Policy: For Accelerated Development in IndiaArya SBelum ada peringkat

- Strategy White PaperDokumen16 halamanStrategy White PaperVishnupriya SharmaBelum ada peringkat

- Impact of Budget 2014-15 on key sectorsDokumen4 halamanImpact of Budget 2014-15 on key sectorsRaj AraBelum ada peringkat

- Personal Income Tax in India A Roadmap For FutureDokumen4 halamanPersonal Income Tax in India A Roadmap For FutureEditor IJTSRDBelum ada peringkat

- Improving long term-growth prospects will help revive investmentDokumen79 halamanImproving long term-growth prospects will help revive investmentashokavikramadityaBelum ada peringkat

- EconomicSurvey2014 15Dokumen22 halamanEconomicSurvey2014 15tbharathkumarreddy3081Belum ada peringkat

- India Union Budget 2011: "Quality Service Is Not What You Put Into It - It's What The Client Gets Out of It"Dokumen41 halamanIndia Union Budget 2011: "Quality Service Is Not What You Put Into It - It's What The Client Gets Out of It"Jacob JheraldBelum ada peringkat

- Budget 2011Dokumen4 halamanBudget 2011viv_nitjBelum ada peringkat

- Highlights of Union Budget 2011-12 Quotes and ReformsDokumen15 halamanHighlights of Union Budget 2011-12 Quotes and ReformsrahulssitBelum ada peringkat

- New Era, New Hopes - The Indian Market and Economy in The Upcoming YearsDokumen4 halamanNew Era, New Hopes - The Indian Market and Economy in The Upcoming YearsBhavya GautamBelum ada peringkat

- Economic Survey 2015-16 highlights key challenges facing Indian economyDokumen1 halamanEconomic Survey 2015-16 highlights key challenges facing Indian economyAspirant NewbieBelum ada peringkat

- Fiscal Policy of India - Almost FinalDokumen30 halamanFiscal Policy of India - Almost FinalBhagyashree SatheBelum ada peringkat

- Driving Growth Union Budget 2023 24Dokumen25 halamanDriving Growth Union Budget 2023 24shwetaBelum ada peringkat

- IBPS PO Mains Memory Based 2016 (English) : WWW - Careerpower.in WWW - Careeradda.co - inDokumen9 halamanIBPS PO Mains Memory Based 2016 (English) : WWW - Careerpower.in WWW - Careeradda.co - inPriyanshu JainBelum ada peringkat

- KPMG Union Budget 2014Dokumen32 halamanKPMG Union Budget 2014Ashish KediaBelum ada peringkat

- Indian BudgetDokumen60 halamanIndian BudgetNirav SolankiBelum ada peringkat

- Darshini Gayithri 2023 An Econometric Analysis of Revenue Diversification Among Selected Indian StatesDokumen23 halamanDarshini Gayithri 2023 An Econometric Analysis of Revenue Diversification Among Selected Indian StatessushilBelum ada peringkat

- Key Features of Budget 2012-2013Dokumen15 halamanKey Features of Budget 2012-2013anupbhansali2004Belum ada peringkat

- Bold Step Towards 5 Trillion Economy: CMA Bhogavalli Mallikarjuna GuptaDokumen3 halamanBold Step Towards 5 Trillion Economy: CMA Bhogavalli Mallikarjuna GuptavenkannaBelum ada peringkat

- Impact of Budget 2016 On Indian IndustryDokumen13 halamanImpact of Budget 2016 On Indian IndustryAsutosh PatroBelum ada peringkat

- Power Infra 2Dokumen2 halamanPower Infra 2siddharth_nptiBelum ada peringkat

- Key Features of Budget 2014Dokumen5 halamanKey Features of Budget 2014Roxanne AyalaBelum ada peringkat

- Growth and DevelopmentDokumen12 halamanGrowth and DevelopmentRahul BaggaBelum ada peringkat

- Monthly - April - 2015Dokumen56 halamanMonthly - April - 2015Akshaj ShahBelum ada peringkat

- Union Budget 2010-2011: Presented byDokumen44 halamanUnion Budget 2010-2011: Presented bynishantmeBelum ada peringkat

- STRATEGY FOR NEW INDIA - DriversDokumen156 halamanSTRATEGY FOR NEW INDIA - DriversNarine D'souzaBelum ada peringkat

- Insights Daily Current Events, 27 February 2016: Topic: Indian Economy - Growth and DevelopmentDokumen10 halamanInsights Daily Current Events, 27 February 2016: Topic: Indian Economy - Growth and DevelopmentRakesh KumarBelum ada peringkat

- Priority-For-Policy - HTML: Page - 1Dokumen12 halamanPriority-For-Policy - HTML: Page - 1Kathryn TeoBelum ada peringkat

- Budget BOOK FinalDokumen19 halamanBudget BOOK FinalAmin ChhipaBelum ada peringkat

- Union Budget 2011-12: HighlightsDokumen14 halamanUnion Budget 2011-12: HighlightsNDTVBelum ada peringkat

- Economic Survey 2019 HighlightsDokumen13 halamanEconomic Survey 2019 HighlightsThe Indian Express100% (2)

- BudgetDokumen6 halamanBudgetPriyanka DaveBelum ada peringkat

- Budget Plan Financial GuidelineDokumen12 halamanBudget Plan Financial GuidelineRahul DubeyBelum ada peringkat

- Anshul MittalDokumen11 halamanAnshul Mittalaakkii028Belum ada peringkat

- Budget Analysis-2012 - T.P Ostwal & AssociatesDokumen115 halamanBudget Analysis-2012 - T.P Ostwal & AssociatesvaidheiBelum ada peringkat

- Highlights of Budget 2009-10Dokumen13 halamanHighlights of Budget 2009-10chauhanaimt38Belum ada peringkat

- Budget 2011-12 - Analysis: Tax ProjectDokumen19 halamanBudget 2011-12 - Analysis: Tax ProjectSaurabh SadaniBelum ada peringkat

- Areas of Concern in IndiaDokumen17 halamanAreas of Concern in IndiaElle Gio CasibangBelum ada peringkat

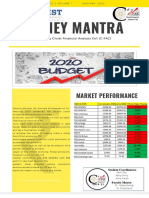

- Money Mantra: Market PerformanceDokumen4 halamanMoney Mantra: Market PerformanceAlbin SibyBelum ada peringkat

- Present State of Goods and Services Tax (GST) Reform in IndiaDokumen24 halamanPresent State of Goods and Services Tax (GST) Reform in IndiaKuberBelum ada peringkat

- Present State of Goods and Services Tax (GST) Reform in IndiaDokumen24 halamanPresent State of Goods and Services Tax (GST) Reform in Indiashubham jagtapBelum ada peringkat

- Literature Review of Taxation in IndiaDokumen4 halamanLiterature Review of Taxation in Indiac5hzgcdj100% (1)

- 48 National Cost Convention, 2007: Inaugural Address On Sustaining The Higher GrowthDokumen8 halaman48 National Cost Convention, 2007: Inaugural Address On Sustaining The Higher Growthapi-3705877Belum ada peringkat

- Time Series Analysis Between GDCF and GDPDokumen15 halamanTime Series Analysis Between GDCF and GDPRohit BarveBelum ada peringkat

- Hyderabad keeps business-friendly tag; India's ease of doing business ranking improvesDokumen27 halamanHyderabad keeps business-friendly tag; India's ease of doing business ranking improvesHimanshu GuptaBelum ada peringkat

- Crux 3.0 - 01Dokumen12 halamanCrux 3.0 - 01Neeraj GargBelum ada peringkat

- Indian Union Budget 2020Dokumen11 halamanIndian Union Budget 2020Md DhaniyalBelum ada peringkat

- Bangladesh Quarterly Economic Update: June 2014Dari EverandBangladesh Quarterly Economic Update: June 2014Belum ada peringkat

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismDari EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismBelum ada peringkat

- A Comprehensive Assessment of Tax Capacity in Southeast AsiaDari EverandA Comprehensive Assessment of Tax Capacity in Southeast AsiaBelum ada peringkat

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesDari EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesBelum ada peringkat

- 2 Obligations General Provisions 1156 1162Dokumen15 halaman2 Obligations General Provisions 1156 1162Emanuel CenidozaBelum ada peringkat

- Wa0004.Dokumen85 halamanWa0004.sheetalsri1407Belum ada peringkat

- Contoh Format Soal PTSDokumen3 halamanContoh Format Soal PTSSmp nasional plus widiatmikaBelum ada peringkat

- IFM Goodweek Tires, Inc.Dokumen2 halamanIFM Goodweek Tires, Inc.Desalegn Baramo GEBelum ada peringkat

- SSC CGL Tier 2 Quantitative Abilities 16-Nov-2020Dokumen17 halamanSSC CGL Tier 2 Quantitative Abilities 16-Nov-2020aBelum ada peringkat

- Ce QuizDokumen2 halamanCe QuizCidro Jake TyronBelum ada peringkat

- Activity 1: 2. Does His Homework - He S 3 Late ForDokumen10 halamanActivity 1: 2. Does His Homework - He S 3 Late ForINTELIGENCIA EDUCATIVABelum ada peringkat

- Marketing Case Study - MM1 (EPGPX02, GROUP-06)Dokumen5 halamanMarketing Case Study - MM1 (EPGPX02, GROUP-06)kaushal dhapareBelum ada peringkat

- The Sociopath's MantraDokumen2 halamanThe Sociopath's MantraStrategic ThinkerBelum ada peringkat

- Registration Form: Advancement in I.C.Engine and Vehicle System"Dokumen2 halamanRegistration Form: Advancement in I.C.Engine and Vehicle System"Weld TechBelum ada peringkat

- Revised Organizational Structure of Railway BoardDokumen4 halamanRevised Organizational Structure of Railway BoardThirunavukkarasu ThirunavukkarasuBelum ada peringkat

- Literature Circles Secondary SolutionsDokumen2 halamanLiterature Circles Secondary Solutionsapi-235368198Belum ada peringkat

- An Equivalent SDOF System Model For Estimating The Earthquake Response of R/C Buildings With Hysteretic DampersDokumen8 halamanAn Equivalent SDOF System Model For Estimating The Earthquake Response of R/C Buildings With Hysteretic DampersAlex MolinaBelum ada peringkat

- Choi, J H - Augustinian Interiority-The Teleological Deification of The Soul Through Divine Grace PDFDokumen253 halamanChoi, J H - Augustinian Interiority-The Teleological Deification of The Soul Through Divine Grace PDFed_colenBelum ada peringkat

- Munslow, A. What History IsDokumen2 halamanMunslow, A. What History IsGoshai DaianBelum ada peringkat

- Fish Feed Composition and ProductionDokumen54 halamanFish Feed Composition and ProductionhaniffBelum ada peringkat

- Rizal's First Return Home to the PhilippinesDokumen52 halamanRizal's First Return Home to the PhilippinesMaria Mikaela MarcelinoBelum ada peringkat

- Solutions Manual For Corporate Finance, 6e Jonathan BerkDokumen7 halamanSolutions Manual For Corporate Finance, 6e Jonathan Berksobiakhan52292Belum ada peringkat

- B§ÐmMm OÝ_ : EH$ {Z~§YmVrc H$ënZmDokumen70 halamanB§ÐmMm OÝ_ : EH$ {Z~§YmVrc H$ënZmVikas NikharangeBelum ada peringkat

- 268 General Knowledge Set ADokumen48 halaman268 General Knowledge Set Aguru prasadBelum ada peringkat

- Solving Problems Involving Simple Interest: Lesson 2Dokumen27 halamanSolving Problems Involving Simple Interest: Lesson 2Paolo MaquidatoBelum ada peringkat

- JNVD Souvenir FinalDokumen67 halamanJNVD Souvenir Finalkundanno1100% (1)

- Noise Pollution Control Policy IndiaDokumen10 halamanNoise Pollution Control Policy IndiaAllu GiriBelum ada peringkat

- ICE Professional Review GuidanceDokumen23 halamanICE Professional Review Guidancerahulgehlot2008Belum ada peringkat