Anda mungkin juga menyukai

- BusTax Part 2Dokumen5 halamanBusTax Part 2Celine Therese BuBelum ada peringkat

- Donors Tax TheoriesDokumen6 halamanDonors Tax TheoriesAstrid VargasBelum ada peringkat

- TAX2Dokumen10 halamanTAX2Barbie EboniaBelum ada peringkat

- Statement: A Legally Adopted Child Who Is Not A Relative by Consanguinity of The 2 Statement: The Relatives by Consanguinity of The Wife Are Strangers As Far As DonorDokumen10 halamanStatement: A Legally Adopted Child Who Is Not A Relative by Consanguinity of The 2 Statement: The Relatives by Consanguinity of The Wife Are Strangers As Far As DonorGlo GanzonBelum ada peringkat

- Transfer Tax Quiz QuestionsDokumen5 halamanTransfer Tax Quiz QuestionsKyasiah Mae AragonesBelum ada peringkat

- MC - Exercises On Donor's Tax (PRTC)Dokumen12 halamanMC - Exercises On Donor's Tax (PRTC)Anna Charlotte33% (3)

- Donors Tax ReviewerDokumen9 halamanDonors Tax ReviewerMark Noel SanteBelum ada peringkat

- Bus Law and TaxDokumen15 halamanBus Law and Taxkay_kleirBelum ada peringkat

- Tax2 Midterm Exam-SentDokumen12 halamanTax2 Midterm Exam-SentRen A EleponioBelum ada peringkat

- Chapter 6 Donor S Tax PDFDokumen9 halamanChapter 6 Donor S Tax PDFLuna CakesBelum ada peringkat

- Tax2 Midterm ExamDokumen13 halamanTax2 Midterm ExamRen A Eleponio100% (2)

- Preboard CompreDokumen191 halamanPreboard CompreInny Agin100% (1)

- TAXATIONDokumen9 halamanTAXATIONkekadiegoBelum ada peringkat

- Q6 Donors TaxDokumen7 halamanQ6 Donors TaxGreta DuqueBelum ada peringkat

- TAX Final-PB FEUDokumen9 halamanTAX Final-PB FEUkarim abitagoBelum ada peringkat

- Estate TaxDokumen21 halamanEstate Taxjustin_bb100% (7)

- DONOR's Tax Multiple Choice QuestionDokumen13 halamanDONOR's Tax Multiple Choice QuestionRen A Eleponio83% (12)

- Taxation Donors Tax Quizzer 2020Dokumen7 halamanTaxation Donors Tax Quizzer 2020melyBelum ada peringkat

- Chapter 06 Donor's TaxDokumen16 halamanChapter 06 Donor's TaxNikki Bucatcat0% (2)

- Taxation - Donors-Tax - Quizzer - 2018Dokumen6 halamanTaxation - Donors-Tax - Quizzer - 2018Kenneth Bryan Tegerero Tegio67% (6)

- Chapter 16 TaxDokumen13 halamanChapter 16 TaxEmmanuel PenullarBelum ada peringkat

- Intro To Income TaxDokumen4 halamanIntro To Income TaxJennifer Arcadio100% (1)

- Part 5 Donor S TaxDokumen35 halamanPart 5 Donor S TaxKenBelum ada peringkat

- Tax2 Bar Qs CompiledDokumen10 halamanTax2 Bar Qs CompiledDaisyKeith VinesBelum ada peringkat

- Prelim Tax 2Dokumen13 halamanPrelim Tax 2Joseph Mangahas50% (2)

- Donors Tax Reviewer BLTDokumen10 halamanDonors Tax Reviewer BLTtrishaBelum ada peringkat

- Answer AnswerDokumen9 halamanAnswer Answerbatoonrussel61Belum ada peringkat

- 2013 New Pre-Mid Dept ExamDokumen6 halaman2013 New Pre-Mid Dept ExamJulie Ann PiliBelum ada peringkat

- Donors Tax Quali ReviewerDokumen7 halamanDonors Tax Quali ReviewerRodelLaborBelum ada peringkat

- Chapter 05 Estate TaxDokumen14 halamanChapter 05 Estate TaxNikki BucatcatBelum ada peringkat

- Transfer Taxes Theory QuizzerDokumen15 halamanTransfer Taxes Theory QuizzerKenBelum ada peringkat

- Quiz Bee QestionnairesDokumen34 halamanQuiz Bee Qestionnairesanor.aquino.upBelum ada peringkat

- Quiz Questions and AnswersDokumen61 halamanQuiz Questions and AnswersMarvin AndresBelum ada peringkat

- Put A Mark On The Letter of Your ChoiceDokumen5 halamanPut A Mark On The Letter of Your Choicejhell dela cruzBelum ada peringkat

- Quizzer-Donor's TaxDokumen4 halamanQuizzer-Donor's TaxVergel Martinez33% (3)

- Taxation Quizzer PDFDokumen61 halamanTaxation Quizzer PDFPrince Guese86% (7)

- T R S A: HE Eview Chool of CcountancyDokumen143 halamanT R S A: HE Eview Chool of CcountancyJane MorilloBelum ada peringkat

- T R S A: HE Eview Chool of CcountancyDokumen14 halamanT R S A: HE Eview Chool of CcountancyRenz Joshua Quizon MunozBelum ada peringkat

- ReSA B42 TAX First PB Exam - Questions, Answers - SolutionsDokumen18 halamanReSA B42 TAX First PB Exam - Questions, Answers - SolutionsPearl Mae De VeasBelum ada peringkat

- 1Dokumen6 halaman1Marinel FelipeBelum ada peringkat

- Multiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationDokumen34 halamanMultiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationJay GalleroBelum ada peringkat

- DONOR S Tax Multiple Choice Question 1Dokumen13 halamanDONOR S Tax Multiple Choice Question 1Kj Banal80% (5)

- A. Condonation or Remission of A DebtDokumen3 halamanA. Condonation or Remission of A DebtTk KimBelum ada peringkat

- Mcq-Estate TaxDokumen2 halamanMcq-Estate TaxRandy ManzanoBelum ada peringkat

- Tax 86-12Dokumen5 halamanTax 86-12Marinel FelipeBelum ada peringkat

- Tax 86-12Dokumen5 halamanTax 86-12Marinel FelipeBelum ada peringkat

- Taxation of Individuals QuizzerDokumen38 halamanTaxation of Individuals QuizzerCookie Pookie BallerShopBelum ada peringkat

- Online Seatwork - Donors TaxDokumen12 halamanOnline Seatwork - Donors TaxVirginia PalisukBelum ada peringkat

- Taxation of Individuals QuizzerDokumen37 halamanTaxation of Individuals QuizzerCharry Ramos62% (13)

- Tax On Ind-QuizDokumen34 halamanTax On Ind-QuizKathleen Jane Solmayor100% (2)

- Multiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationDokumen34 halamanMultiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationAngel May L. LopezBelum ada peringkat

- Transfer Taxes Tax 2Dokumen45 halamanTransfer Taxes Tax 2Nat PantsBelum ada peringkat

- Income Taxation of IndividualsDokumen26 halamanIncome Taxation of Individualsarkisha100% (1)

- 1617 1stS FX CLim 1 1Dokumen10 halaman1617 1stS FX CLim 1 1ShitzeoBelum ada peringkat

- Vanishing Deductions From The Grss EstateDokumen7 halamanVanishing Deductions From The Grss EstateSenianna HaleBelum ada peringkat

- Value Added TaxDokumen8 halamanValue Added TaxErica VillaruelBelum ada peringkat

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Dari EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Belum ada peringkat

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Dari EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Penilaian: 5 dari 5 bintang5/5 (1)

- Tax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesDari EverandTax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesBelum ada peringkat

- Dutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshDokumen2 halamanDutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshNur NobiBelum ada peringkat

- Gov - Uk: Register For and File Your Self Assessment Tax ReturnDokumen4 halamanGov - Uk: Register For and File Your Self Assessment Tax ReturnJane Yonzon-RepolBelum ada peringkat

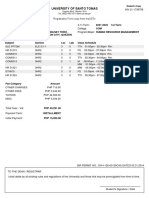

- University of Santo TomasDokumen1 halamanUniversity of Santo TomasDennis Michael DyBelum ada peringkat

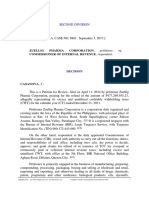

- Zuellig Vs CIRDokumen36 halamanZuellig Vs CIRMagenic Manila IncBelum ada peringkat

- Duplicate Copy: Balance Due 20466.50Dokumen2 halamanDuplicate Copy: Balance Due 20466.50ᏕᏬᏰᎧᎴᏂ ᏦᏬᎷᏗᏒ0% (1)

- Donors Tax DWCLDokumen6 halamanDonors Tax DWCLKyle Jezrel GimaoBelum ada peringkat

- Unit StatementDokumen3 halamanUnit StatementMrshiva2Belum ada peringkat

- Invoice FormatDokumen1 halamanInvoice Formatshreyash nakhawaBelum ada peringkat

- 1Dokumen13 halaman1Anonymous Se3uRZBelum ada peringkat

- By S.P.MishraDokumen43 halamanBy S.P.MishrasamBelum ada peringkat

- Banking XII PDFDokumen157 halamanBanking XII PDFmzahidbBelum ada peringkat

- Service TaxDokumen15 halamanService TaxMonu TulsyanBelum ada peringkat

- Basic Concept of Income TaxDokumen4 halamanBasic Concept of Income TaxNaurah Atika DinaBelum ada peringkat

- Funciones y Operaciones Del Cálculo de La NóminaDokumen51 halamanFunciones y Operaciones Del Cálculo de La NóminaRoberto MartínezBelum ada peringkat

- 1778 Inv & WaybillDokumen4 halaman1778 Inv & WaybillDALMIARJY DEPOBelum ada peringkat

- BSNL Wishes All Its Esteemed Customers A Very Happy and Safe DiwaliDokumen3 halamanBSNL Wishes All Its Esteemed Customers A Very Happy and Safe DiwaliFiroz ShaikhBelum ada peringkat

- Memorandum: Nihon Sekkei, Inc. - 1Dokumen7 halamanMemorandum: Nihon Sekkei, Inc. - 1Son PhanBelum ada peringkat

- Tx-Uk Mock 1Dokumen20 halamanTx-Uk Mock 1Lalan JaiswalBelum ada peringkat

- IPR ProjectDokumen32 halamanIPR ProjectHemantPrajapatiBelum ada peringkat

- FLT No - A-12, Starline Chs LTD, Sector No-1, Gorai, Rsc-4, Plot No-20 Best Officer QTR Bus ST, Borivali (W), Mumbai, 400092Dokumen2 halamanFLT No - A-12, Starline Chs LTD, Sector No-1, Gorai, Rsc-4, Plot No-20 Best Officer QTR Bus ST, Borivali (W), Mumbai, 400092akshali raneBelum ada peringkat

- Statement of Earnings and Deductions: Payment Date: Pay End DateDokumen1 halamanStatement of Earnings and Deductions: Payment Date: Pay End Dateanjali daveBelum ada peringkat

- Brad-O RDokumen1 halamanBrad-O Rgab100% (1)

- Belman Compania Vs Central Bank of The Phil 2Dokumen1 halamanBelman Compania Vs Central Bank of The Phil 2eunice demaclidBelum ada peringkat

- Module 1 Lesson 2 Estate Tax DeductionsDokumen15 halamanModule 1 Lesson 2 Estate Tax DeductionsHya Althea DiamanteBelum ada peringkat

- @ProCA - Inter DT Clubbing and Set Off Question Bank Nov2022Dokumen83 halaman@ProCA - Inter DT Clubbing and Set Off Question Bank Nov2022hero36407Belum ada peringkat

- Registration Upload22.07.2020Dokumen3 halamanRegistration Upload22.07.2020Afaque AlamBelum ada peringkat

- InvoiceDokumen1 halamanInvoiceRythmn MagnaniBelum ada peringkat

- Proforma Invoice-HDLDokumen1 halamanProforma Invoice-HDLRahul GuptaBelum ada peringkat

- What Is INMOTION - AIRPORT ORD CHICAGO IL - Scam ChargeDokumen4 halamanWhat Is INMOTION - AIRPORT ORD CHICAGO IL - Scam ChargeVictor NercioBelum ada peringkat