Anda mungkin juga menyukai

- 50% Allowance ClarificationDokumen2 halaman50% Allowance ClarificationHumayoun Ahmad FarooqiBelum ada peringkat

- Pension Increases Table PunjabDokumen2 halamanPension Increases Table PunjabHumayoun Ahmad Farooqi78% (18)

- Pay Fixation PunjabDokumen79 halamanPay Fixation PunjabHumayoun Ahmad Farooqi100% (2)

- AffidavitDokumen2 halamanAffidavitHumayoun Ahmad FarooqiBelum ada peringkat

- Regularization of Contract Employees Grade 1-15 Punjab GovtDokumen3 halamanRegularization of Contract Employees Grade 1-15 Punjab GovtHumayoun Ahmad Farooqi100% (5)

- Punjab Delegation of Financial Rules Updated 2012Dokumen394 halamanPunjab Delegation of Financial Rules Updated 2012Humayoun Ahmad FarooqiBelum ada peringkat

- Final Seniority List of DDAO/DTO/DOADokumen6 halamanFinal Seniority List of DDAO/DTO/DOAHumayoun Ahmad FarooqiBelum ada peringkat

- Islami Mahino Ke Fazail o Ahkaam Molana RoohullahDokumen236 halamanIslami Mahino Ke Fazail o Ahkaam Molana RoohullahKamrans_Maktaba_Urdu0% (2)

- Electronic Crimes Act 2004Dokumen12 halamanElectronic Crimes Act 2004Humayoun Ahmad FarooqiBelum ada peringkat

- List of Sahaba R.A - UpdatedDokumen92 halamanList of Sahaba R.A - UpdatedShadab Shaikh69% (13)

- Bermuda Tikon Aur Dajjal by Sheikh Umar AsimDokumen277 halamanBermuda Tikon Aur Dajjal by Sheikh Umar AsimMusalman Bhai100% (1)

- DAJJAL Kaun Kaab Kaaha by Mufti Abu Lubaba Shah MansoorDokumen250 halamanDAJJAL Kaun Kaab Kaaha by Mufti Abu Lubaba Shah MansoorHumayoun Ahmad Farooqi100% (3)

- Tanbeeh Ul-Ghafileen by Shaykh Abu Laith Samarqandi R.A Urdu TranslationDokumen328 halamanTanbeeh Ul-Ghafileen by Shaykh Abu Laith Samarqandi R.A Urdu TranslationTalib Ghaffari86% (7)

- Aqeeda Zahoor e Mehdi Ahadith Ki Roshni MayDokumen191 halamanAqeeda Zahoor e Mehdi Ahadith Ki Roshni MayISLAMIC LIBRARYBelum ada peringkat

- Bachon Ke Liay Ibtidai Deeni Taleemaat by Sheikh Mufti Ehsanullah ShaiqDokumen59 halamanBachon Ke Liay Ibtidai Deeni Taleemaat by Sheikh Mufti Ehsanullah ShaiqMusalman BhaiBelum ada peringkat

- Intergovernmental TransfersDokumen31 halamanIntergovernmental TransfersHumayoun Ahmad FarooqiBelum ada peringkat

- Constitution of Pakistan 1973 in Urdu VerDokumen256 halamanConstitution of Pakistan 1973 in Urdu Vermuradlaghari82% (159)

- Building and Road B&R Code, DFRDokumen286 halamanBuilding and Road B&R Code, DFRHumayoun Ahmad Farooqi100% (1)

- District Budget RulesDokumen98 halamanDistrict Budget RulesHumayoun Ahmad FarooqiBelum ada peringkat

- The Punjab Urban Immovable Property Tax ActDokumen12 halamanThe Punjab Urban Immovable Property Tax ActHumayoun Ahmad FarooqiBelum ada peringkat

- Punjab Medical Attendance RulesDokumen55 halamanPunjab Medical Attendance RulesHumayoun Ahmad Farooqi78% (9)

- Final Manual of DaosDokumen265 halamanFinal Manual of DaosHumayoun Ahmad Farooqi100% (1)

- ETODokumen25 halamanETOAltaf SheikhBelum ada peringkat

- The Punjab Court FeesDokumen1 halamanThe Punjab Court FeesHumayoun Ahmad FarooqiBelum ada peringkat

- The Punjab Agricultural Income Tax Act 1997Dokumen11 halamanThe Punjab Agricultural Income Tax Act 1997Humayoun Ahmad FarooqiBelum ada peringkat

- The Punjab Land Revenue ActDokumen65 halamanThe Punjab Land Revenue ActHumayoun Ahmad FarooqiBelum ada peringkat

- The Punjab Motor Vehicles Taxation ActDokumen10 halamanThe Punjab Motor Vehicles Taxation ActHumayoun Ahmad FarooqiBelum ada peringkat

- The Punjab Government Servants Housing Foundation Act 2004Dokumen6 halamanThe Punjab Government Servants Housing Foundation Act 2004Humayoun Ahmad FarooqiBelum ada peringkat

- PEEDA ActDokumen11 halamanPEEDA ActFurzan AbbasBelum ada peringkat

- The On-Farm Water ManagementDokumen7 halamanThe On-Farm Water ManagementHumayoun Ahmad FarooqiBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Stirling Bio Power GeneratorDokumen5 halamanStirling Bio Power GeneratorAvram Stefan100% (2)

- PSI 8.8L ServiceDokumen197 halamanPSI 8.8L Serviceedelmolina100% (1)

- Area & Perimeter - CRACK SSC PDFDokumen10 halamanArea & Perimeter - CRACK SSC PDFSai Swaroop AttadaBelum ada peringkat

- Application For New Ration Card - Telangana & AP StatesDokumen1 halamanApplication For New Ration Card - Telangana & AP Statesping2gopiBelum ada peringkat

- PPR 8001Dokumen1 halamanPPR 8001quangga10091986Belum ada peringkat

- Chapter 2: Static Routing: Instructor MaterialsDokumen63 halamanChapter 2: Static Routing: Instructor MaterialsAhmad Mustafa AbimayuBelum ada peringkat

- Magnetic Properties of MaterialsDokumen10 halamanMagnetic Properties of MaterialsNoviBelum ada peringkat

- c15 ldn01610 SchematicDokumen4 halamanc15 ldn01610 SchematicJacques Van Niekerk50% (2)

- Presentation On Plant LayoutDokumen20 halamanPresentation On Plant LayoutSahil NayyarBelum ada peringkat

- Openness and The Market Friendly ApproachDokumen27 halamanOpenness and The Market Friendly Approachmirzatouseefahmed100% (2)

- PCB Design PCB Design: Dr. P. C. PandeyDokumen13 halamanPCB Design PCB Design: Dr. P. C. PandeyengshimaaBelum ada peringkat

- ClientDokumen51 halamanClientCarla Nilana Lopes XavierBelum ada peringkat

- TUV300 T4 Plus Vs TUV300 T6 Plus Vs TUV300 T8 Vs TUV300 T10 - CarWaleDokumen12 halamanTUV300 T4 Plus Vs TUV300 T6 Plus Vs TUV300 T8 Vs TUV300 T10 - CarWalernbansalBelum ada peringkat

- Coding Guidelines-CDokumen71 halamanCoding Guidelines-CKishoreRajuBelum ada peringkat

- MBFI Quiz KeyDokumen7 halamanMBFI Quiz Keypunitha_pBelum ada peringkat

- Internet Intranet ExtranetDokumen28 halamanInternet Intranet ExtranetAmeya Patil100% (1)

- Pocket Pod PresetsDokumen13 halamanPocket Pod PresetsmarcusolivusBelum ada peringkat

- Lululemon Style GuideDokumen15 halamanLululemon Style Guideapi-263257893Belum ada peringkat

- Anwar Hossain PDFDokumen4 halamanAnwar Hossain PDFnodaw92388Belum ada peringkat

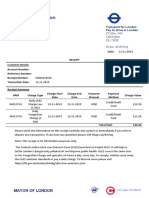

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDokumen1 halamanTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucBelum ada peringkat

- Hukbalahap: March 16, 2019 Godwin M. Rarama Readings in The Philippine History Seat No. 35Dokumen2 halamanHukbalahap: March 16, 2019 Godwin M. Rarama Readings in The Philippine History Seat No. 35Godwin RaramaBelum ada peringkat

- 5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFDokumen1 halaman5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFBobby B. BrownBelum ada peringkat

- Implementation of BS 8500 2006 Concrete Minimum Cover PDFDokumen13 halamanImplementation of BS 8500 2006 Concrete Minimum Cover PDFJimmy Lopez100% (1)

- TelekomDokumen2 halamanTelekomAnonymous eS7MLJvPZCBelum ada peringkat

- Lecun 20201027 AttDokumen72 halamanLecun 20201027 AttEfrain TitoBelum ada peringkat

- NMIMS Offer LetterDokumen4 halamanNMIMS Offer LetterSUBHAJITBelum ada peringkat

- EU MEA Market Outlook Report 2022Dokumen21 halamanEU MEA Market Outlook Report 2022ahmedBelum ada peringkat

- Unix Training ContentDokumen5 halamanUnix Training ContentsathishkumarBelum ada peringkat

- QP02Dokumen11 halamanQP02zakwanmustafa0% (1)

- New CVLRDokumen2 halamanNew CVLRanahata2014Belum ada peringkat