Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Actuarial Advantage BookDokumen60 halamanActuarial Advantage BookAnonymous DLEF3GvBelum ada peringkat

- Financial Statement Anlysis 10e Subramanyam Wild Chapter 4 PDFDokumen43 halamanFinancial Statement Anlysis 10e Subramanyam Wild Chapter 4 PDFRyan75% (4)

- M A PlaybookDokumen24 halamanM A PlaybookDwayne JohnsonBelum ada peringkat

- A Financial Statement Analysis ProjectDokumen14 halamanA Financial Statement Analysis ProjectJibin Raju100% (1)

- Icici Loans and AdvancesDokumen88 halamanIcici Loans and AdvancesSaraswati Pratik0% (1)

- HDFC MergerDokumen20 halamanHDFC Mergershaleen bansalBelum ada peringkat

- M&A FinalDokumen64 halamanM&A FinalVanini ClaudeBelum ada peringkat

- Specialized Investments - g5Dokumen15 halamanSpecialized Investments - g5KaonashiBelum ada peringkat

- DONE BA 118.3 Module 2 Quiz 1answer KeyDokumen8 halamanDONE BA 118.3 Module 2 Quiz 1answer KeyRed Ashley De LeonBelum ada peringkat

- Midterm Long Quiz - Part 2Dokumen6 halamanMidterm Long Quiz - Part 2Chrismae Monteverde SantosBelum ada peringkat

- MultiplesDokumen49 halamanMultiplesDekov72Belum ada peringkat

- BE Unit III BFIADokumen178 halamanBE Unit III BFIAGaurav SwamyBelum ada peringkat

- Module 1Dokumen25 halamanModule 1Gowri MahadevBelum ada peringkat

- AGC PE Buyers Vista Apr 2020 - VimpDokumen47 halamanAGC PE Buyers Vista Apr 2020 - VimpKIM MALAR 22Belum ada peringkat

- Saln BlankDokumen3 halamanSaln BlankMariel Avilla Mercado-CortezBelum ada peringkat

- Daicii RanbaxyDokumen27 halamanDaicii RanbaxydimpledsmilesBelum ada peringkat

- Cuture AssignmentDokumen5 halamanCuture Assignmentvisha183240100% (1)

- Adv. Sachin M. Kalyankar: Kgis - Sachin@yahoo - Co.inDokumen8 halamanAdv. Sachin M. Kalyankar: Kgis - Sachin@yahoo - Co.inAdv. Sachin KalyankarBelum ada peringkat

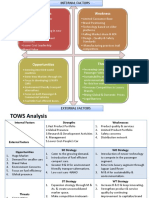

- Tata Motors SWOT TOWS CPM MatrixDokumen6 halamanTata Motors SWOT TOWS CPM MatrixTushar Ballabh50% (2)

- STM TataSteel Group7 SectionBDokumen53 halamanSTM TataSteel Group7 SectionBSiddharth Sharma100% (1)

- An Events Approach To Basic AccountingDokumen9 halamanAn Events Approach To Basic AccountingEycha ErozBelum ada peringkat

- Reverse Merger: Features of Reverse MergersDokumen3 halamanReverse Merger: Features of Reverse MergerssangeetagoeleBelum ada peringkat

- Aol 10QDokumen155 halamanAol 10QAnonymous 6tuR1hzBelum ada peringkat

- The Crisis Brewing Within The Indian Economy Has Gained Unanimous Acceptance by NowDokumen2 halamanThe Crisis Brewing Within The Indian Economy Has Gained Unanimous Acceptance by NowSyed fayas thanveer SBelum ada peringkat

- Business Combinations (Ifrs 3)Dokumen29 halamanBusiness Combinations (Ifrs 3)anon_253544781Belum ada peringkat

- 2009 Annual Report AXA Private EquityDokumen80 halaman2009 Annual Report AXA Private EquityGary ChanBelum ada peringkat

- Indonesia Palm Oil: Sector BriefingDokumen40 halamanIndonesia Palm Oil: Sector BriefingatanmasriBelum ada peringkat

- Mpe 506 NotesDokumen14 halamanMpe 506 NotesFancyfantastic KinuthiaBelum ada peringkat

- SBAProject FinalsDokumen5 halamanSBAProject Finalsjoy mesanaBelum ada peringkat

- Lesson 5 Koots Tea Case StudyDokumen10 halamanLesson 5 Koots Tea Case StudyBikram Prajapati100% (1)