Anda mungkin juga menyukai

- Fifth Circuit Decision Against FDA in Apter CaseDokumen24 halamanFifth Circuit Decision Against FDA in Apter CaseAssociation of American Physicians and Surgeons100% (1)

- SPX Now and ThenDokumen1 halamanSPX Now and ThenCreditTraderBelum ada peringkat

- Weaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSDokumen37 halamanWeaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSJim Hoft100% (2)

- USD TLGP MaturitiesDokumen1 halamanUSD TLGP MaturitiesCreditTraderBelum ada peringkat

- Reynolds Public Health Proclamation - 2020.04.06Dokumen5 halamanReynolds Public Health Proclamation - 2020.04.06Shane Vander HartBelum ada peringkat

- IG-HY Vs Stocks Relative-ValueDokumen1 halamanIG-HY Vs Stocks Relative-ValueCreditTraderBelum ada peringkat

- HY Vs IG DurationDokumen1 halamanHY Vs IG DurationCreditTraderBelum ada peringkat

- SPL 20101019Dokumen1 halamanSPL 20101019CreditTraderBelum ada peringkat

- Credit ContractionDokumen1 halamanCredit ContractionCreditTraderBelum ada peringkat

- IG Fundamentals Q22010Dokumen1 halamanIG Fundamentals Q22010CreditTraderBelum ada peringkat

- IG Range CompressionDokumen1 halamanIG Range CompressionCreditTraderBelum ada peringkat

- CDR Csa Scatter Aug10Dokumen1 halamanCDR Csa Scatter Aug10CreditTraderBelum ada peringkat

- HY-IG Vs StocksDokumen1 halamanHY-IG Vs StocksCreditTraderBelum ada peringkat

- EUR Vs GDP-Weighted CDSDokumen1 halamanEUR Vs GDP-Weighted CDSCreditTraderBelum ada peringkat

- CDR Csa Aug2010Dokumen1 halamanCDR Csa Aug2010CreditTraderBelum ada peringkat

- C&I Loans + ABCP - Aggregate CreditDokumen1 halamanC&I Loans + ABCP - Aggregate CreditCreditTraderBelum ada peringkat

- HY-IG Vs EquityDokumen1 halamanHY-IG Vs EquityCreditTraderBelum ada peringkat

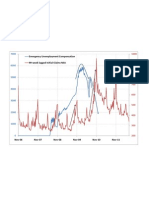

- EUC and 99-Week-Lagged Initial ClaimsDokumen1 halamanEUC and 99-Week-Lagged Initial ClaimsCreditTraderBelum ada peringkat

- CDR Csa 20100813Dokumen1 halamanCDR Csa 20100813CreditTraderBelum ada peringkat

- FSB30 IntrinsicsDokumen1 halamanFSB30 IntrinsicsCreditTraderBelum ada peringkat

- IG Over TSYDokumen1 halamanIG Over TSYCreditTraderBelum ada peringkat

- IG Weekly RangeDokumen1 halamanIG Weekly RangeCreditTraderBelum ada peringkat

- CDR Csa 20100716Dokumen1 halamanCDR Csa 20100716CreditTraderBelum ada peringkat

- CDR Csa 201007Dokumen1 halamanCDR Csa 201007CreditTraderBelum ada peringkat

- Implied CorrelationDokumen1 halamanImplied CorrelationCreditTraderBelum ada peringkat

- IG Vs TSY CycleDokumen1 halamanIG Vs TSY CycleCreditTraderBelum ada peringkat

- Exchange Rate Regime Analysis For The Chinese YuanDokumen10 halamanExchange Rate Regime Analysis For The Chinese YuanCreditTraderBelum ada peringkat

- Spread Leverage ComparisonDokumen1 halamanSpread Leverage ComparisonCreditTraderBelum ada peringkat

- JUN Roll by SectorDokumen1 halamanJUN Roll by SectorCreditTraderBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Dell & Ricoh Introduction LetterDokumen49 halamanDell & Ricoh Introduction LetterAli SharifiBelum ada peringkat

- Liebherr l544 - L 574 Service ManualDokumen658 halamanLiebherr l544 - L 574 Service ManualVerona Mamaia100% (15)

- The Indian Partnership Act, 1932Dokumen17 halamanThe Indian Partnership Act, 1932Engineer100% (1)

- TOEFL IdiomsDokumen63 halamanTOEFL IdiomsMario Matus González100% (1)

- Complaint HULRBDokumen4 halamanComplaint HULRBPatrio Jr SeñeresBelum ada peringkat

- Board Resolution - Dissolving Corporation RRGDokumen2 halamanBoard Resolution - Dissolving Corporation RRGJhun Merino100% (10)

- HDFC Securities Limited: Client Equity Derivative Ledger For The Period 01-APR-19 TO 30-JUN-19Dokumen2 halamanHDFC Securities Limited: Client Equity Derivative Ledger For The Period 01-APR-19 TO 30-JUN-19Num NutzBelum ada peringkat

- Annual Report PT Gunawan Dianjaya Steel TBK 2015Dokumen118 halamanAnnual Report PT Gunawan Dianjaya Steel TBK 2015Ratna Dwi KurniaBelum ada peringkat

- Ge Elect 2 - Entrepreneurial MindDokumen34 halamanGe Elect 2 - Entrepreneurial MindElisa PlanzarBelum ada peringkat

- Seginus Inc Is Proud To Release New Inventory Item: Housing Assembly Scroll 2805489-4EHDokumen2 halamanSeginus Inc Is Proud To Release New Inventory Item: Housing Assembly Scroll 2805489-4EHPR.comBelum ada peringkat

- Eurocity Corporate Structure 2Dokumen6 halamanEurocity Corporate Structure 2simon1608Belum ada peringkat

- Proposed Titles For Redevelopment Projects: Urban Node: An Integrated Tourist Market CenterDokumen6 halamanProposed Titles For Redevelopment Projects: Urban Node: An Integrated Tourist Market CenterErika RafaelBelum ada peringkat

- 2.) National Sugar Trading V PNB - CastroDokumen2 halaman2.) National Sugar Trading V PNB - CastroMalcolm Cruz100% (1)

- TelDokumen4 halamanTelabdulBelum ada peringkat

- Danaher Corporation: 2017 OverviewDokumen30 halamanDanaher Corporation: 2017 OverviewMichael Cano Lombardo100% (1)

- BS 2009-10Dokumen109 halamanBS 2009-10narendra kumarBelum ada peringkat

- LAW AMLA PresentationDokumen28 halamanLAW AMLA PresentationThilagavathy PalaniappanBelum ada peringkat

- Does The Recognition of Football Players...Dokumen40 halamanDoes The Recognition of Football Players...Juan Ruiz-UrquijoBelum ada peringkat

- Navieras ExtranjerasDokumen16 halamanNavieras ExtranjerasClaudia GarciaBelum ada peringkat

- PT - Payroll OutsourcingDokumen9 halamanPT - Payroll OutsourcingMujtaba MerchantBelum ada peringkat

- Approved List of Employers 5 10 17 NEW 1Dokumen52 halamanApproved List of Employers 5 10 17 NEW 1Mithun Nair MBelum ada peringkat

- RC Property Transfers 10-18to11-7watermarkDokumen9 halamanRC Property Transfers 10-18to11-7watermarkElizabeth WrightBelum ada peringkat

- Csss 2008Dokumen240 halamanCsss 2008rfvz6sBelum ada peringkat

- Combination Notes For LLMDokumen52 halamanCombination Notes For LLMshashwat dangiBelum ada peringkat

- Principal Agent ProblemDokumen3 halamanPrincipal Agent ProblemMalik Wasim Abbas100% (1)

- Glomac Berhad (GLOMAC) - Company Profile and SWOT Analysis PDFDokumen38 halamanGlomac Berhad (GLOMAC) - Company Profile and SWOT Analysis PDFMuhammad Zaki0% (1)

- Proposed Policy & Guidelines For Cash Advance Requisition LiquidationDokumen3 halamanProposed Policy & Guidelines For Cash Advance Requisition LiquidationEmmanuelCuaresma100% (1)

- Tata Corus PPT Group 5Dokumen37 halamanTata Corus PPT Group 5Abhay Thakur100% (1)

- An Analysis of The Indian Outbound Travel MarketDokumen18 halamanAn Analysis of The Indian Outbound Travel MarketLieven Der KinderenBelum ada peringkat

- 0chapter 1-Strategic ManagementDokumen19 halaman0chapter 1-Strategic ManagementAlyannaBelum ada peringkat