Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Capital Returns 2 PDFDokumen12 halamanCapital Returns 2 PDFNivesh Pande100% (1)

- Questions For GE Imagination (Answers)Dokumen4 halamanQuestions For GE Imagination (Answers)Gavin PereiraBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Princes of YenDokumen90 halamanPrinces of Yenjpfunds100% (3)

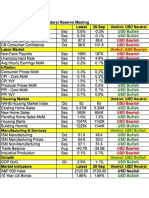

- US Economy Fed Reserve Indicators - JPGDokumen1 halamanUS Economy Fed Reserve Indicators - JPGvmmatt23Belum ada peringkat

- Basking Ridge - A Rich HamletDokumen5 halamanBasking Ridge - A Rich Hamletvmmatt23Belum ada peringkat

- Blazing Chicken KabobsDokumen2 halamanBlazing Chicken Kabobsvmmatt23Belum ada peringkat

- Capital Budget TemplateDokumen1 halamanCapital Budget TemplaterajvakBelum ada peringkat

- Rules For Dads Raising Daughters The Good Men Project's ListDokumen3 halamanRules For Dads Raising Daughters The Good Men Project's Listvmmatt23Belum ada peringkat

- What Body Language Says About DoctorsDokumen3 halamanWhat Body Language Says About Doctorsvmmatt23Belum ada peringkat

- Understanding Crypto Fundamentals Value Investing in Cryptoassets and Management of Underlying Risks 1St Edition Thomas Jeegers All ChapterDokumen68 halamanUnderstanding Crypto Fundamentals Value Investing in Cryptoassets and Management of Underlying Risks 1St Edition Thomas Jeegers All Chapteramy.logan318100% (7)

- In Gold We Trust 2015Dokumen140 halamanIn Gold We Trust 2015Gold Silver Worlds100% (1)

- Chinas Exchange Rate PolicyDokumen16 halamanChinas Exchange Rate PolicybuphosooBelum ada peringkat

- TheComingChinaCrisis 10-06-2011Dokumen102 halamanTheComingChinaCrisis 10-06-2011Simon LouieBelum ada peringkat

- EISENBACH Financial Stability PoliciesDokumen40 halamanEISENBACH Financial Stability PoliciesAlex ZhongBelum ada peringkat

- Financial CrisisDokumen36 halamanFinancial CrisisSamit ChowdhuryBelum ada peringkat

- Wisdom & Whims of The CollectiveDokumen8 halamanWisdom & Whims of The CollectiveTraderCat SolarisBelum ada peringkat

- The Conduct of Monetary Policy: Strategy and TacticsDokumen34 halamanThe Conduct of Monetary Policy: Strategy and TacticsAlejandroArnoldoFritzRuenesBelum ada peringkat

- Report Title: Starbucks Marketing Plans Name: - ID: - Submitted To: - Submitted DateDokumen18 halamanReport Title: Starbucks Marketing Plans Name: - ID: - Submitted To: - Submitted Datemaham azizBelum ada peringkat

- Behavioural Finance Advantages and DisadvantagesDokumen2 halamanBehavioural Finance Advantages and DisadvantagesKartika Bhuvaneswaran NairBelum ada peringkat

- The Signal and The NoiseDokumen2 halamanThe Signal and The NoiseVasanth RajaBelum ada peringkat

- Financial CrisesDokumen24 halamanFinancial CrisesMaria Shaffaq50% (2)

- The Political Economy of Monetary Circuits Tradition and Change in Post-Keynesian Economics (Jean-François Ponsot, Sergio Rossi (Eds.) ) (Z-Library)Dokumen257 halamanThe Political Economy of Monetary Circuits Tradition and Change in Post-Keynesian Economics (Jean-François Ponsot, Sergio Rossi (Eds.) ) (Z-Library)Fachri RanuBelum ada peringkat

- STUDENT PROJECT ResearchDokumen19 halamanSTUDENT PROJECT ResearchkirtikaBelum ada peringkat

- What I Learned This Week: Bernard Baruch Elbert HubbardDokumen46 halamanWhat I Learned This Week: Bernard Baruch Elbert HubbardMWBelum ada peringkat

- River North Editions Fall 2013 CatalogDokumen108 halamanRiver North Editions Fall 2013 CatalogIndependent Publishers GroupBelum ada peringkat

- Barber & Odean - The Internet and The InvestorDokumen14 halamanBarber & Odean - The Internet and The Investoronat85Belum ada peringkat

- Impact of Global Financial Crisis (2007-2008) : ON The Indian EconomyDokumen48 halamanImpact of Global Financial Crisis (2007-2008) : ON The Indian EconomyDiksha PrajapatiBelum ada peringkat

- Term Paper On: Stock Market Crisis in BangladeshDokumen24 halamanTerm Paper On: Stock Market Crisis in BangladeshPushpa BaruaBelum ada peringkat

- Tullett Prebon Project Armagedon Aug 2011Dokumen34 halamanTullett Prebon Project Armagedon Aug 2011SwamiBelum ada peringkat

- Behaviour Finance AssignmentDokumen4 halamanBehaviour Finance Assignmentparakh malhotraBelum ada peringkat

- The Effect of The Global Financial Meltdown On The Nigerian EconomyDokumen13 halamanThe Effect of The Global Financial Meltdown On The Nigerian EconomyMorrison Omokiniovo Jessa SnrBelum ada peringkat

- Li Lu ArticlesDokumen10 halamanLi Lu Articlesmaxprogram100% (3)

- Clarium Save Now Invest LaterDokumen22 halamanClarium Save Now Invest Latermarketfolly.comBelum ada peringkat

- Global DebtDokumen36 halamanGlobal DebtAri Pingaley100% (1)

- The Siren Song of Factor TimingDokumen9 halamanThe Siren Song of Factor TimingHao OuYangBelum ada peringkat

- MODULE 5 Specialized Crime Investigation 2Dokumen5 halamanMODULE 5 Specialized Crime Investigation 2Kay KUaBelum ada peringkat