Anda mungkin juga menyukai

- Illustration of Loneliness-B ClarinetDokumen1 halamanIllustration of Loneliness-B ClarinetfaithbuiBelum ada peringkat

- Accounting Exam BDokumen7 halamanAccounting Exam BfaithbuiBelum ada peringkat

- Piano Concerto No. 20Dokumen4 halamanPiano Concerto No. 20faithbuiBelum ada peringkat

- Piano Concerto No. 20Dokumen4 halamanPiano Concerto No. 20faithbuiBelum ada peringkat

- Piano Concerto No. 20 - Horn IIDokumen4 halamanPiano Concerto No. 20 - Horn IIfaithbuiBelum ada peringkat

- Piano Concerto No. 20 - Horn IIDokumen4 halamanPiano Concerto No. 20 - Horn IIfaithbuiBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5782)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- LG Oled65g6p T-Con Board Layout Voltages 2017Dokumen10 halamanLG Oled65g6p T-Con Board Layout Voltages 2017Fernando AguiarBelum ada peringkat

- Assassin Teens-Ryan, AvengerDokumen10 halamanAssassin Teens-Ryan, AvengerSunay BhagatBelum ada peringkat

- KENYA - Tourism Sector Perfomance Report - 2019Dokumen30 halamanKENYA - Tourism Sector Perfomance Report - 2019Paul UdotoBelum ada peringkat

- Puerto - Rico - Codes - 2018 Live LoadsDokumen2 halamanPuerto - Rico - Codes - 2018 Live LoadsAlex SanchezBelum ada peringkat

- Morbid Curiosities: The Art of Montague Rhodes JamesDokumen7 halamanMorbid Curiosities: The Art of Montague Rhodes JamesMatthew BanksBelum ada peringkat

- Codex 1Dokumen4 halamanCodex 1Juan Diego MartínezBelum ada peringkat

- Singular Subjects Verbs ExamplesDokumen2 halamanSingular Subjects Verbs Exampleseliza ismailBelum ada peringkat

- How To Make A Ship in A BottleDokumen3 halamanHow To Make A Ship in A BottlePranjal SoodBelum ada peringkat

- Viisan VK18 Book Scanner - BrochureDokumen16 halamanViisan VK18 Book Scanner - BrochureChristian Robert NalicaBelum ada peringkat

- Final PortfolioDokumen12 halamanFinal Portfolioapi-529179424Belum ada peringkat

- Blue DVD ListDokumen379 halamanBlue DVD ListMiranda FranklinBelum ada peringkat

- Mercantilism GameDokumen20 halamanMercantilism Gameapi-341406434Belum ada peringkat

- Top NotchersDokumen17 halamanTop NotchersKierk Robin RetBelum ada peringkat

- Lumi by Akira Back MenuDokumen3 halamanLumi by Akira Back MenuEaterSDBelum ada peringkat

- The Monkey and The CrocodileDokumen3 halamanThe Monkey and The Crocodileapi-3821467100% (3)

- Hip-Hop PPT DemoDokumen9 halamanHip-Hop PPT Demoapi-292940790100% (1)

- Goodtime Maintenance ManualDokumen24 halamanGoodtime Maintenance ManualRami TannousBelum ada peringkat

- A Friend Like Filby by Mark Wakely PDFDokumen302 halamanA Friend Like Filby by Mark Wakely PDFMark Wakely0% (1)

- Report LagDokumen312 halamanReport LagBulentDoganBelum ada peringkat

- Extra Credit Essay - AnthroDokumen4 halamanExtra Credit Essay - AnthroMeghan NanneyBelum ada peringkat

- #1 Sample EssaysDokumen4 halaman#1 Sample Essaysbersam05Belum ada peringkat

- What did you do last weekend sentencesDokumen3 halamanWhat did you do last weekend sentencesRONALDCONBelum ada peringkat

- Sports and Activities VocabularyDokumen1 halamanSports and Activities VocabularyMerida KimBelum ada peringkat

- Airblue TicketDokumen2 halamanAirblue TicketJawad Bashir67% (6)

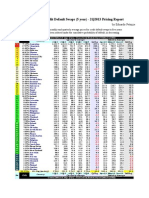

- Sovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportDokumen1 halamanSovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportEduardo PetazzeBelum ada peringkat

- Announcer: Welcome To The Essential Tennis Podcast. If You Lave Tennis and Wants ToDokumen9 halamanAnnouncer: Welcome To The Essential Tennis Podcast. If You Lave Tennis and Wants ToVicente SouzaBelum ada peringkat

- 7 - The Biliary TractDokumen48 halaman7 - The Biliary TractKim RamosBelum ada peringkat

- Boys Scout of The Philippines: Patrol Leaders Training CourseDokumen3 halamanBoys Scout of The Philippines: Patrol Leaders Training CourseHelen AlensonorinBelum ada peringkat

- 00 - Whatever People Say I Am, That's What I'm Not PDFDokumen151 halaman00 - Whatever People Say I Am, That's What I'm Not PDFbirajr78Belum ada peringkat

- Each) : Grammar 1 Write The Question For Each Following Answer. Example: She Played Basketball YesterdayDokumen17 halamanEach) : Grammar 1 Write The Question For Each Following Answer. Example: She Played Basketball YesterdayProduction PeachyBelum ada peringkat