Anda mungkin juga menyukai

- 29 9 13 Accounts SumsDokumen11 halaman29 9 13 Accounts SumssahilgeraBelum ada peringkat

- Prep Trading - Profit-And-Loss-Ac Balance SheetDokumen25 halamanPrep Trading - Profit-And-Loss-Ac Balance Sheetfaltumail379100% (1)

- Final AccountsDokumen27 halamanFinal AccountsNafis Siddiqui100% (1)

- Final Accounts Revision ProblemsDokumen4 halamanFinal Accounts Revision Problemsblazingsun_11Belum ada peringkat

- 11 Accountancy Notes Ch08 Financial Statements of Sole Proprietorship 02Dokumen9 halaman11 Accountancy Notes Ch08 Financial Statements of Sole Proprietorship 02Anonymous NSNpGa3T93100% (1)

- Final AccountsDokumen12 halamanFinal AccountsHarish SinghBelum ada peringkat

- Income Statement & Balance Sheet-1Dokumen18 halamanIncome Statement & Balance Sheet-1Shreyasi RanjanBelum ada peringkat

- Branch AccountsDokumen12 halamanBranch AccountsRobert Henson100% (1)

- 1.profit and Loss Account:: A.V.Harun Raaj SRO 0258424Dokumen15 halaman1.profit and Loss Account:: A.V.Harun Raaj SRO 0258424harunraajBelum ada peringkat

- Case 12Dokumen10 halamanCase 12Kashif KhurshidBelum ada peringkat

- Problems GeneralDokumen9 halamanProblems GeneralAmal BharaliBelum ada peringkat

- Final Acc-Numerical 1Dokumen10 halamanFinal Acc-Numerical 1Rajshree BhardwajBelum ada peringkat

- YuyutuDokumen15 halamanYuyutuDeepak R GoradBelum ada peringkat

- Excel Project EntrepreneurDokumen21 halamanExcel Project EntrepreneurshumailshauqueBelum ada peringkat

- 4.model Problems On Final AccountsDokumen4 halaman4.model Problems On Final Accountsparth38Belum ada peringkat

- Final AccDokumen13 halamanFinal Accmdr32000Belum ada peringkat

- PAL0022 T3 - Topic 3Dokumen10 halamanPAL0022 T3 - Topic 3Samuel KohBelum ada peringkat

- Income Statements 2010Dokumen10 halamanIncome Statements 2010Shivam GoelBelum ada peringkat

- Analysis of Financial StatementsDokumen33 halamanAnalysis of Financial StatementsKushal Lapasia100% (1)

- Financial Projection Template - NewDokumen5 halamanFinancial Projection Template - NewNorhisham DaudBelum ada peringkat

- 4.ratio Analysis Problems FormatDokumen5 halaman4.ratio Analysis Problems Formatparth38Belum ada peringkat

- Final AccountsDokumen5 halamanFinal AccountsGopal KrishnanBelum ada peringkat

- 7 Adjustments To Final AccountsDokumen11 halaman7 Adjustments To Final AccountsBhavneet SachdevaBelum ada peringkat

- Exercise (Final Accounts)Dokumen14 halamanExercise (Final Accounts)Abhishek BansalBelum ada peringkat

- David MAP 107Dokumen10 halamanDavid MAP 107Ridah SolomonBelum ada peringkat

- 1cash Flow Ques1Dokumen6 halaman1cash Flow Ques1Dhir ChaubeyBelum ada peringkat

- Mea CCSDokumen1 halamanMea CCSb21ai008Belum ada peringkat

- Final AccountDokumen47 halamanFinal Accountsakshi tomarBelum ada peringkat

- 2012 Final Exam SolutionDokumen14 halaman2012 Final Exam SolutionOmar Ahmed ElkhalilBelum ada peringkat

- Final AccountsDokumen12 halamanFinal Accountsanandm1986100% (1)

- Income Statement For The Year Ended 31-03-2012 Marks 12Dokumen2 halamanIncome Statement For The Year Ended 31-03-2012 Marks 12Anand RathiBelum ada peringkat

- Financial and Management Accounting Practice Questions - Set 2Dokumen4 halamanFinancial and Management Accounting Practice Questions - Set 2Reena GoswamiBelum ada peringkat

- Final Account BBADokumen37 halamanFinal Account BBAgrivand100% (1)

- Trading Account PDFDokumen9 halamanTrading Account PDFVijayaraj Jeyabalan100% (1)

- 7110 s05 QP 1Dokumen12 halaman7110 s05 QP 1kaviraj1006Belum ada peringkat

- AccountDokumen2 halamanAccountnomaanahmadshahBelum ada peringkat

- Final Accounts PPT APTDokumen36 halamanFinal Accounts PPT APTGaurav gusai100% (1)

- MIS Financials Format XlsMISDokumen78 halamanMIS Financials Format XlsMISarajamani78100% (1)

- Illustration: Particulars Rs. Particulars Rs. RsDokumen3 halamanIllustration: Particulars Rs. Particulars Rs. Rstinasoni11Belum ada peringkat

- ACT 501 - AssignmentDokumen6 halamanACT 501 - AssignmentShariful Islam ShaheenBelum ada peringkat

- Answer Sheet v-1 24052014Dokumen7 halamanAnswer Sheet v-1 24052014psawant77Belum ada peringkat

- Branch AccountDokumen78 halamanBranch AccountAlessandro MadauBelum ada peringkat

- ABE Dip 1 - Financial Accounting JUNE 2005Dokumen19 halamanABE Dip 1 - Financial Accounting JUNE 2005spinster40% (1)

- Accounting ProblemsDokumen9 halamanAccounting ProblemsMukta MattaBelum ada peringkat

- Final Accounts (Financial Statements)Dokumen6 halamanFinal Accounts (Financial Statements)Raaghav SrinivasanBelum ada peringkat

- Income StatementDokumen13 halamanIncome StatementThéotime HabinezaBelum ada peringkat

- (TR DR) (TR CR)Dokumen33 halaman(TR DR) (TR CR)sanddyhs2uBelum ada peringkat

- Loyola College (Autonomous), Chennai - 600 034.: First Semester - Nov 2005Dokumen4 halamanLoyola College (Autonomous), Chennai - 600 034.: First Semester - Nov 2005Charles VinothBelum ada peringkat

- Final Accounts With Out AdjustmentsDokumen2 halamanFinal Accounts With Out AdjustmentsMurari NayuduBelum ada peringkat

- Final AccountsDokumen20 halamanFinal AccountsSeri SummaBelum ada peringkat

- Branch AccountsDokumen4 halamanBranch Accountsnavin_raghuBelum ada peringkat

- Doubtful Debt and Bad DebtsDokumen6 halamanDoubtful Debt and Bad DebtskarimikaBelum ada peringkat

- Seminar Solutions - Term 2Dokumen36 halamanSeminar Solutions - Term 2bontom333Belum ada peringkat

- 01 Company Final Accounts QuestionsDokumen10 halaman01 Company Final Accounts QuestionsMd. Iqbal Hasan0% (1)

- Laundry - System Analysis and Design - (Excel Linking)Dokumen10 halamanLaundry - System Analysis and Design - (Excel Linking)JO SABelum ada peringkat

- Class Exercise AccountingDokumen4 halamanClass Exercise AccountingMohsin Farooq100% (1)

- Wholesalers Trade Agents & Broker Revenues World Summary: Market Values & Financials by CountryDari EverandWholesalers Trade Agents & Broker Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryDari EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Income Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawDari EverandIncome Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawPenilaian: 3.5 dari 5 bintang3.5/5 (4)

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersDari EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersBelum ada peringkat

- Introduction and Methodology: Determinants of GLP and Profitability of Selected MFI'sDokumen112 halamanIntroduction and Methodology: Determinants of GLP and Profitability of Selected MFI'sskibcobsaivigneshBelum ada peringkat

- Corporate Strategic Planning - Corporate Strategic PlanningCorporate Strategic PlanningCorporate Strategic PlanningCorporate Strategic PlanningDokumen29 halamanCorporate Strategic Planning - Corporate Strategic PlanningCorporate Strategic PlanningCorporate Strategic PlanningCorporate Strategic Planningskibcobsaivignesh50% (2)

- Accounting, Accounts, AccDokumen2 halamanAccounting, Accounts, AccskibcobsaivigneshBelum ada peringkat

- An Overview of Steel SectorDokumen18 halamanAn Overview of Steel SectorskibcobsaivigneshBelum ada peringkat

- Strategic BusinessDokumen71 halamanStrategic BusinessskibcobsaivigneshBelum ada peringkat

- Prasanth Report CorrectedDokumen40 halamanPrasanth Report CorrectedskibcobsaivigneshBelum ada peringkat

- Consumer Behaviour PDFDokumen99 halamanConsumer Behaviour PDFskibcobsaivigneshBelum ada peringkat

- Ministry of Financelfks FLK SF SLFLSFLSKF SKF SKF LDokumen5 halamanMinistry of Financelfks FLK SF SLFLSFLSKF SKF SKF LskibcobsaivigneshBelum ada peringkat

- Acc 1k Askf - Fos.m, Lafojzaf,.masf Kljmafdasfm - Fopjer.,mfl Maf Lkjaf. Masf LKF Lkasf LkafDokumen42 halamanAcc 1k Askf - Fos.m, Lafojzaf,.masf Kljmafdasfm - Fopjer.,mfl Maf Lkjaf. Masf LKF Lkasf LkafskibcobsaivigneshBelum ada peringkat

- SCM, Third Party Logistics, 3PL, Supply Chain ManagementDokumen151 halamanSCM, Third Party Logistics, 3PL, Supply Chain ManagementskibcobsaivigneshBelum ada peringkat

- Project GuidanceDokumen17 halamanProject GuidanceTulsi MahtoBelum ada peringkat

- Consumer Perception of Mobile Telephony Tariffs With Cost CapsDokumen8 halamanConsumer Perception of Mobile Telephony Tariffs With Cost CapsskibcobsaivigneshBelum ada peringkat

- Introductionklsfjsfjsjfjdsfjklnsd,mflnklnsdvnnxvoklnxvnnxcvklnxnv,mnxcvkllkn,vmnx,mvn,mn,nxvln,mxnv,mnxv,n,xvn,xnv,m,xnv,mnx,vnkljflnsonkln,xnvxv,n,mvkllnf,nvlknxv,n,xv,mnxv,mn,xmvn,mnxv,mnxvnxv,nvlm,nxv,n,nxv,lnx,v,xvn,xvn,nxv,,n,,mn,fs,msf,msnf,ns,fns,fsfms,mfnnsfnsf.mf.msf.msf,.sfmmsfsmf,.smmsf.msfmsmfsmf.smfsklmsdf.,mfs.msmy.tmusmgfsutmfrs.umtr,f.mustyusmrtu,.smrs.ymfryDokumen4 halamanIntroductionklsfjsfjsjfjdsfjklnsd,mflnklnsdvnnxvoklnxvnnxcvklnxnv,mnxcvkllkn,vmnx,mvn,mn,nxvln,mxnv,mnxv,n,xvn,xnv,m,xnv,mnx,vnkljflnsonkln,xnvxv,n,mvkllnf,nvlknxv,n,xv,mnxv,mn,xmvn,mnxv,mnxvnxv,nvlm,nxv,n,nxv,lnx,v,xvn,xvn,nxv,,n,,mn,fs,msf,msnf,ns,fns,fsfms,mfnnsfnsf.mf.msf.msf,.sfmmsfsmf,.smmsf.msfmsmfsmf.smfsklmsdf.,mfs.msmy.tmusmgfsutmfrs.umtr,f.mustyusmrtu,.smrs.ymfryskibcobsaivigneshBelum ada peringkat

- SCM, Supply Chain Management, Third Party LogisticsDokumen72 halamanSCM, Supply Chain Management, Third Party LogisticsskibcobsaivigneshBelum ada peringkat

- Third Party Logistics Providers (3PL) : Kyle Sera Amy Irvine Scott Andrew Carrie Schmidt Ryan LancasterDokumen23 halamanThird Party Logistics Providers (3PL) : Kyle Sera Amy Irvine Scott Andrew Carrie Schmidt Ryan LancasterJayajoannBelum ada peringkat

- Store Operation PDFDokumen128 halamanStore Operation PDFskibcobsaivigneshBelum ada peringkat

- Quality Online Banking ServicesDokumen79 halamanQuality Online Banking ServicesTinh ThuyBelum ada peringkat

- Supply Chain ManagementDokumen15 halamanSupply Chain ManagementskibcobsaivigneshBelum ada peringkat

- Supply Chain Management, 3PLDokumen4 halamanSupply Chain Management, 3PLskibcobsaivigneshBelum ada peringkat

- Store Operation PDFDokumen128 halamanStore Operation PDFskibcobsaivigneshBelum ada peringkat

- 3 RD Party LogisticsDokumen51 halaman3 RD Party LogisticsmotabhaBelum ada peringkat

- Supply Chain ManagementDokumen15 halamanSupply Chain ManagementskibcobsaivigneshBelum ada peringkat

- Supply Chain Management, 3PLDokumen4 halamanSupply Chain Management, 3PLskibcobsaivigneshBelum ada peringkat

- Consumer Behaviour PDFDokumen99 halamanConsumer Behaviour PDFskibcobsaivigneshBelum ada peringkat

- Multi-Channel Consumer Perceptions: Teltzrow@wiwi - Hu-Berlin - deDokumen14 halamanMulti-Channel Consumer Perceptions: Teltzrow@wiwi - Hu-Berlin - deSivanaga MalleshBelum ada peringkat

- Consumer Perception of Mobile Telephony Tariffs With Cost CapsDokumen8 halamanConsumer Perception of Mobile Telephony Tariffs With Cost CapsskibcobsaivigneshBelum ada peringkat

- Supply Chain Management: Vinod Gupta School of Management (VGSOM) Indian Institute of Technology KharagpurDokumen6 halamanSupply Chain Management: Vinod Gupta School of Management (VGSOM) Indian Institute of Technology KharagpurskibcobsaivigneshBelum ada peringkat

- Supply Chain ManagementDokumen27 halamanSupply Chain ManagementskibcobsaivigneshBelum ada peringkat

- Supply Chain Management, 3PLDokumen4 halamanSupply Chain Management, 3PLskibcobsaivigneshBelum ada peringkat

- TAX CIR Vs IsabelaDokumen1 halamanTAX CIR Vs IsabelaEly VelascoBelum ada peringkat

- Ch09Part02.Home Office and Branch Accounting (Special Problems) PDFDokumen2 halamanCh09Part02.Home Office and Branch Accounting (Special Problems) PDFStephanie Ann AsuncionBelum ada peringkat

- Wall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto CurrenciesDokumen139 halamanWall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto Currenciesboo100% (5)

- Gst-ChallanDokumen2 halamanGst-Challandeepak kumarBelum ada peringkat

- Problems in AccountingDokumen4 halamanProblems in AccountingRaul Soriano CabantingBelum ada peringkat

- Northern Rock 2Dokumen19 halamanNorthern Rock 2banksternation100% (1)

- Cambridge International General Certificate of Secondary EducationDokumen20 halamanCambridge International General Certificate of Secondary EducationAung Zaw HtweBelum ada peringkat

- TaxInvoice PDFDokumen1 halamanTaxInvoice PDFponiteBelum ada peringkat

- Commercial Bank PDFDokumen13 halamanCommercial Bank PDFTanhaBelum ada peringkat

- Sample Letter - Explanation For Delinquent PaymentDokumen2 halamanSample Letter - Explanation For Delinquent PaymentJ Stocker100% (2)

- Paychecks Crossword PuzzleDokumen1 halamanPaychecks Crossword Puzzleapi-2760115920% (3)

- Fin Mar-Chapter9Dokumen2 halamanFin Mar-Chapter9EANNA15Belum ada peringkat

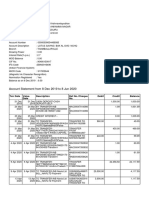

- Account Statement From 8 Dec 2019 To 8 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen6 halamanAccount Statement From 8 Dec 2019 To 8 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceMUTHYALA NEERAJABelum ada peringkat

- Classification of Income TaxDokumen1 halamanClassification of Income TaxKrizel DABelum ada peringkat

- What's Going On 2019 - Cornerstone AdvisorsDokumen35 halamanWhat's Going On 2019 - Cornerstone AdvisorsVivekBelum ada peringkat

- Partner Ship - IIDokumen6 halamanPartner Ship - IIM JEEVARATHNAM NAIDUBelum ada peringkat

- Valmiki Shiksha Sadan H. S. S.: Sent Up Examination-2071Dokumen3 halamanValmiki Shiksha Sadan H. S. S.: Sent Up Examination-2071Rabindra Raj BistaBelum ada peringkat

- Scope and LimitationDokumen5 halamanScope and LimitationVivek Kumar50% (4)

- Qualified Written RequestDokumen2 halamanQualified Written Request3rdforceent100% (1)

- Slides Week 2 PDFDokumen91 halamanSlides Week 2 PDFYash ModiBelum ada peringkat

- Ch02 Mini CaseDokumen5 halamanCh02 Mini CaseJosé Augusto BernabéBelum ada peringkat

- 8 LPC-format PDFDokumen2 halaman8 LPC-format PDFKamran AliBelum ada peringkat

- Case AnalysisDokumen3 halamanCase Analysisanjali shilpa kajalBelum ada peringkat

- Salary Presentation 1Dokumen56 halamanSalary Presentation 1NIRAVBelum ada peringkat

- Assessment 2: InstructionsDokumen5 halamanAssessment 2: InstructionsThiago FlorianoBelum ada peringkat

- Daguhoy Enterprises, Inc. vs. Ponce G.R. No. L-6515, October 18, 1954 96 Phil 15Dokumen2 halamanDaguhoy Enterprises, Inc. vs. Ponce G.R. No. L-6515, October 18, 1954 96 Phil 15Hope Trinity Enriquez100% (1)

- Copy B To Be Filed With Employee S FEDERAL Tax Return: See Instructions For Box 12Dokumen3 halamanCopy B To Be Filed With Employee S FEDERAL Tax Return: See Instructions For Box 12memek1123Belum ada peringkat

- Doing Business in Oman: A Tax and Legal GuideDokumen16 halamanDoing Business in Oman: A Tax and Legal GuideAnand PrakashBelum ada peringkat

- Memorandum of Association OF ThanniDokumen4 halamanMemorandum of Association OF ThanniDHRUVINKUMAR CHAUHANBelum ada peringkat

- Peta 2Dokumen5 halamanPeta 2JebEscuetaAriolaBelum ada peringkat