Anda mungkin juga menyukai

- Detailed Engineering Design PhaseDokumen8 halamanDetailed Engineering Design PhaseWilliam Palozzo100% (1)

- Process Safety DesignDokumen13 halamanProcess Safety DesignWilliam Palozzo100% (2)

- OjoylanJenny - Charmingly (Case#5)Dokumen5 halamanOjoylanJenny - Charmingly (Case#5)Jenny Ojoylan100% (1)

- Pipeline EconomicsDokumen66 halamanPipeline Economicsali100% (1)

- Icc CatalogueDokumen28 halamanIcc CatalogueWilliam PalozzoBelum ada peringkat

- Real Estate Economics QuestionsDokumen6 halamanReal Estate Economics QuestionsJuan Carlos Nocedal100% (3)

- Document Controlling ManagementDokumen18 halamanDocument Controlling ManagementWilliam PalozzoBelum ada peringkat

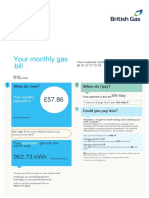

- Get PDF For Bill ViewDokumen4 halamanGet PDF For Bill ViewKrishna8765Belum ada peringkat

- Oil and Gas Contracts in Trinidad and Tobago Heidi WongDokumen32 halamanOil and Gas Contracts in Trinidad and Tobago Heidi WongAdian AndrewsBelum ada peringkat

- Monitoring Nigerian Oil and Gas ProductionDokumen104 halamanMonitoring Nigerian Oil and Gas Productiontsar_philip2010Belum ada peringkat

- 2012 PetroSkills Facilities Training GuideDokumen68 halaman2012 PetroSkills Facilities Training GuideWilliam PalozzoBelum ada peringkat

- SPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field EconomicsDokumen19 halamanSPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field Economicsipali4christ_5308248Belum ada peringkat

- Eni S.p.A. Exploration & Production Division Facilities Documents and Software SpecificationDokumen178 halamanEni S.p.A. Exploration & Production Division Facilities Documents and Software SpecificationWilliam Palozzo100% (1)

- OMC 2015 ProgrammeDokumen48 halamanOMC 2015 ProgrammeWilliam PalozzoBelum ada peringkat

- 3 International Commercial Sale of GoodsDokumen31 halaman3 International Commercial Sale of GoodsPranav GhabrooBelum ada peringkat

- SMC Guide BookDokumen15 halamanSMC Guide BookUsman Haider89% (9)

- Carbon Finance: The Financial Implications of Climate ChangeDari EverandCarbon Finance: The Financial Implications of Climate ChangePenilaian: 5 dari 5 bintang5/5 (1)

- Flaring DownDokumen4 halamanFlaring DownWilliam PalozzoBelum ada peringkat

- A Gas-1-5-2-4-2-1-2-1-1-1-3-1-1Dokumen1 halamanA Gas-1-5-2-4-2-1-2-1-1-1-3-1-1Daia SorinBelum ada peringkat

- Day1 - 06 - Ramona Volciuc-Ionescu - Volvic-Ionescu SCADokumen21 halamanDay1 - 06 - Ramona Volciuc-Ionescu - Volvic-Ionescu SCAaegean227Belum ada peringkat

- Norwegian Petroleum TaxationDokumen72 halamanNorwegian Petroleum TaxationHayden VanBelum ada peringkat

- 4 - June 2016 Paper 3.04 (Suggested Solutions)Dokumen11 halaman4 - June 2016 Paper 3.04 (Suggested Solutions)Faisal MehmoodBelum ada peringkat

- Royalty Review 0815 BMO (00000002)Dokumen25 halamanRoyalty Review 0815 BMO (00000002)TeamWildroseBelum ada peringkat

- Petroleum Revenue Funds - Part 1Dokumen4 halamanPetroleum Revenue Funds - Part 1Sameer YounusBelum ada peringkat

- Windfall Taxes Good Politics, Tricky Policy Financial TimesDokumen11 halamanWindfall Taxes Good Politics, Tricky Policy Financial TimesNinetyNineBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDokumen15 halamanPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamBelum ada peringkat

- Cambodia Oil Gas Newsletter 8Dokumen4 halamanCambodia Oil Gas Newsletter 8Murad MuradovBelum ada peringkat

- Will the Euro Survive the Debt CrisisDokumen18 halamanWill the Euro Survive the Debt CrisisSoumyadip MistryBelum ada peringkat

- Ch.9 Regional Economic IssuesDokumen39 halamanCh.9 Regional Economic IssuesDina SamirBelum ada peringkat

- Oil Contracts & Production Sharing Agreements ExplainedDokumen27 halamanOil Contracts & Production Sharing Agreements ExplainedfrelonfrelonBelum ada peringkat

- June 2019 Module 3.04Dokumen14 halamanJune 2019 Module 3.04Faisal MehmoodBelum ada peringkat

- Clase8 Endesa EurogenDokumen28 halamanClase8 Endesa EurogenJuan JesúsBelum ada peringkat

- Opec ProposalDokumen6 halamanOpec Proposalapi-633570160Belum ada peringkat

- Cambridge Working Papers in Economics CWPE 0508: Why Tax Energy? Towards A More Rational Energy PolicyDokumen37 halamanCambridge Working Papers in Economics CWPE 0508: Why Tax Energy? Towards A More Rational Energy PolicyMatteo LeonardiBelum ada peringkat

- Dissertation Oil PricesDokumen4 halamanDissertation Oil PricesDoMyCollegePaperForMeColumbia100% (1)

- Nigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas SectorDokumen6 halamanNigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas Sectorpradeep s gillBelum ada peringkat

- Petroleum Subsidies: A Case Against SubsidiesDokumen25 halamanPetroleum Subsidies: A Case Against Subsidiesanmol_bajajBelum ada peringkat

- Taxation and Investment Issues in Mining: Paul MitchellDokumen5 halamanTaxation and Investment Issues in Mining: Paul MitchellbenaskotBelum ada peringkat

- Crude OilDokumen13 halamanCrude OilRajesh Kumar RoutBelum ada peringkat

- Rising Fuel PricesDokumen2 halamanRising Fuel PricesstudentBelum ada peringkat

- Rising Fuel PricesDokumen2 halamanRising Fuel PricesununBelum ada peringkat

- LLM: Oil and Gas Law-State Control (LS5045) Student ID: 51123686Dokumen8 halamanLLM: Oil and Gas Law-State Control (LS5045) Student ID: 51123686lipikahimBelum ada peringkat

- Lecture Slides Chapter 08Dokumen24 halamanLecture Slides Chapter 08Nadeem JonaidBelum ada peringkat

- Impact of Finance & Accounting On The Energy IndustryDokumen2 halamanImpact of Finance & Accounting On The Energy IndustryJubril_A_DaviesBelum ada peringkat

- Cap & Trade: An Overview of the Key Concepts and ConsiderationsDokumen8 halamanCap & Trade: An Overview of the Key Concepts and Considerationschut123Belum ada peringkat

- OPEC Oil Outlook 2030Dokumen22 halamanOPEC Oil Outlook 2030Bruno Dias da CostaBelum ada peringkat

- Lecture 9Dokumen6 halamanLecture 9Rabie HarounBelum ada peringkat

- Macroeconomic Effects of Petroleum Price HikeDokumen7 halamanMacroeconomic Effects of Petroleum Price Hikemd yousufBelum ada peringkat

- File Comp Mining Tax RegimeDokumen12 halamanFile Comp Mining Tax Regimeatcher01Belum ada peringkat

- Why Deflation Is Good News For EuropeDokumen2 halamanWhy Deflation Is Good News For EuropeRun ZhongBelum ada peringkat

- Fuel Excise TaxDokumen6 halamanFuel Excise TaxRobin BaricauaBelum ada peringkat

- Optimize Tax Regime for Extractive IndustriesDokumen49 halamanOptimize Tax Regime for Extractive IndustriesSaeda NajafizadaBelum ada peringkat

- Phasing Out Fuel Subsidies in NigeriaDokumen3 halamanPhasing Out Fuel Subsidies in NigeriaEfosaUwaifoBelum ada peringkat

- Fiscal Regimes - Some AspectsDokumen9 halamanFiscal Regimes - Some AspectsGeorge GeorgiadisBelum ada peringkat

- Oil Production Economics and Politics in Latin AmericaDokumen46 halamanOil Production Economics and Politics in Latin AmericaHéctor FloresBelum ada peringkat

- SPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal BillDokumen14 halamanSPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal Billipali4christ_5308248Belum ada peringkat

- TheoilsectorDokumen24 halamanTheoilsectorjamilkhannBelum ada peringkat

- The Dynamics of Windfall Taxation System20092Dokumen9 halamanThe Dynamics of Windfall Taxation System20092Mouni SheoranBelum ada peringkat

- Flexible hybrid power plants for the energy transitionDokumen10 halamanFlexible hybrid power plants for the energy transitionWilliam PalozzoBelum ada peringkat

- Conference Report LRDokumen20 halamanConference Report LRWilliam PalozzoBelum ada peringkat

- Opi Svi 001 Annex E Handover Process Framework PDFDokumen3 halamanOpi Svi 001 Annex E Handover Process Framework PDFWilliam PalozzoBelum ada peringkat

- Api 322-1994Dokumen70 halamanApi 322-1994William PalozzoBelum ada peringkat

- Tennesee OilDokumen106 halamanTennesee OilWilliam PalozzoBelum ada peringkat

- Africa's Place in The Global HydrocarbonsDokumen30 halamanAfrica's Place in The Global HydrocarbonsWilliam PalozzoBelum ada peringkat

- 2012 First Quarter ResultsDokumen21 halaman2012 First Quarter ResultsWilliam PalozzoBelum ada peringkat

- Case Study IGFDokumen33 halamanCase Study IGFAmirol Ahmad TarmiziBelum ada peringkat

- Brian Nixon, Decommissioning North SeaDokumen7 halamanBrian Nixon, Decommissioning North SeaWilliam PalozzoBelum ada peringkat

- 4.1 - ANX-1 Definition of Mechanical CompletionDokumen18 halaman4.1 - ANX-1 Definition of Mechanical CompletionWilliam PalozzoBelum ada peringkat

- GAT2004 GKP 2010.004 Keys To A Successful Initial StartupDokumen2 halamanGAT2004 GKP 2010.004 Keys To A Successful Initial StartupWilliam PalozzoBelum ada peringkat

- Fenixus (Compatibiliteitsmodus)Dokumen17 halamanFenixus (Compatibiliteitsmodus)William PalozzoBelum ada peringkat

- IAS 16 SummaryDokumen5 halamanIAS 16 SummarythenikkitrBelum ada peringkat

- Jawapan ACC116 Week 6-Nahzatul ShimaDokumen2 halamanJawapan ACC116 Week 6-Nahzatul Shimaanon_207469897Belum ada peringkat

- Philippe Burger University of The Free State OECD Meeting Rabat - May 2008Dokumen45 halamanPhilippe Burger University of The Free State OECD Meeting Rabat - May 2008Soenarto SoendjajaBelum ada peringkat

- CH 4Dokumen23 halamanCH 4Gizaw BelayBelum ada peringkat

- Workshop Debt Securities STAFFDokumen42 halamanWorkshop Debt Securities STAFFIshan MalakarBelum ada peringkat

- Tugas Pertemuan 2 - Alya Sufi Ikrima - 041911333248Dokumen3 halamanTugas Pertemuan 2 - Alya Sufi Ikrima - 041911333248Alya Sufi IkrimaBelum ada peringkat

- Burmah CastrolDokumen13 halamanBurmah CastrolanfkrBelum ada peringkat

- Biotech Sunglasses Break-Even AnalysisDokumen8 halamanBiotech Sunglasses Break-Even AnalysisKuralay TilegenBelum ada peringkat

- Audit 3 Midterm Exam (CH 17,18,19,20 Cabrera)Dokumen3 halamanAudit 3 Midterm Exam (CH 17,18,19,20 Cabrera)Roldan Hiano ManganipBelum ada peringkat

- Costing Solutions GuideDokumen2 halamanCosting Solutions Guideপ্রদীপ হালদারBelum ada peringkat

- Bond ValuationDokumen3 halamanBond ValuationGauravBelum ada peringkat

- Chapter2 Exercise and TestDokumen22 halamanChapter2 Exercise and TestMichelle LamBelum ada peringkat

- How 24-Year-Old Stock Trader Made $8 Million in 2 YearsDokumen11 halamanHow 24-Year-Old Stock Trader Made $8 Million in 2 YearstimBelum ada peringkat

- DemandDokumen13 halamanDemandSweet EmmeBelum ada peringkat

- 9 Micro Ch17 Presentation7e Chap09Dokumen41 halaman9 Micro Ch17 Presentation7e Chap09Nguyễn Lê KhánhBelum ada peringkat

- Questions (Fun With Economics)Dokumen7 halamanQuestions (Fun With Economics)Bhoomi SinghBelum ada peringkat

- Chapter11 PDFDokumen22 halamanChapter11 PDFSairevanth ChakkaBelum ada peringkat

- SMChap 015Dokumen40 halamanSMChap 015zoomblue200100% (2)

- Chapter 9 SolutionsDokumen4 halamanChapter 9 SolutionsVaibhav MehtaBelum ada peringkat

- Chapter 4 Investment EfficiencyDokumen70 halamanChapter 4 Investment Efficiency10-12A1- Nguyễn Chí HiếuBelum ada peringkat

- 3.1 Income Elasticity of DemandDokumen35 halaman3.1 Income Elasticity of DemandBighnesh MahapatraBelum ada peringkat

- Ch17 - Money Growth and InflationDokumen49 halamanCh17 - Money Growth and InflationĐào Việt PhúcBelum ada peringkat

- Unit 3 Accounting For MaterialsDokumen21 halamanUnit 3 Accounting For MaterialsAayushi KothariBelum ada peringkat

- Government Issues Clarifications in Form of Faqs On One Time Compliance Window Scheme of The Black Money Taxation ActDokumen23 halamanGovernment Issues Clarifications in Form of Faqs On One Time Compliance Window Scheme of The Black Money Taxation ActSankaram KasturiBelum ada peringkat

- SkodaDokumen29 halamanSkodaPratik Bhuptani75% (4)