Anda mungkin juga menyukai

- BQ FinalDokumen188 halamanBQ FinalNicholas DavisBelum ada peringkat

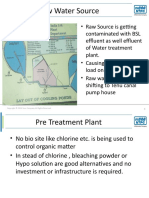

- Click To Edit Master Title Style: Raw Water SourceDokumen7 halamanClick To Edit Master Title Style: Raw Water SourceNicholas DavisBelum ada peringkat

- of Electrical Audit 2Dokumen43 halamanof Electrical Audit 2Nicholas DavisBelum ada peringkat

- Closing PresentationDokumen12 halamanClosing PresentationNicholas DavisBelum ada peringkat

- PP Audit Rep 2018 BPSCLDokumen13 halamanPP Audit Rep 2018 BPSCLNicholas DavisBelum ada peringkat

- of Electrical AuditDokumen18 halamanof Electrical AuditNicholas DavisBelum ada peringkat

- Rajesh Kumar Future of Coal Based Generation Jan2018Dokumen23 halamanRajesh Kumar Future of Coal Based Generation Jan2018Nicholas DavisBelum ada peringkat

- Click To Edit Master Title Style: Raw Water SourceDokumen7 halamanClick To Edit Master Title Style: Raw Water SourceNicholas DavisBelum ada peringkat

- EI PresentationDokumen11 halamanEI PresentationNicholas DavisBelum ada peringkat

- A Midsummer Night's Dream: Enter THESEUS, HIPPOLYTA, PHILOSTRATE, and AttendantsDokumen54 halamanA Midsummer Night's Dream: Enter THESEUS, HIPPOLYTA, PHILOSTRATE, and AttendantsNicholas DavisBelum ada peringkat

- Click To Edit Master Title Style: Raw Water SourceDokumen7 halamanClick To Edit Master Title Style: Raw Water SourceNicholas DavisBelum ada peringkat

- Sri Hanuman Chalisa in HindiDokumen3 halamanSri Hanuman Chalisa in HindiSrivatsa97% (31)

- Hdfcbank Credit Card Rewards CatalogueDokumen69 halamanHdfcbank Credit Card Rewards Cataloguemith143Belum ada peringkat

- Fire Insuranc E.: Done By: Sudeepta SabatDokumen10 halamanFire Insuranc E.: Done By: Sudeepta SabatNicholas DavisBelum ada peringkat

- RSC Oil Sands Panel Main Report Oct 2012Dokumen440 halamanRSC Oil Sands Panel Main Report Oct 2012Nicholas DavisBelum ada peringkat

- Paradise Lost PDFDokumen374 halamanParadise Lost PDFNicholas DavisBelum ada peringkat

- 1 - Introduction To DerivativesDokumen34 halaman1 - Introduction To DerivativesNicholas Davis100% (4)

- Tech MahindraDokumen5 halamanTech MahindraNicholas DavisBelum ada peringkat

- PDCA VisitDokumen34 halamanPDCA VisitNicholas DavisBelum ada peringkat

- Solutions For Conventional Power Generation: Enhanced Performance, Efficiency and ReliabilityDokumen12 halamanSolutions For Conventional Power Generation: Enhanced Performance, Efficiency and ReliabilityNicholas DavisBelum ada peringkat

- Bank Finanace ITDokumen348 halamanBank Finanace ITNicholas DavisBelum ada peringkat

- Bank Finanace ITDokumen348 halamanBank Finanace ITNicholas DavisBelum ada peringkat

- 24 - ILO HistoryDokumen5 halaman24 - ILO HistoryNicholas DavisBelum ada peringkat

- Modernisation of Meat and Fish ShopsDokumen1 halamanModernisation of Meat and Fish ShopsNicholas DavisBelum ada peringkat

- Class Schedule of PGEXP 2014-16 Term VIDokumen4 halamanClass Schedule of PGEXP 2014-16 Term VINicholas DavisBelum ada peringkat

- Sample Green Belt Examination QuestionsDokumen26 halamanSample Green Belt Examination QuestionsRengarajan ThiruvengadaswamyBelum ada peringkat

- Nike, IncDokumen19 halamanNike, IncRavi PrakashBelum ada peringkat

- Presentation Chairman BPSCL Feb 16 Final NolinksDokumen58 halamanPresentation Chairman BPSCL Feb 16 Final NolinksNicholas DavisBelum ada peringkat

- Course Outline Project Management 2016 Rajiv MisraDokumen4 halamanCourse Outline Project Management 2016 Rajiv MisraNicholas DavisBelum ada peringkat

- Six Sigma ExamDokumen5 halamanSix Sigma Exammajid4uonly100% (5)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- ForEx Hidden SystemsDokumen123 halamanForEx Hidden SystemsWar Prince100% (2)

- Forklift Driving Training MalaysiaDokumen2 halamanForklift Driving Training MalaysiaIsogroupBelum ada peringkat

- Leizel C. AmidoDokumen2 halamanLeizel C. AmidoAmido Capagngan LeizelBelum ada peringkat

- GDP For 1st QuarterDokumen5 halamanGDP For 1st QuarterUmesh MatkarBelum ada peringkat

- 33611B SUV & Light Truck Manufacturing in The US Industry ReportDokumen38 halaman33611B SUV & Light Truck Manufacturing in The US Industry ReportSubhash BabuBelum ada peringkat

- The Great South African Land ScandalDokumen158 halamanThe Great South African Land ScandalTinyiko S. MalulekeBelum ada peringkat

- Trump and Globalization - 0Dokumen14 halamanTrump and Globalization - 0Alexei PalamaruBelum ada peringkat

- Capsim Success MeasuresDokumen10 halamanCapsim Success MeasuresalyrBelum ada peringkat

- China-The Land That Failed To Fail PDFDokumen81 halamanChina-The Land That Failed To Fail PDFeric_stBelum ada peringkat

- Global Strategic Planning: ObjectivesDokumen4 halamanGlobal Strategic Planning: ObjectivesHitesh GevariyaBelum ada peringkat

- Capital Weekly 018 OnlineDokumen20 halamanCapital Weekly 018 OnlineBelize ConsulateBelum ada peringkat

- Plan Contable EmpresarialDokumen432 halamanPlan Contable EmpresarialJhamil Nirek PascasioBelum ada peringkat

- The Currency Correlation Secret - TwoDokumen10 halamanThe Currency Correlation Secret - Twofebrichow100% (1)

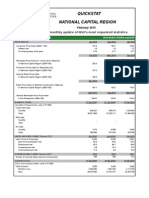

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDokumen3 halamanQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiBelum ada peringkat

- Model Sale AgreementDokumen4 halamanModel Sale AgreementNagaraj KumbleBelum ada peringkat

- Brochure (Eng) - 2021 Oda KoreaDokumen9 halamanBrochure (Eng) - 2021 Oda Koreasunjung kimBelum ada peringkat

- Import - Export Tariff of Local Charges at HCM For FCL & LCL & Air (Free-Hand) - FinalDokumen2 halamanImport - Export Tariff of Local Charges at HCM For FCL & LCL & Air (Free-Hand) - FinalNguyễn Thanh LongBelum ada peringkat

- RSAW Review of The Year 2021Dokumen14 halamanRSAW Review of The Year 2021Prasamsa PBelum ada peringkat

- Law University SynopsisDokumen3 halamanLaw University Synopsistinabhuvan50% (2)

- KFC Offer T&C: SL - No Outlet Name CityDokumen16 halamanKFC Offer T&C: SL - No Outlet Name Cityanita rajenBelum ada peringkat

- A Complaint Is A GiftDokumen8 halamanA Complaint Is A GiftSRIDHAR SUBRAMANIAMBelum ada peringkat

- WSE-LWDFS.20-08.Andik Syaifudin Zuhri-ProposalDokumen12 halamanWSE-LWDFS.20-08.Andik Syaifudin Zuhri-ProposalandikszuhriBelum ada peringkat

- Nothing AdaptorDokumen1 halamanNothing AdaptorOmbabu SharmaBelum ada peringkat

- 2023 Nigerian Capital Market UpdateDokumen13 halaman2023 Nigerian Capital Market Updatemay izinyonBelum ada peringkat

- Dummy VariableDokumen21 halamanDummy VariableMuhammad MudassirBelum ada peringkat

- Balancing Natural Gas Policy Vol-1 Summary (NPC, 2003)Dokumen118 halamanBalancing Natural Gas Policy Vol-1 Summary (NPC, 2003)Nak-Gyun KimBelum ada peringkat

- Hni 72Dokumen1 halamanHni 72Arsh AhmadBelum ada peringkat

- To Sell or Scale Up: Canada's Patent Strategy in A Knowledge EconomyDokumen22 halamanTo Sell or Scale Up: Canada's Patent Strategy in A Knowledge EconomyInstitute for Research on Public Policy (IRPP)Belum ada peringkat

- Acctg 1 PS 1Dokumen3 halamanAcctg 1 PS 1Aj GuanzonBelum ada peringkat

- Invoice: House No 211-R, Sector 15-B, Afer Zon North Nazima Bad Town, KarachiDokumen3 halamanInvoice: House No 211-R, Sector 15-B, Afer Zon North Nazima Bad Town, KarachijeogilaniBelum ada peringkat