Anda mungkin juga menyukai

- Risky InvestmentDokumen35 halamanRisky InvestmentbellohalesBelum ada peringkat

- Financial DerivativesDokumen30 halamanFinancial DerivativesBevBelum ada peringkat

- BKM, Chap 16Dokumen16 halamanBKM, Chap 16rob_jiangBelum ada peringkat

- Soln CH 20 Option IntroDokumen14 halamanSoln CH 20 Option IntroSilviu TrebuianBelum ada peringkat

- BRIGHAM CH 19 SM 3ce - REVISEDDokumen11 halamanBRIGHAM CH 19 SM 3ce - REVISEDVu Khanh LeBelum ada peringkat

- SOA MFE 76 Practice Ques SolsDokumen70 halamanSOA MFE 76 Practice Ques SolsGracia DongBelum ada peringkat

- FINS2624 Problem Set 9 SolutionsDokumen9 halamanFINS2624 Problem Set 9 SolutionssdfklmjsdlklskfjdBelum ada peringkat

- Week 3 Solutions To ExercisesDokumen6 halamanWeek 3 Solutions To ExercisesBerend van RoozendaalBelum ada peringkat

- MFE SampleQS1-76Dokumen185 halamanMFE SampleQS1-76Jihyeon Kim100% (1)

- Week 9. Problems - OptionDokumen16 halamanWeek 9. Problems - OptionMarissa MarissaBelum ada peringkat

- Edu 2009 Spring Exam Mfe QaDokumen154 halamanEdu 2009 Spring Exam Mfe QaYan David WangBelum ada peringkat

- Binomial and Black Scholes - 111153Dokumen18 halamanBinomial and Black Scholes - 111153merijan31773Belum ada peringkat

- Fin 6515 Solutions To Problems On FuturesDokumen1 halamanFin 6515 Solutions To Problems On FuturesZion WilliamsBelum ada peringkat

- Lecture 22Dokumen40 halamanLecture 22Rita ChetwaniBelum ada peringkat

- Exam FM Sample SolutionsDokumen13 halamanExam FM Sample SolutionsLueshen Wellington100% (1)

- Chapter 9Dokumen7 halamanChapter 9sylbluebubblesBelum ada peringkat

- Pricingoptions by BlackscholesDokumen98 halamanPricingoptions by BlackscholesNitish TanwarBelum ada peringkat

- Hw4 Mfe Au14 SolutionDokumen7 halamanHw4 Mfe Au14 SolutionWenn ZhangBelum ada peringkat

- Finance Questions and SolutionsDokumen10 halamanFinance Questions and SolutionsEli Koech100% (1)

- Pset 03 Spring2020 SolutionsDokumen15 halamanPset 03 Spring2020 Solutionsjoshua arnettBelum ada peringkat

- Lect6 OptionsDokumen35 halamanLect6 OptionsAllen GrceBelum ada peringkat

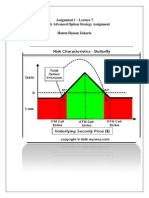

- Butterfly Advanced Option Strategy AssignmentDokumen3 halamanButterfly Advanced Option Strategy AssignmentHatem HassanBelum ada peringkat

- Ps Options SolutionsDokumen18 halamanPs Options SolutionsjahanzebibaBelum ada peringkat

- Sample Questions Test 3 - Final-2017spDokumen5 halamanSample Questions Test 3 - Final-2017spchocolatedoggy12Belum ada peringkat

- The Binomial Model For Pricing OptionsDokumen4 halamanThe Binomial Model For Pricing OptionsFlorencia Tiffany WijayaBelum ada peringkat

- Ch08 Solutions ManualDokumen4 halamanCh08 Solutions ManualKUSUMA WIDYA TANTRIBelum ada peringkat

- Tutorial 11 Binomial Option PricingDokumen3 halamanTutorial 11 Binomial Option PricingHenry Ng Yong KangBelum ada peringkat

- Brealey. Myers. Allen Chapter 21 TestDokumen15 halamanBrealey. Myers. Allen Chapter 21 TestSasha100% (1)

- Assingnment: Ch#4 (Options Market and Contracts)Dokumen10 halamanAssingnment: Ch#4 (Options Market and Contracts)Mahnoor ShahbazBelum ada peringkat

- Practice 4 AnsDokumen4 halamanPractice 4 AnsAnonymous RWwhsCNBRBelum ada peringkat

- Financial Derivative (90 M Session)Dokumen33 halamanFinancial Derivative (90 M Session)nicero555Belum ada peringkat

- Derivative Markets Solutions'Dokumen30 halamanDerivative Markets Solutions'Kamy ZhuBelum ada peringkat

- ECO4108Z Futures, Options, DerivativesDokumen4 halamanECO4108Z Futures, Options, DerivativesnondweBelum ada peringkat

- MGMT 41150 Final Practice Questions - KeyDokumen3 halamanMGMT 41150 Final Practice Questions - KeyLaxus Dreyer0% (1)

- Financial Derivatives: Reference: Chapter 10, FFOM BookDokumen24 halamanFinancial Derivatives: Reference: Chapter 10, FFOM BookAnonymous tgYyno0w6Belum ada peringkat

- Mini Case Chapter 8Dokumen8 halamanMini Case Chapter 8William Y. OspinaBelum ada peringkat

- Msc. Accounting and FinanceDokumen18 halamanMsc. Accounting and FinancerytchluvBelum ada peringkat

- Properties of Stock Option PricesDokumen27 halamanProperties of Stock Option PricesPatriciaBelum ada peringkat

- Chapter 6Dokumen23 halamanChapter 6Majd AbukharmahBelum ada peringkat

- Binomial Option Pricing ModelDokumen27 halamanBinomial Option Pricing ModelParthapratim Debnath50% (2)

- Fundamentals of Futures and Options Markets Edition 7 CH 12 Problem SolutionsDokumen10 halamanFundamentals of Futures and Options Markets Edition 7 CH 12 Problem SolutionsMichael Evans100% (2)

- Derivative Markets SolutionsDokumen30 halamanDerivative Markets Solutionsnk7350100% (2)

- Assignment5-MockExam - Jupyter Notebook-1Dokumen5 halamanAssignment5-MockExam - Jupyter Notebook-1Ravi RaushanBelum ada peringkat

- Measures of Central TendencyDokumen18 halamanMeasures of Central TendencySANIUL ISLAM100% (1)

- 6 - Tutorial FINS3625S2Yr2018Week 6 Tutorial SolutionsDokumen9 halaman6 - Tutorial FINS3625S2Yr2018Week 6 Tutorial SolutionsChrisBelum ada peringkat

- Final Exam Mock SolutionsDokumen7 halamanFinal Exam Mock Solutionskokmunwai717Belum ada peringkat

- Mfe Sample Questions Solutions Adv DerivativesDokumen93 halamanMfe Sample Questions Solutions Adv DerivativesLetsogile BaloiBelum ada peringkat

- Delta and GammaDokumen69 halamanDelta and GammaHarleen KaurBelum ada peringkat

- Tutorial Solutions Week 11Dokumen3 halamanTutorial Solutions Week 11Jaden EuBelum ada peringkat

- GROUP9 Chapter10 Decision TheoryDokumen37 halamanGROUP9 Chapter10 Decision TheoryAndrei Nicole Mendoza RiveraBelum ada peringkat

- Hw2 Suggested SolutionDokumen4 halamanHw2 Suggested Solutionandrewsource1Belum ada peringkat

- Manual To ShreveDokumen64 halamanManual To ShreveIvan Tay100% (1)

- Chap 5Dokumen52 halamanChap 5august mayBelum ada peringkat

- SolutionsDokumen8 halamanSolutionsJavid BalakishiyevBelum ada peringkat

- FINS2624 Problem Set 10 SolutionDokumen5 halamanFINS2624 Problem Set 10 SolutionsdfklmjsdlklskfjdBelum ada peringkat

- Group 14 Options Pricing Model Questions Block 3Dokumen9 halamanGroup 14 Options Pricing Model Questions Block 3Mark AdrianBelum ada peringkat

- Soln CH 21 Option ValDokumen10 halamanSoln CH 21 Option ValSilviu TrebuianBelum ada peringkat

- FIN3621 Review 9Dokumen2 halamanFIN3621 Review 9KhoaNamNguyenBelum ada peringkat

- Differentiation (Calculus) Mathematics Question BankDari EverandDifferentiation (Calculus) Mathematics Question BankPenilaian: 4 dari 5 bintang4/5 (1)

- Schiffman CB10 PPT 01Dokumen32 halamanSchiffman CB10 PPT 01via86100% (1)

- CFA Lecture 4 Examples Suggested SolutionsDokumen22 halamanCFA Lecture 4 Examples Suggested SolutionsSharul Islam100% (1)

- Your Index ReportDokumen1 halamanYour Index ReportSharul IslamBelum ada peringkat

- Digital Marketing Boot Camp CurriculumDokumen6 halamanDigital Marketing Boot Camp CurriculumSharul IslamBelum ada peringkat

- Brooks Kubik - Dinosaur TrainingDokumen98 halamanBrooks Kubik - Dinosaur TrainingMark PetrovichBelum ada peringkat

- A Pure Herbal Soap: Feel The Nature On Your SkinDokumen15 halamanA Pure Herbal Soap: Feel The Nature On Your SkinSharul IslamBelum ada peringkat

- Financial Ratio AnalysisDokumen1 halamanFinancial Ratio AnalysisSharul IslamBelum ada peringkat

- Roses DigbyDokumen46 halamanRoses DigbySharul IslamBelum ada peringkat

- Derivative Security QuestionDokumen5 halamanDerivative Security QuestionSharul IslamBelum ada peringkat

- Derivative SecurityDokumen1 halamanDerivative SecuritySharul IslamBelum ada peringkat

- Market Resesearch QuestionnaireDokumen5 halamanMarket Resesearch QuestionnaireSharul IslamBelum ada peringkat

- Research Proposal GuideDokumen4 halamanResearch Proposal GuideSharul IslamBelum ada peringkat

- Proposal ProposalDokumen3 halamanProposal ProposalSharul IslamBelum ada peringkat

- Exploratory Research: Analysis of Data CollectedDokumen4 halamanExploratory Research: Analysis of Data CollectedSharul IslamBelum ada peringkat

- Decision Model in MarketingDokumen28 halamanDecision Model in MarketingSharul IslamBelum ada peringkat

- Corporate Finance Assignment MBSDokumen14 halamanCorporate Finance Assignment MBSSharul IslamBelum ada peringkat

- International Marketing ProjectDokumen85 halamanInternational Marketing ProjectSharul IslamBelum ada peringkat

- MBS CF ASsignment 1Dokumen11 halamanMBS CF ASsignment 1Sharul IslamBelum ada peringkat

- Vietnam PR Agency Tender Invitation and Brief (Project Basis) - MSLDokumen9 halamanVietnam PR Agency Tender Invitation and Brief (Project Basis) - MSLtranyenminh12Belum ada peringkat

- Family Code Cases Full TextDokumen69 halamanFamily Code Cases Full TextNikki AndradeBelum ada peringkat

- Ia Prompt 12 Theme: Knowledge and Knower "Is Bias Inevitable in The Production of Knowledge?"Dokumen2 halamanIa Prompt 12 Theme: Knowledge and Knower "Is Bias Inevitable in The Production of Knowledge?"Arham ShahBelum ada peringkat

- Swepp 1Dokumen11 halamanSwepp 1Augusta Altobar100% (2)

- BorgWarner v. Pierburg Et. Al.Dokumen9 halamanBorgWarner v. Pierburg Et. Al.PriorSmartBelum ada peringkat

- DPS Quarterly Exam Grade 9Dokumen3 halamanDPS Quarterly Exam Grade 9Michael EstrellaBelum ada peringkat

- OD428150379753135100Dokumen1 halamanOD428150379753135100Sourav SantraBelum ada peringkat

- Cagayan Capitol Valley Vs NLRCDokumen7 halamanCagayan Capitol Valley Vs NLRCvanessa_3Belum ada peringkat

- Ashish TPR AssignmentDokumen12 halamanAshish TPR Assignmentpriyesh20087913Belum ada peringkat

- Conflict Resolution in ChinaDokumen26 halamanConflict Resolution in ChinaAurora Dekoninck-MilitaruBelum ada peringkat

- Book Item 97952Dokumen18 halamanBook Item 97952Shairah May MendezBelum ada peringkat

- The Absent Presence of Progressive Rock in The British Music Press 1968 1974 PDFDokumen33 halamanThe Absent Presence of Progressive Rock in The British Music Press 1968 1974 PDFwago_itBelum ada peringkat

- CLOUDDokumen2 halamanCLOUDSawan AgarwalBelum ada peringkat

- CMSPCOR02T Final Question Paper 2022Dokumen2 halamanCMSPCOR02T Final Question Paper 2022DeepBelum ada peringkat

- Modern Dispatch - Cyberpunk Adventure GeneratorDokumen6 halamanModern Dispatch - Cyberpunk Adventure Generatorkarnoparno2Belum ada peringkat

- Official Directory of The European Union 2012Dokumen560 halamanOfficial Directory of The European Union 2012André Paula SantosBelum ada peringkat

- Test Bank For Global 4 4th Edition Mike PengDokumen9 halamanTest Bank For Global 4 4th Edition Mike PengPierre Wetzel100% (32)

- MhfdsbsvslnsafvjqjaoaodldananDokumen160 halamanMhfdsbsvslnsafvjqjaoaodldananLucijanBelum ada peringkat

- A.jjeb.g.p 2019Dokumen4 halamanA.jjeb.g.p 2019angellajordan123Belum ada peringkat

- Webinar2021 Curriculum Alena Frid OECDDokumen30 halamanWebinar2021 Curriculum Alena Frid OECDreaderjalvarezBelum ada peringkat

- Student Name: - : Question DetailsDokumen105 halamanStudent Name: - : Question Detailsyea okayBelum ada peringkat

- Department of Planning and Community Development: Organizational ChartDokumen5 halamanDepartment of Planning and Community Development: Organizational ChartkeithmontpvtBelum ada peringkat

- Creative Writing PieceDokumen3 halamanCreative Writing Pieceapi-608098440Belum ada peringkat

- Teaching Resume-Anna BedillionDokumen3 halamanTeaching Resume-Anna BedillionAnna Adams ProctorBelum ada peringkat

- Tok SB Ibdip Ch1Dokumen16 halamanTok SB Ibdip Ch1Luis Andrés Arce SalazarBelum ada peringkat

- Vodafone Training Induction PPT UpdatedDokumen39 halamanVodafone Training Induction PPT Updatedeyad mohamadBelum ada peringkat

- Pol Parties PDFDokumen67 halamanPol Parties PDFlearnmorBelum ada peringkat

- WAS 101 EditedDokumen132 halamanWAS 101 EditedJateni joteBelum ada peringkat

- Bangladesh Labor Law HandoutDokumen18 halamanBangladesh Labor Law HandoutMd. Mainul Ahsan SwaadBelum ada peringkat

- People vs. DonesaDokumen11 halamanPeople vs. DonesaEarlene DaleBelum ada peringkat