Anda mungkin juga menyukai

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018Dari EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018Belum ada peringkat

- 12 19 Reid Letter ManagersDokumen38 halaman12 19 Reid Letter Managersclyde2400Belum ada peringkat

- Downsizing Federal Government Spending: A Cato Institute GuideDari EverandDownsizing Federal Government Spending: A Cato Institute GuideBelum ada peringkat

- 10 7 Baucus LetterDokumen27 halaman10 7 Baucus LetterBrian AhierBelum ada peringkat

- Implementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesDari EverandImplementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesBelum ada peringkat

- Congressional Budget Office U.S. Congress Washington, DC 20515Dokumen17 halamanCongressional Budget Office U.S. Congress Washington, DC 20515api-26139761Belum ada peringkat

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDari Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsBelum ada peringkat

- 2010 Budget Perspective: The Real Deficit Effect of The Health BillDokumen5 halaman2010 Budget Perspective: The Real Deficit Effect of The Health BillWashington ExaminerBelum ada peringkat

- Hidden Spending: The Politics of Federal Credit ProgramsDari EverandHidden Spending: The Politics of Federal Credit ProgramsBelum ada peringkat

- Congressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Dokumen25 halamanCongressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Zim VicomBelum ada peringkat

- The Economists' Voice 2.0: The Financial Crisis, Health Care Reform, and MoreDari EverandThe Economists' Voice 2.0: The Financial Crisis, Health Care Reform, and MoreBelum ada peringkat

- Macro Effects of IRADokumen21 halamanMacro Effects of IRAmuhammad.nm.abidBelum ada peringkat

- Budget Update August 2005Dokumen6 halamanBudget Update August 2005Committee For a Responsible Federal BudgetBelum ada peringkat

- Wiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsDari EverandWiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsBelum ada peringkat

- Budgetcomparisons 4 5 00Dokumen5 halamanBudgetcomparisons 4 5 00Committee For a Responsible Federal BudgetBelum ada peringkat

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryDari EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Senate Amendment 2137 To H.R. 3684, The Infrastructure Investment and Jobs Act, As Proposed On August 1, 2021Dokumen19 halamanSenate Amendment 2137 To H.R. 3684, The Infrastructure Investment and Jobs Act, As Proposed On August 1, 2021Cynthia MoranBelum ada peringkat

- Budget Update March 142006Dokumen10 halamanBudget Update March 142006Committee For a Responsible Federal BudgetBelum ada peringkat

- Activities Related to Credit Intermediation Miscellaneous Revenues World Summary: Market Values & Financials by CountryDari EverandActivities Related to Credit Intermediation Miscellaneous Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- C R F B: Ommittee For A Esponsible Ederal UdgetDokumen6 halamanC R F B: Ommittee For A Esponsible Ederal UdgetCommittee For a Responsible Federal BudgetBelum ada peringkat

- 1040 Exam Prep: Module I: The Form 1040 FormulaDari Everand1040 Exam Prep: Module I: The Form 1040 FormulaPenilaian: 1 dari 5 bintang1/5 (3)

- Department of Health & Human ServicesDokumen31 halamanDepartment of Health & Human ServicesBrian AhierBelum ada peringkat

- HouseandSenateBudgetsApril2008 000Dokumen8 halamanHouseandSenateBudgetsApril2008 000Committee For a Responsible Federal BudgetBelum ada peringkat

- OACT Memorandum On Financial Impact of H R 3962 11-13-09 NoPWDokumen31 halamanOACT Memorandum On Financial Impact of H R 3962 11-13-09 NoPWthecynicaleconomistBelum ada peringkat

- CBO Debt Deal EstimateDokumen17 halamanCBO Debt Deal EstimateAustin DeneanBelum ada peringkat

- Inflation Reduction Act: Preliminary Estimates of Budgetary and Macroeconomic EffectsDokumen5 halamanInflation Reduction Act: Preliminary Estimates of Budgetary and Macroeconomic EffectsJohn SmithBelum ada peringkat

- Congressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Dokumen16 halamanCongressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515editorial.onlineBelum ada peringkat

- Economic Impacts of Waiting To Resolve The Long Term Budget ImbalanceDokumen12 halamanEconomic Impacts of Waiting To Resolve The Long Term Budget ImbalanceMilton RechtBelum ada peringkat

- CBO Score and Assessment To Repeal ObamacareDokumen10 halamanCBO Score and Assessment To Repeal ObamacareDarla DawaldBelum ada peringkat

- Legislative Fiscal Office Analysis of HB 1 Reengrossed (Updated 5/25/15)Dokumen135 halamanLegislative Fiscal Office Analysis of HB 1 Reengrossed (Updated 5/25/15)RepNLandryBelum ada peringkat

- Dream Act CostsDokumen6 halamanDream Act Costsjulie_rose3104Belum ada peringkat

- Impact of Unemployment Compensation Fund InsolvencyDokumen11 halamanImpact of Unemployment Compensation Fund InsolvencyAndy ChowBelum ada peringkat

- Hr4348conference Cbo ReportDokumen8 halamanHr4348conference Cbo ReportPeggy W SatterfieldBelum ada peringkat

- Getpdf 1Dokumen61 halamanGetpdf 1WilliamBelum ada peringkat

- Impact of StimulusDokumen20 halamanImpact of StimulusrebeltradersBelum ada peringkat

- FOMB - Letter - Senate of Puerto Rico - Response Letter Section 204 (A) (6) SB 1304 - February 7, 2024Dokumen3 halamanFOMB - Letter - Senate of Puerto Rico - Response Letter Section 204 (A) (6) SB 1304 - February 7, 2024Metro Puerto RicoBelum ada peringkat

- Estimated Impact of The American Recovery and Reinvestment Act On Employment and Economic Output From July 2010 Through September 2010Dokumen20 halamanEstimated Impact of The American Recovery and Reinvestment Act On Employment and Economic Output From July 2010 Through September 2010bball23fanBelum ada peringkat

- Budget Update May 2005Dokumen7 halamanBudget Update May 2005Committee For a Responsible Federal BudgetBelum ada peringkat

- CBO Letter March 5Dokumen18 halamanCBO Letter March 5ZerohedgeBelum ada peringkat

- The Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedDokumen19 halamanThe Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedcaseywootenBelum ada peringkat

- Us Cbo Budget DeficitsDokumen18 halamanUs Cbo Budget Deficitswmartin46Belum ada peringkat

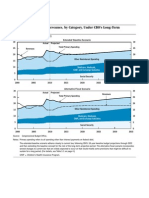

- Primary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosDokumen25 halamanPrimary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosPeggy W SatterfieldBelum ada peringkat

- Deficit Committee PaperDokumen5 halamanDeficit Committee PaperRyan DeCaroBelum ada peringkat

- Estimated Impact of The American Recovery and Reinvestment Act On Employment and Economic Output From October 2010 Through December 2010Dokumen20 halamanEstimated Impact of The American Recovery and Reinvestment Act On Employment and Economic Output From October 2010 Through December 2010Jeffrey DunetzBelum ada peringkat

- CBO2 Feb 2008Dokumen4 halamanCBO2 Feb 2008Committee For a Responsible Federal BudgetBelum ada peringkat

- Senator Murray Budget Memo 1-24Dokumen12 halamanSenator Murray Budget Memo 1-24Ezra Klein100% (1)

- FY 13 OMB JC Sequestration ReportDokumen83 halamanFY 13 OMB JC Sequestration ReportCeleste KatzBelum ada peringkat

- Exam19 20 SolutionsDokumen3 halamanExam19 20 SolutionsHenri De sloovereBelum ada peringkat

- CBO - Congressional Budget Office - Analysis On Harry Reid Debt Ceiling Proposed Plan - July 27th 2011Dokumen11 halamanCBO - Congressional Budget Office - Analysis On Harry Reid Debt Ceiling Proposed Plan - July 27th 2011Zim VicomBelum ada peringkat

- C L C S: Olorado Egislative Ouncil TaffDokumen12 halamanC L C S: Olorado Egislative Ouncil TaffCircuit MediaBelum ada peringkat

- RSC FY2011 Budget ProposalDokumen34 halamanRSC FY2011 Budget ProposalRandall SmithBelum ada peringkat

- CEA - The Economic Impact of ARRA - 20100414Dokumen45 halamanCEA - The Economic Impact of ARRA - 20100414Indivar Dutta-GuptaBelum ada peringkat

- Addressing The Long-Run Budget Deficit - A Comparison of Approaches - August 25, 2011 - (CRS)Dokumen38 halamanAddressing The Long-Run Budget Deficit - A Comparison of Approaches - August 25, 2011 - (CRS)QuantDev-MBelum ada peringkat

- Fy 2013 July UpdateDokumen281 halamanFy 2013 July UpdateNick ReismanBelum ada peringkat

- CBO Long-Term Analysis of Ryan's Budget ProposalDokumen30 halamanCBO Long-Term Analysis of Ryan's Budget ProposalMilton RechtBelum ada peringkat

- Presbudget 2 6 97Dokumen4 halamanPresbudget 2 6 97Committee For a Responsible Federal BudgetBelum ada peringkat

- CBOmemo Jan 04Dokumen2 halamanCBOmemo Jan 04Committee For a Responsible Federal BudgetBelum ada peringkat

- Disclose ActDokumen94 halamanDisclose Actclyde2400Belum ada peringkat

- 2001 Anthrax Investigation ReportDokumen96 halaman2001 Anthrax Investigation Reportclyde2400Belum ada peringkat

- Senate Health Reform Bill: Manager's AmendmentDokumen383 halamanSenate Health Reform Bill: Manager's AmendmentMarkWarnerBelum ada peringkat

- 2009q3 SinglevolumeDokumen3.404 halaman2009q3 Singlevolumeclyde2400Belum ada peringkat

- 11 23 GHG Emissions BriefDokumen12 halaman11 23 GHG Emissions Briefclyde2400Belum ada peringkat

- Affordable Health Care For America ActDokumen1.990 halamanAffordable Health Care For America ActThe West Virginia Examiner/WV Watchdog100% (1)

- Format of EFC/SFC Memorandum (For Revised Cost Estimate (RCE) Proposal)Dokumen7 halamanFormat of EFC/SFC Memorandum (For Revised Cost Estimate (RCE) Proposal)Melissa MillerBelum ada peringkat

- The Africa Act Plan: An IEG EvaluationDokumen181 halamanThe Africa Act Plan: An IEG EvaluationIndependent Evaluation GroupBelum ada peringkat

- Chapter 26 - Saving Investment and The Fincancial SystemDokumen10 halamanChapter 26 - Saving Investment and The Fincancial SystemScott PlunkettBelum ada peringkat

- HUD Salary DataDokumen5 halamanHUD Salary DataDennis YuskoBelum ada peringkat

- 6 BudgetingDokumen2 halaman6 BudgetingClyette Anne Flores BorjaBelum ada peringkat

- Bauxite Transfert PricingDokumen21 halamanBauxite Transfert PricingEyock PierreBelum ada peringkat

- Rau IASDokumen178 halamanRau IASNeeraj RåwâtBelum ada peringkat

- Budgeting Process and Pitching Ppt-Module-1,2Dokumen52 halamanBudgeting Process and Pitching Ppt-Module-1,2Abhishek RainaBelum ada peringkat

- AccountingDokumen57 halamanAccountingReynaldo Jose Alvarado RamosBelum ada peringkat

- Variable CostingDokumen7 halamanVariable CostingAiya Lumban0% (1)

- Fifth National Development Plan 2006 - 10Dokumen397 halamanFifth National Development Plan 2006 - 10Chola MukangaBelum ada peringkat

- ScavengeDokumen162 halamanScavengeIvan GeiryBelum ada peringkat

- Currency Trader Magazine 2011-06Dokumen31 halamanCurrency Trader Magazine 2011-06Lascu RomanBelum ada peringkat

- Sridhar P - Notes On PMP (Formulas)Dokumen5 halamanSridhar P - Notes On PMP (Formulas)KARTHIK145Belum ada peringkat

- Spoilage, Rework and ScrapDokumen27 halamanSpoilage, Rework and ScrapJason Gubatan100% (3)

- Cost Estimating Checklist PDFDokumen17 halamanCost Estimating Checklist PDFwalidBelum ada peringkat

- Hemant Pandey WMP13017 Inexperience Case IssueDokumen3 halamanHemant Pandey WMP13017 Inexperience Case IssueHemant PandeyBelum ada peringkat

- Cash MGTDokumen18 halamanCash MGTHai HaBelum ada peringkat

- Clingly Company (Eric Madia)Dokumen4 halamanClingly Company (Eric Madia)Eric MadiaBelum ada peringkat

- Balance Budget Sim Lesson PlanDokumen5 halamanBalance Budget Sim Lesson Planapi-245012288Belum ada peringkat

- Part 3B Planning and Budgeting 322 QuestionsDokumen96 halamanPart 3B Planning and Budgeting 322 QuestionsMariaBelum ada peringkat

- CVPDokumen20 halamanCVPDen Potxsz100% (1)

- CBS News Poll: Fiscal CliffDokumen14 halamanCBS News Poll: Fiscal CliffCBS_News0% (1)

- QS VariationsDokumen7 halamanQS VariationsSathiya SeelanBelum ada peringkat

- 2016 Budget Guidelines PDFDokumen136 halaman2016 Budget Guidelines PDFNYAMEKYE ADOMAKOBelum ada peringkat

- CyfDokumen13 halamanCyfdeepakBelum ada peringkat

- Barangay Budget GuidelineDokumen10 halamanBarangay Budget GuidelineMicky MoranteBelum ada peringkat

- SAP Funds Management INFODokumen4 halamanSAP Funds Management INFOAkashBelum ada peringkat

- Human Development Report Andhra Pradesh 2007 Full ReportDokumen280 halamanHuman Development Report Andhra Pradesh 2007 Full ReportkalyanlspBelum ada peringkat

- Project Management PlanDokumen38 halamanProject Management PlanEnghlab Eftekhari100% (2)

- Modern Warriors: Real Stories from Real HeroesDari EverandModern Warriors: Real Stories from Real HeroesPenilaian: 3.5 dari 5 bintang3.5/5 (3)

- Power Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicDari EverandPower Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicBelum ada peringkat

- The Next Civil War: Dispatches from the American FutureDari EverandThe Next Civil War: Dispatches from the American FuturePenilaian: 3.5 dari 5 bintang3.5/5 (48)

- The Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpDari EverandThe Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpPenilaian: 4.5 dari 5 bintang4.5/5 (11)

- The Courage to Be Free: Florida's Blueprint for America's RevivalDari EverandThe Courage to Be Free: Florida's Blueprint for America's RevivalBelum ada peringkat

- Crimes and Cover-ups in American Politics: 1776-1963Dari EverandCrimes and Cover-ups in American Politics: 1776-1963Penilaian: 4.5 dari 5 bintang4.5/5 (26)

- Game Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeDari EverandGame Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimePenilaian: 4 dari 5 bintang4/5 (572)

- The Red and the Blue: The 1990s and the Birth of Political TribalismDari EverandThe Red and the Blue: The 1990s and the Birth of Political TribalismPenilaian: 4 dari 5 bintang4/5 (29)

- Stonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonDari EverandStonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonPenilaian: 4.5 dari 5 bintang4.5/5 (21)

- The Science of Liberty: Democracy, Reason, and the Laws of NatureDari EverandThe Science of Liberty: Democracy, Reason, and the Laws of NatureBelum ada peringkat

- Bad Religion: How We Became a Nation of HereticsDari EverandBad Religion: How We Became a Nation of HereticsPenilaian: 4 dari 5 bintang4/5 (74)

- To Make Men Free: A History of the Republican PartyDari EverandTo Make Men Free: A History of the Republican PartyPenilaian: 4.5 dari 5 bintang4.5/5 (21)

- Witch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryDari EverandWitch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryPenilaian: 4 dari 5 bintang4/5 (6)

- The Invisible Bridge: The Fall of Nixon and the Rise of ReaganDari EverandThe Invisible Bridge: The Fall of Nixon and the Rise of ReaganPenilaian: 4.5 dari 5 bintang4.5/5 (32)

- The Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorDari EverandThe Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorBelum ada peringkat

- The Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaDari EverandThe Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaPenilaian: 4.5 dari 5 bintang4.5/5 (4)

- A Short History of the United States: From the Arrival of Native American Tribes to the Obama PresidencyDari EverandA Short History of the United States: From the Arrival of Native American Tribes to the Obama PresidencyPenilaian: 3.5 dari 5 bintang3.5/5 (19)

- Socialism 101: From the Bolsheviks and Karl Marx to Universal Healthcare and the Democratic Socialists, Everything You Need to Know about SocialismDari EverandSocialism 101: From the Bolsheviks and Karl Marx to Universal Healthcare and the Democratic Socialists, Everything You Need to Know about SocialismPenilaian: 4.5 dari 5 bintang4.5/5 (42)

- Resistance: How Women Saved Democracy from Donald TrumpDari EverandResistance: How Women Saved Democracy from Donald TrumpBelum ada peringkat

- Corruptible: Who Gets Power and How It Changes UsDari EverandCorruptible: Who Gets Power and How It Changes UsPenilaian: 4.5 dari 5 bintang4.5/5 (45)

- Slouching Towards Gomorrah: Modern Liberalism and American DeclineDari EverandSlouching Towards Gomorrah: Modern Liberalism and American DeclinePenilaian: 4 dari 5 bintang4/5 (59)

- Revealing the Wickedness of the American Government: Organized Stalking, Electronic Harassment, and Human ExperimentationDari EverandRevealing the Wickedness of the American Government: Organized Stalking, Electronic Harassment, and Human ExperimentationPenilaian: 5 dari 5 bintang5/5 (1)

- UFO: The Inside Story of the US Government's Search for Alien Life Here—and Out ThereDari EverandUFO: The Inside Story of the US Government's Search for Alien Life Here—and Out TherePenilaian: 4.5 dari 5 bintang4.5/5 (16)

- Manufacturing Consent: The Political Economy of the Mass MediaDari EverandManufacturing Consent: The Political Economy of the Mass MediaPenilaian: 4 dari 5 bintang4/5 (495)