Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Ducting Insulation ScheduleDokumen1 halamanDucting Insulation ScheduleMohammed AliBelum ada peringkat

- Comparative Analysis of The Dispute Resolution MechanismsDokumen22 halamanComparative Analysis of The Dispute Resolution MechanismsMohammed AliBelum ada peringkat

- Biggest NovelDokumen1 halamanBiggest NovelMohammed AliBelum ada peringkat

- Gas Generators GraphDokumen1 halamanGas Generators GraphMohammed AliBelum ada peringkat

- WhatsAppDokumen1 halamanWhatsAppMohammed AliBelum ada peringkat

- APC Guide - Q&ADokumen188 halamanAPC Guide - Q&AMohamed Ismath Kalideen100% (1)

- CBSE Link 10 Papers PDFDokumen3 halamanCBSE Link 10 Papers PDFMohammed AliBelum ada peringkat

- UntitledDokumen1 halamanUntitledMohammed AliBelum ada peringkat

- Evolution of Medieval Thought Second Edition The David KnowlesDokumen3 halamanEvolution of Medieval Thought Second Edition The David KnowlesMohammed AliBelum ada peringkat

- Probable APC QuestionsDokumen4 halamanProbable APC Questionsakg2004167% (3)

- Challenging The Adjudicators DecisionDokumen5 halamanChallenging The Adjudicators DecisionMohammed AliBelum ada peringkat

- Dubai Legal and Regulatory System PDFDokumen9 halamanDubai Legal and Regulatory System PDFAlex HalliwellBelum ada peringkat

- Banishing Shall From Business Contracts ACLADokumen2 halamanBanishing Shall From Business Contracts ACLAMohammed AliBelum ada peringkat

- Evolution of Medieval Thought Second Edition The David Knowles PDFDokumen366 halamanEvolution of Medieval Thought Second Edition The David Knowles PDFMohammed Ali100% (2)

- Rating of Power Cables - George Anders PDFDokumen513 halamanRating of Power Cables - George Anders PDFMohammed Ali100% (1)

- What Is PH120Dokumen1 halamanWhat Is PH120Mohammed AliBelum ada peringkat

- Contract InterpretationDokumen3 halamanContract InterpretationMohammed AliBelum ada peringkat

- Coal and Petroleum: Activity 3.1 I DoDokumen32 halamanCoal and Petroleum: Activity 3.1 I DoEswaranBelum ada peringkat

- An Outlook of APC PDFDokumen3 halamanAn Outlook of APC PDFMohammed AliBelum ada peringkat

- Type of Gland: Cable GlandsDokumen7 halamanType of Gland: Cable GlandsNavneet SinghBelum ada peringkat

- Fuel - Consumption - Chart - Standard Diesel EngineDokumen1 halamanFuel - Consumption - Chart - Standard Diesel EngineCaptIsqanBelum ada peringkat

- Shopping & RetailDokumen246 halamanShopping & RetailMohammed AliBelum ada peringkat

- Surace FinishesDokumen50 halamanSurace FinishesMohammed AliBelum ada peringkat

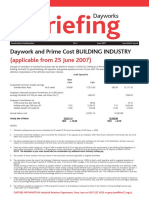

- Day WorksDokumen1 halamanDay WorksMohammed AliBelum ada peringkat

- S Aa Aux Bat&Ch Lead 48 S (Rev.0 2007)Dokumen16 halamanS Aa Aux Bat&Ch Lead 48 S (Rev.0 2007)Mohammed AliBelum ada peringkat

- Extension of Time Claim ProcedureDokumen108 halamanExtension of Time Claim ProcedureAshish Kumar GuptaBelum ada peringkat

- Transformer Installation RulesDokumen5 halamanTransformer Installation RulesMohammed AliBelum ada peringkat

- KAHRAMAA RegulationsDokumen140 halamanKAHRAMAA RegulationsMohammed AliBelum ada peringkat

- Tech AbbreviationsDokumen11 halamanTech AbbreviationsMohammed AliBelum ada peringkat

- Power QualityDokumen130 halamanPower QualityMohammed AliBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Mini Project A-9-1Dokumen12 halamanMini Project A-9-1santhoshrao19Belum ada peringkat

- Necromunda CatalogDokumen35 halamanNecromunda Catalogzafnequin8494100% (1)

- Company Registration Procedure Handbook in Cambodia, EnglishDokumen124 halamanCompany Registration Procedure Handbook in Cambodia, EnglishThea100% (16)

- Retailing PPT (Shailwi Nitish)Dokumen14 halamanRetailing PPT (Shailwi Nitish)vinit PatidarBelum ada peringkat

- Motion To Dismiss Guidry Trademark Infringement ClaimDokumen23 halamanMotion To Dismiss Guidry Trademark Infringement ClaimDaniel BallardBelum ada peringkat

- Small Data, Big Decisions: Model Selection in The Small-Data RegimeDokumen10 halamanSmall Data, Big Decisions: Model Selection in The Small-Data Regimejuan carlos monasterio saezBelum ada peringkat

- Early Christian ArchitectureDokumen38 halamanEarly Christian ArchitectureInspirations & ArchitectureBelum ada peringkat

- Serenity RPG Firefly Role Playing Game PDFDokumen225 halamanSerenity RPG Firefly Role Playing Game PDFNathaniel Broyles67% (3)

- Load Schedule: DescriptionDokumen1 halamanLoad Schedule: Descriptionkurt james alorroBelum ada peringkat

- 2022 NEDA Annual Report Pre PubDokumen68 halaman2022 NEDA Annual Report Pre PubfrancessantiagoBelum ada peringkat

- Combining Wavelet and Kalman Filters For Financial Time Series PredictionDokumen17 halamanCombining Wavelet and Kalman Filters For Financial Time Series PredictionLuis OliveiraBelum ada peringkat

- NOV23 Nomura Class 6Dokumen54 halamanNOV23 Nomura Class 6JAYA BHARATHA REDDYBelum ada peringkat

- S P99 41000099DisplayVendorListDokumen31 halamanS P99 41000099DisplayVendorListMazen Sanad100% (1)

- PRINCIPLES OF TEACHING NotesDokumen24 halamanPRINCIPLES OF TEACHING NotesHOLLY MARIE PALANGAN100% (2)

- Aashirwaad Notes For CA IPCC Auditing & Assurance by Neeraj AroraDokumen291 halamanAashirwaad Notes For CA IPCC Auditing & Assurance by Neeraj AroraMohammed NasserBelum ada peringkat

- Mahindra First Choice Wheels LTD: 4-Wheeler Inspection ReportDokumen5 halamanMahindra First Choice Wheels LTD: 4-Wheeler Inspection ReportRavi LoveBelum ada peringkat

- Windows Insider ProgramDokumen10 halamanWindows Insider ProgramVasileBurcuBelum ada peringkat

- Matrices and Vectors. - . in A Nutshell: AT Patera, M Yano October 9, 2014Dokumen19 halamanMatrices and Vectors. - . in A Nutshell: AT Patera, M Yano October 9, 2014navigareeBelum ada peringkat

- The Impact of Personnel Behaviour in Clean RoomDokumen59 halamanThe Impact of Personnel Behaviour in Clean Roomisrael afolayan mayomiBelum ada peringkat

- Voice Over Script For Pilot TestingDokumen2 halamanVoice Over Script For Pilot TestingRichelle Anne Tecson ApitanBelum ada peringkat

- Operator'S Manual PM20X-X-X-BXX: 2" Diaphragm PumpDokumen12 halamanOperator'S Manual PM20X-X-X-BXX: 2" Diaphragm PumpOmar TadeoBelum ada peringkat

- Paper 4 Material Management Question BankDokumen3 halamanPaper 4 Material Management Question BankDr. Rakshit Solanki100% (2)

- Vtoris 100% Clean Paypal Transfer Guide 2015Dokumen8 halamanVtoris 100% Clean Paypal Transfer Guide 2015Sean FrohmanBelum ada peringkat

- ISSA2013Ed CabinStores v100 Часть10Dokumen2 halamanISSA2013Ed CabinStores v100 Часть10AlexanderBelum ada peringkat

- Training Course For 2 Class Boiler Proficiency Certificate (Gujarat Ibr)Dokumen3 halamanTraining Course For 2 Class Boiler Proficiency Certificate (Gujarat Ibr)JAY PARIKHBelum ada peringkat

- Dash8 200 300 Electrical PDFDokumen35 halamanDash8 200 300 Electrical PDFCarina Ramo LakaBelum ada peringkat

- PixiiDokumen3 halamanPixiiFoxBelum ada peringkat

- Family Factors: Its Effect On The Academic Performance of The Grade 6 Pupils of East Bayugan Central Elementary SchoolDokumen11 halamanFamily Factors: Its Effect On The Academic Performance of The Grade 6 Pupils of East Bayugan Central Elementary SchoolGrace Joy AsorBelum ada peringkat

- How Muslim Inventors Changed The WorldDokumen4 halamanHow Muslim Inventors Changed The WorldShadab AnjumBelum ada peringkat

- List of Bird Sanctuaries in India (State-Wise)Dokumen6 halamanList of Bird Sanctuaries in India (State-Wise)VISHRUTH.S. GOWDABelum ada peringkat