Anda mungkin juga menyukai

- Studio Ghibli - Ghibli MedleyDokumen6 halamanStudio Ghibli - Ghibli MedleyNurul Ain Razali100% (14)

- Christmas - Classical - Bach and Rachmaninoff MedleyDokumen8 halamanChristmas - Classical - Bach and Rachmaninoff Medleymaustro100% (1)

- 1990 Newsday Article On Donald TrumpDokumen10 halaman1990 Newsday Article On Donald TrumpGlennKesslerWPBelum ada peringkat

- Market failures and government interventionDokumen13 halamanMarket failures and government interventionMavic CasasBelum ada peringkat

- Career FAQs - Accounting PDFDokumen150 halamanCareer FAQs - Accounting PDFmaustroBelum ada peringkat

- Career FAQs - Accounting PDFDokumen150 halamanCareer FAQs - Accounting PDFmaustroBelum ada peringkat

- Career FAQs - Legal PDFDokumen197 halamanCareer FAQs - Legal PDFmaustroBelum ada peringkat

- Market Potential and Customer Satisfaction of Adidas ShoesDokumen85 halamanMarket Potential and Customer Satisfaction of Adidas ShoesPurnendraBelum ada peringkat

- Chap 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsDokumen48 halamanChap 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsjeankerlensBelum ada peringkat

- Career FAQs - Work From Home PDFDokumen202 halamanCareer FAQs - Work From Home PDFmaustroBelum ada peringkat

- LC Draft Raw Cashew NutDokumen5 halamanLC Draft Raw Cashew NutUDAYBelum ada peringkat

- Market Structure Analysis: Types and CharacteristicsDokumen19 halamanMarket Structure Analysis: Types and Characteristicsgayasesha100% (1)

- The Sims - Build 5Dokumen12 halamanThe Sims - Build 5maustroBelum ada peringkat

- The Sims - Build 5Dokumen12 halamanThe Sims - Build 5maustroBelum ada peringkat

- Module 7Dokumen35 halamanModule 7Mishti Ritz MukherjeeBelum ada peringkat

- CSR, Sustainability, Ethics & - Governance - Bernhard Bachmann (Auth.) - Ethical Leadership in Organizations - Concepts and Implementation (2017, Springer International Publishing)Dokumen213 halamanCSR, Sustainability, Ethics & - Governance - Bernhard Bachmann (Auth.) - Ethical Leadership in Organizations - Concepts and Implementation (2017, Springer International Publishing)ZahirSyah100% (1)

- Positive Normative EconomicsDokumen4 halamanPositive Normative EconomicslulughoshBelum ada peringkat

- AssignmentDokumen5 halamanAssignmentdishan joelBelum ada peringkat

- Economics Exam Notes - MonopolyDokumen5 halamanEconomics Exam Notes - MonopolyDistingBelum ada peringkat

- Micro2 Lec 02 HandoutDokumen11 halamanMicro2 Lec 02 HandoutsofiaBelum ada peringkat

- Perfect and Imperfect MarketDokumen10 halamanPerfect and Imperfect MarketMalde KhuntiBelum ada peringkat

- Monopolistic Competition, Oligopoly, and Pure MonopolyDokumen5 halamanMonopolistic Competition, Oligopoly, and Pure MonopolyImran SiddBelum ada peringkat

- Session 1.2017Dokumen2 halamanSession 1.2017Amgad ElshamyBelum ada peringkat

- Ec131 Market StructuresDokumen24 halamanEc131 Market StructuresResult ThomasBelum ada peringkat

- Market Structure NotesDokumen8 halamanMarket Structure NotesABDUL HADIBelum ada peringkat

- Market StructureDokumen7 halamanMarket StructureAsadulla KhanBelum ada peringkat

- Competition, Profit and Other Objectives: What Does Normal Profit Mean?Dokumen7 halamanCompetition, Profit and Other Objectives: What Does Normal Profit Mean?Ming Pong NgBelum ada peringkat

- Perfect Competition Describes Markets Such That No Participants Are Large Enough To HauctDokumen17 halamanPerfect Competition Describes Markets Such That No Participants Are Large Enough To HauctRrisingg MishraaBelum ada peringkat

- Chapter 35 - Different Market StructuresDokumen52 halamanChapter 35 - Different Market StructuresPhuong DaoBelum ada peringkat

- A Written Report in Pure Monopoly: Submitted ToDokumen12 halamanA Written Report in Pure Monopoly: Submitted ToEd Leen ÜBelum ada peringkat

- Monopolistic CompetitionDokumen5 halamanMonopolistic CompetitionSyed BabrakBelum ada peringkat

- Market-Structures-in-Terms-of-Sellers-week-5Dokumen5 halamanMarket-Structures-in-Terms-of-Sellers-week-5Ex PertzBelum ada peringkat

- T5. CompetitionDokumen4 halamanT5. CompetitionNothing ThereBelum ada peringkat

- BE II - U1 Market Structure and PricingDokumen6 halamanBE II - U1 Market Structure and PricingVishal AgrawalBelum ada peringkat

- EconomicsDokumen2 halamanEconomicsIrish Mae T. EspallardoBelum ada peringkat

- Impacts of Monopoly On EfficiencyDokumen3 halamanImpacts of Monopoly On EfficiencyDyan LacanlaleBelum ada peringkat

- CIS Microeconomics Exam ThreeDokumen4 halamanCIS Microeconomics Exam ThreeVictoriaBelum ada peringkat

- Monopolistic Competition Is A Form ofDokumen8 halamanMonopolistic Competition Is A Form ofjcipriano_1Belum ada peringkat

- Assignment - Market StructureDokumen5 halamanAssignment - Market Structurerhizelle19Belum ada peringkat

- Topic: Price Positioning in A Competitive Market, A Case Study On Tile Company (Nitco)Dokumen10 halamanTopic: Price Positioning in A Competitive Market, A Case Study On Tile Company (Nitco)Shivangi mittalBelum ada peringkat

- Market StructuresDokumen12 halamanMarket Structuresrajneshchander100% (1)

- Economics AssignmentDokumen4 halamanEconomics AssignmentFarman RazaBelum ada peringkat

- Econ This IsDokumen11 halamanEcon This Isbeasteast80Belum ada peringkat

- A Market Is A Place Buyers and Sellers Meet To Make Exchanges, Such As Money For A Cell Phone. TDokumen3 halamanA Market Is A Place Buyers and Sellers Meet To Make Exchanges, Such As Money For A Cell Phone. TMonaoray BalowaBelum ada peringkat

- Resume of Principles of Economics Chapter on Firms in Competitive MarketsDokumen4 halamanResume of Principles of Economics Chapter on Firms in Competitive MarketsWanda AuliaBelum ada peringkat

- Chapter Two: Demand and SupplyDokumen71 halamanChapter Two: Demand and Supplykasech mogesBelum ada peringkat

- Monopoly Characteristics and Market ControlDokumen6 halamanMonopoly Characteristics and Market ControlSonia MenezesBelum ada peringkat

- Micro Notes Chapter 10Dokumen10 halamanMicro Notes Chapter 10D HoBelum ada peringkat

- Econ. Mod 5Dokumen19 halamanEcon. Mod 5Jenny Rose SanchezBelum ada peringkat

- Final Exam (Answer) : ECO1132 (Fall-2020)Dokumen13 halamanFinal Exam (Answer) : ECO1132 (Fall-2020)Nahid Mahmud ZayedBelum ada peringkat

- MARKET STRUCURE PPTDokumen43 halamanMARKET STRUCURE PPTGEORGEBelum ada peringkat

- Perfect Competition and Pricing DecisionsDokumen11 halamanPerfect Competition and Pricing DecisionsBirendra ShresthaBelum ada peringkat

- MonopolyDokumen7 halamanMonopolyGercel Therese SerafinoBelum ada peringkat

- Monopolistic CompetitionDokumen25 halamanMonopolistic Competitionmurthy2009Belum ada peringkat

- Weekly Summary ReportDokumen7 halamanWeekly Summary Reportmd.educationaidsBelum ada peringkat

- Perfect and Imperfect CompetitionDokumen7 halamanPerfect and Imperfect CompetitionShirish GutheBelum ada peringkat

- Chapter 7 Market Structures Teacher NotesDokumen10 halamanChapter 7 Market Structures Teacher Notesresendizalexander05Belum ada peringkat

- Economics Chapter 5Dokumen22 halamanEconomics Chapter 5Hirut AnjaBelum ada peringkat

- Q1) Assess The Differences and The Similarities in Characteristics, Pricing and Output Between Perfect Competition and Monopolistic Competition.Dokumen6 halamanQ1) Assess The Differences and The Similarities in Characteristics, Pricing and Output Between Perfect Competition and Monopolistic Competition.Sumble NaeemBelum ada peringkat

- Lecture Chapter6Dokumen7 halamanLecture Chapter6Angelica Joy ManaoisBelum ada peringkat

- MKT Structure !Dokumen25 halamanMKT Structure !jakowanBelum ada peringkat

- Economic Analysis: MonopolyDokumen27 halamanEconomic Analysis: Monopolykisser141Belum ada peringkat

- Contestable Markets (Final 2)Dokumen6 halamanContestable Markets (Final 2)Shrey DivvaakarBelum ada peringkat

- COMPETITION AND DIFFERENTIATED PRODUCTSDokumen19 halamanCOMPETITION AND DIFFERENTIATED PRODUCTSPowli HarshavardhanBelum ada peringkat

- IB MicroeconomicsDokumen55 halamanIB MicroeconomicszainBelum ada peringkat

- Market Structures: BarriersDokumen4 halamanMarket Structures: BarriersAdelwina AsuncionBelum ada peringkat

- Notes Business EcoDokumen8 halamanNotes Business EcoWissal RiyaniBelum ada peringkat

- Micro II Note Finalll 1Dokumen60 halamanMicro II Note Finalll 1minemy214Belum ada peringkat

- Market Structures ExplainedDokumen2 halamanMarket Structures ExplainedPriyanshu GuptaBelum ada peringkat

- Career FAQs - Save The World PDFDokumen193 halamanCareer FAQs - Save The World PDFmaustroBelum ada peringkat

- Career FAQs - Be Your Own Boss PDFDokumen233 halamanCareer FAQs - Be Your Own Boss PDFmaustroBelum ada peringkat

- Career FAQs InformationTechnologyDokumen178 halamanCareer FAQs InformationTechnologyxx1yyy1Belum ada peringkat

- Career FAQs Banking CareersDokumen181 halamanCareer FAQs Banking CareersTimothy NguyenBelum ada peringkat

- Career FAQs - Sample Cover Letter PDFDokumen2 halamanCareer FAQs - Sample Cover Letter PDFmaustroBelum ada peringkat

- Career FAQs - Property PDFDokumen169 halamanCareer FAQs - Property PDFmaustroBelum ada peringkat

- Career FAQs - Law (NSW and ACT) PDFDokumen148 halamanCareer FAQs - Law (NSW and ACT) PDFmaustroBelum ada peringkat

- Career FAQs - Sample CV PDFDokumen4 halamanCareer FAQs - Sample CV PDFmaustroBelum ada peringkat

- Career FAQs - Financial Planning PDFDokumen206 halamanCareer FAQs - Financial Planning PDFmaustroBelum ada peringkat

- Career FAQs - Investment Banking PDFDokumen170 halamanCareer FAQs - Investment Banking PDFmaustroBelum ada peringkat

- Career FAQs - Sample CV PDFDokumen4 halamanCareer FAQs - Sample CV PDFmaustroBelum ada peringkat

- Career FAQs - Save The World PDFDokumen193 halamanCareer FAQs - Save The World PDFmaustroBelum ada peringkat

- Career FAQs - Law (NSW and ACT) PDFDokumen148 halamanCareer FAQs - Law (NSW and ACT) PDFmaustroBelum ada peringkat

- Career FAQs - Entertainment PDFDokumen190 halamanCareer FAQs - Entertainment PDFmaustroBelum ada peringkat

- Career FAQs - Investment Banking PDFDokumen170 halamanCareer FAQs - Investment Banking PDFmaustroBelum ada peringkat

- Career FAQs Banking CareersDokumen181 halamanCareer FAQs Banking CareersTimothy NguyenBelum ada peringkat

- Career FAQs - Sample Cover Letter PDFDokumen2 halamanCareer FAQs - Sample Cover Letter PDFmaustroBelum ada peringkat

- Commentary On Cases of BreachDokumen46 halamanCommentary On Cases of BreachmaustroBelum ada peringkat

- The Sims - Build 3, 'Since We Met'Dokumen9 halamanThe Sims - Build 3, 'Since We Met'maustroBelum ada peringkat

- Career FAQs - Financial Planning PDFDokumen206 halamanCareer FAQs - Financial Planning PDFmaustroBelum ada peringkat

- Career FAQs - Entertainment PDFDokumen190 halamanCareer FAQs - Entertainment PDFmaustroBelum ada peringkat

- Laputa - Main Theme (A Minor)Dokumen10 halamanLaputa - Main Theme (A Minor)maustroBelum ada peringkat

- Oxford Said MBA Brochure 2017 18 PDFDokumen13 halamanOxford Said MBA Brochure 2017 18 PDFEducación ContinuaBelum ada peringkat

- Model Trading Standard ExplainedDokumen12 halamanModel Trading Standard ExplainedVinca Grace SihombingBelum ada peringkat

- Cornell NotesDokumen1 halamanCornell NotesEustass RellyyBelum ada peringkat

- EDCA Publishing & Distributing Corp. vs. Santos PDFDokumen8 halamanEDCA Publishing & Distributing Corp. vs. Santos PDFRaine VerdanBelum ada peringkat

- Planning & Strategic ManagementDokumen135 halamanPlanning & Strategic ManagementSurajit GoswamiBelum ada peringkat

- Factors - Influencing Implementation of A Dry Port PDFDokumen17 halamanFactors - Influencing Implementation of A Dry Port PDFIwan Puja RiyadiBelum ada peringkat

- Ihrm GPDokumen24 halamanIhrm GPMusa AmanBelum ada peringkat

- You Exec - Sales Process FreeDokumen13 halamanYou Exec - Sales Process FreeMariana Dominguez AlvesBelum ada peringkat

- Performance Review and GoalsDokumen3 halamanPerformance Review and GoalsTaha NabilBelum ada peringkat

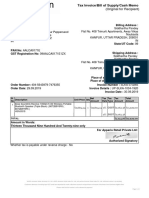

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokumen1 halamanTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Satyam SinghBelum ada peringkat

- COMPRO CB IndonesiaDokumen8 halamanCOMPRO CB IndonesiaWilly AriefBelum ada peringkat

- Overview of Persuasive Advertising-R8-N8.2.2014Dokumen52 halamanOverview of Persuasive Advertising-R8-N8.2.2014Tawfik EwedaBelum ada peringkat

- ENSP - Tender No.0056 - ENSP - DPE - AE - INV - 19 - Supply of A Truck Mounted Bundle ExtractorDokumen2 halamanENSP - Tender No.0056 - ENSP - DPE - AE - INV - 19 - Supply of A Truck Mounted Bundle ExtractorOussama AmaraBelum ada peringkat

- SEC - Graduate PositionDokumen6 halamanSEC - Graduate PositionGiorgos MeleasBelum ada peringkat

- 444 Advanced AccountingDokumen3 halaman444 Advanced AccountingTahir Naeem Jatt0% (1)

- Management Accounting Syllabus UGMDokumen3 halamanManagement Accounting Syllabus UGMdwiiiBelum ada peringkat

- Event Planning Rubric - Alternative Event Project Template Luc PatbergDokumen1 halamanEvent Planning Rubric - Alternative Event Project Template Luc Patbergapi-473891068Belum ada peringkat

- Scope and Methods of EconomicsDokumen4 halamanScope and Methods of EconomicsBalasingam PrahalathanBelum ada peringkat

- MTAP Saturday Math Grade 4Dokumen2 halamanMTAP Saturday Math Grade 4Luis SalengaBelum ada peringkat

- MCR2E Chapter 1 SlidesDokumen14 halamanMCR2E Chapter 1 SlidesRowan RodriguesBelum ada peringkat

- Vinati Organics Ltd financial analysis and key metrics from 2011 to 2020Dokumen30 halamanVinati Organics Ltd financial analysis and key metrics from 2011 to 2020nhariBelum ada peringkat

- CH 09Dokumen35 halamanCH 09ReneeBelum ada peringkat

- JollibeeDokumen5 halamanJollibeeDaphane Kate AureadaBelum ada peringkat

- Average Due Date and Account CurrentDokumen80 halamanAverage Due Date and Account CurrentShynaBelum ada peringkat

- Amrit Notes - PDF Version 1 PDFDokumen49 halamanAmrit Notes - PDF Version 1 PDFAmrit GaireBelum ada peringkat

- Account StatementDokumen3 halamanAccount StatementRonald MyersBelum ada peringkat