Anda mungkin juga menyukai

- IiG OxREP Adam DerconDokumen21 halamanIiG OxREP Adam DerconSamson SeiduBelum ada peringkat

- 1933162Dokumen273 halaman1933162Samson SeiduBelum ada peringkat

- Chapter One Introduction 1Dokumen7 halamanChapter One Introduction 1Samson SeiduBelum ada peringkat

- Peoples and Empires of West Africa in History 1000-1800Dokumen134 halamanPeoples and Empires of West Africa in History 1000-1800Samson SeiduBelum ada peringkat

- Michel LévyColorChartDokumen1 halamanMichel LévyColorChartSamson SeiduBelum ada peringkat

- Land LawDokumen11 halamanLand LawSamson SeiduBelum ada peringkat

- FredDokumen6 halamanFredSamson SeiduBelum ada peringkat

- 9340 36297 1 PBDokumen11 halaman9340 36297 1 PBSamson SeiduBelum ada peringkat

- Doctoral Programme Business 2016-2Dokumen6 halamanDoctoral Programme Business 2016-2Samson SeiduBelum ada peringkat

- References ListDokumen2 halamanReferences ListSamson SeiduBelum ada peringkat

- MaconDokumen1 halamanMaconSamson SeiduBelum ada peringkat

- 02 WholeDokumen405 halaman02 WholeSamson Seidu100% (1)

- Carbon Sequestration in The OceanDokumen32 halamanCarbon Sequestration in The OceanSamson SeiduBelum ada peringkat

- Mercy Chapter TwoDokumen11 halamanMercy Chapter TwoSamson SeiduBelum ada peringkat

- Hutu and TutsiDokumen15 halamanHutu and TutsiSamson SeiduBelum ada peringkat

- Land Law IIDokumen139 halamanLand Law IISamson SeiduBelum ada peringkat

- TEACHER VIEWS ON EXPLANATIONS IN MATHDokumen9 halamanTEACHER VIEWS ON EXPLANATIONS IN MATHSamson SeiduBelum ada peringkat

- Whatsup WordDokumen2 halamanWhatsup WordSamson SeiduBelum ada peringkat

- Guidance and Counselling PracticumDokumen67 halamanGuidance and Counselling PracticumSamson Seidu75% (4)

- Nigeria Basic Science v3Dokumen75 halamanNigeria Basic Science v3Samson SeiduBelum ada peringkat

- Chapter One: 1.1 Background of The StudyDokumen20 halamanChapter One: 1.1 Background of The StudySamson SeiduBelum ada peringkat

- Catholic Young Adult Association (Cyaa) MeetingDokumen2 halamanCatholic Young Adult Association (Cyaa) MeetingSamson SeiduBelum ada peringkat

- PneumoniaDokumen7 halamanPneumoniaseidu86Belum ada peringkat

- Likely Questions For AppointmentDokumen2 halamanLikely Questions For AppointmentSamson SeiduBelum ada peringkat

- Property Law PrecedentDokumen29 halamanProperty Law PrecedentSamson SeiduBelum ada peringkat

- TEACHER VIEWS ON EXPLANATIONS IN MATHDokumen9 halamanTEACHER VIEWS ON EXPLANATIONS IN MATHSamson SeiduBelum ada peringkat

- Taofik's DocsDokumen5 halamanTaofik's DocsSamson SeiduBelum ada peringkat

- Traditional Taboo Practices On Resource Conservation in Uli PDFDokumen14 halamanTraditional Taboo Practices On Resource Conservation in Uli PDFSamson SeiduBelum ada peringkat

- Igbo QuestionDokumen2 halamanIgbo QuestionSamson SeiduBelum ada peringkat

- Innocent's Front PagesDokumen7 halamanInnocent's Front PagesSamson SeiduBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- BD 135 y BD136 PNP NPN Transistores de PotenciaDokumen9 halamanBD 135 y BD136 PNP NPN Transistores de PotenciaMario A StBelum ada peringkat

- PCDA-Rev Advisory For Pensioners SPARSHDokumen5 halamanPCDA-Rev Advisory For Pensioners SPARSHSandeep KumarBelum ada peringkat

- Revision 2 - Investment AppraisalDokumen27 halamanRevision 2 - Investment AppraisalVishal PrasadBelum ada peringkat

- CU v. State Department FOIA Lawsuit (George Kent Emails On Biden-Burisma)Dokumen4 halamanCU v. State Department FOIA Lawsuit (George Kent Emails On Biden-Burisma)Citizens UnitedBelum ada peringkat

- Jaeger ChartDokumen1 halamanJaeger ChartTechnical A-Star Testing & Inspection MalaysiaBelum ada peringkat

- Public International Law-Nationality and StatelessnessDokumen6 halamanPublic International Law-Nationality and StatelessnessElias A ApallaBelum ada peringkat

- Profiles of KPK MpasDokumen51 halamanProfiles of KPK Mpasapi-243100634Belum ada peringkat

- Go Lackawanna 05-29-2011Dokumen56 halamanGo Lackawanna 05-29-2011The Times LeaderBelum ada peringkat

- Men Who Buy SexDokumen32 halamanMen Who Buy SexRed Fox100% (1)

- The Mighty Brush Painting Guide Death Korps of Krieg 143rd LegionDokumen20 halamanThe Mighty Brush Painting Guide Death Korps of Krieg 143rd LegionAitor RomeroBelum ada peringkat

- Producers Bank case study: Enhancing reporting & analyticsDokumen3 halamanProducers Bank case study: Enhancing reporting & analyticsvictorious xtremeBelum ada peringkat

- Application Reference No.: 102099: Applied Post DetailsDokumen1 halamanApplication Reference No.: 102099: Applied Post DetailsPRIYANSHI SRIVASTAVABelum ada peringkat

- BoardingCard 208248333 DSA CLJ PDFDokumen1 halamanBoardingCard 208248333 DSA CLJ PDFLechintan MarianaBelum ada peringkat

- Written Assignment: Residential Property Management NSW (CIVREP-NSW3 - AS - v2)Dokumen95 halamanWritten Assignment: Residential Property Management NSW (CIVREP-NSW3 - AS - v2)swati raghuvansiBelum ada peringkat

- The Political System of The European UnionDokumen6 halamanThe Political System of The European UnionLacramioara StoianBelum ada peringkat

- Official Report of Governor Izquierdo On The Cavite Mutiny of 1872Dokumen2 halamanOfficial Report of Governor Izquierdo On The Cavite Mutiny of 1872202280369Belum ada peringkat

- Bilchitz and Landau - The Evolution of The Separation of PowersDokumen146 halamanBilchitz and Landau - The Evolution of The Separation of PowersJose Almanza MacedoBelum ada peringkat

- Boy Proposing To Girl Drawing - Google SearchDokumen1 halamanBoy Proposing To Girl Drawing - Google SearchMaria RobellonBelum ada peringkat

- Fringe Benefit Tax - Nov 06Dokumen27 halamanFringe Benefit Tax - Nov 06Renievave TorculasBelum ada peringkat

- History of Stock BrokingDokumen4 halamanHistory of Stock BrokingDiwakar SinghBelum ada peringkat

- Windows Registry AnalysisDokumen62 halamanWindows Registry AnalysisSyeda Ashifa Ashrafi PapiaBelum ada peringkat

- STLA (Stellantis N.V.) Annual and Transition Report of Foreign Private Issuers (Sections 13 or 15 (D) ) (20-F) 2024-02-22.pdfDokumen335 halamanSTLA (Stellantis N.V.) Annual and Transition Report of Foreign Private Issuers (Sections 13 or 15 (D) ) (20-F) 2024-02-22.pdfMario MaldonadoBelum ada peringkat

- Patchouli Oil MSDS: Section 1: Chemical Product and Company IdentificationDokumen5 halamanPatchouli Oil MSDS: Section 1: Chemical Product and Company IdentificationMutriono OzhoraBelum ada peringkat

- CIS - Alberto Cortés Gonzalez - 2022Dokumen6 halamanCIS - Alberto Cortés Gonzalez - 2022luz marina LopezBelum ada peringkat

- 095 Lee Vs CADokumen2 halaman095 Lee Vs CAjoyce100% (3)

- What is the public cloud? - Under 40 characterDokumen16 halamanWhat is the public cloud? - Under 40 characterSergio Carrillo DiestraBelum ada peringkat

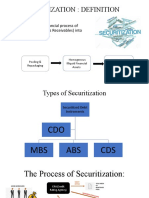

- SECURITIZATIONDokumen5 halamanSECURITIZATIONASHISH KUMARBelum ada peringkat

- Securities and Exchange CommissionDokumen4 halamanSecurities and Exchange CommissionJhoy PuruggananBelum ada peringkat

- Is 3156 2 1992 PDFDokumen8 halamanIs 3156 2 1992 PDFgurdeep singhBelum ada peringkat

- CIPT Onl Mod2Transcript PDFDokumen11 halamanCIPT Onl Mod2Transcript PDFChrist SierraBelum ada peringkat