Anda mungkin juga menyukai

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionDari EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionBelum ada peringkat

- Financial AccountingDokumen455 halamanFinancial AccountingKalGeorgeBelum ada peringkat

- Payment Advice DetailsDokumen2 halamanPayment Advice DetailsVishal KambleBelum ada peringkat

- Clickworker Payment ConformationDokumen1 halamanClickworker Payment ConformationRekha RavaliBelum ada peringkat

- Zuku Payments Format PDFDokumen2 halamanZuku Payments Format PDFKalGeorgeBelum ada peringkat

- Zuku Payments Format PDFDokumen2 halamanZuku Payments Format PDFKalGeorgeBelum ada peringkat

- Kenya passport application formDokumen4 halamanKenya passport application formKalGeorgeBelum ada peringkat

- TRAIN LAW SUMMARYDokumen60 halamanTRAIN LAW SUMMARYLex Dagdag100% (3)

- Notes Chapter 3 REGDokumen7 halamanNotes Chapter 3 REGcpacfa90% (10)

- BRIÑEZDokumen2 halamanBRIÑEZMundo RealBelum ada peringkat

- Invoice JBL PDFDokumen1 halamanInvoice JBL PDFDhruv MishraBelum ada peringkat

- Concepts of Income and Income TaxationDokumen16 halamanConcepts of Income and Income TaxationaisahBelum ada peringkat

- Train I.ppt - Vers. 10.21.2018Dokumen103 halamanTrain I.ppt - Vers. 10.21.2018Ellard28 saturnoBelum ada peringkat

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDari Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsBelum ada peringkat

- Taxation LawDokumen10 halamanTaxation LawflorBelum ada peringkat

- Lesson 5 Part 2 TranscriptionDokumen10 halamanLesson 5 Part 2 TranscriptionErica Joy M. SalvaneraBelum ada peringkat

- 18 Tan V Del Rosario 237 SCRA 324 (1994) - DigestDokumen15 halaman18 Tan V Del Rosario 237 SCRA 324 (1994) - DigestKeith BalbinBelum ada peringkat

- Summer Internship Project Report ON "Itr E-Filing": Subject Code:KMBN308Dokumen60 halamanSummer Internship Project Report ON "Itr E-Filing": Subject Code:KMBN308Sumit Ranjan100% (6)

- 13.republic Vs RicarteDokumen1 halaman13.republic Vs RicarteGyelamagne EstradaBelum ada peringkat

- How Do You See It?: East Africa Quick Tax Guide 2012Dokumen11 halamanHow Do You See It?: East Africa Quick Tax Guide 2012Zimbo KigoBelum ada peringkat

- Deloitte Tax Pocket Guide 2014Dokumen20 halamanDeloitte Tax Pocket Guide 2014YHBelum ada peringkat

- India Highlights of Budget 2016 at A GlanceDokumen5 halamanIndia Highlights of Budget 2016 at A GlanceKARTHIK145Belum ada peringkat

- 10-Practical Questions of Individuals (78-113)Dokumen38 halaman10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- P6mys 2016 Jun QDokumen15 halamanP6mys 2016 Jun QAtiqah DalikBelum ada peringkat

- Tax Reckoner 2013-14: Snapshot of Tax Rates Specific To Mutual FundsDokumen2 halamanTax Reckoner 2013-14: Snapshot of Tax Rates Specific To Mutual FundsZia Ur RehmanBelum ada peringkat

- Finance Bill 2014Dokumen18 halamanFinance Bill 2014Tanvir Ahmed SyedBelum ada peringkat

- Budget Highlights 2013Dokumen12 halamanBudget Highlights 2013Souma MukherjeeBelum ada peringkat

- M4 - Income TaxationDokumen12 halamanM4 - Income TaxationGraceCayabyabNiduazaBelum ada peringkat

- Quick Tax Guide-2012Dokumen9 halamanQuick Tax Guide-2012Paul MaposaBelum ada peringkat

- Employment Income: Presented By: Kennedy OkiroDokumen21 halamanEmployment Income: Presented By: Kennedy OkiroLeah Wambui MachariaBelum ada peringkat

- Financial Budget 2013Dokumen9 halamanFinancial Budget 2013Mitesh PanchalBelum ada peringkat

- Tanzania Tax Guide 2016/2017Dokumen22 halamanTanzania Tax Guide 2016/2017Timothy Rogatus67% (3)

- Income Tax - Major Highlights of Union Budget - 2011-12: Prasad V Sawant Roll No:96 Tax AssignmentDokumen5 halamanIncome Tax - Major Highlights of Union Budget - 2011-12: Prasad V Sawant Roll No:96 Tax AssignmentJohn DoinBelum ada peringkat

- Type Rate of Tax: Value-Added Tax (VAT) Donations Tax Unemployment Insurance ContributionsDokumen2 halamanType Rate of Tax: Value-Added Tax (VAT) Donations Tax Unemployment Insurance Contributionsdiefenbaker13Belum ada peringkat

- Employment Vs HiringDokumen29 halamanEmployment Vs Hiringnaulele robertBelum ada peringkat

- 2010 - Easy - Guide For Foreigner's Year-End Tax SettlementDokumen94 halaman2010 - Easy - Guide For Foreigner's Year-End Tax Settlement안수현Belum ada peringkat

- Tax Rates For MFs And Investors 2012-13Dokumen2 halamanTax Rates For MFs And Investors 2012-13mayankleo_1Belum ada peringkat

- Deloitte - A Pocket Guide To Singapore Tax 2014 PDFDokumen20 halamanDeloitte - A Pocket Guide To Singapore Tax 2014 PDFAlison YangBelum ada peringkat

- Tanzania Tax Guide 2012Dokumen14 halamanTanzania Tax Guide 2012Venkatesh GorurBelum ada peringkat

- Income Tax: 2013-14 Brief Commentary On Major Proposed Amendments Salary Income TaxationDokumen10 halamanIncome Tax: 2013-14 Brief Commentary On Major Proposed Amendments Salary Income TaxationUmar SulemanBelum ada peringkat

- This SARS Pocket Tax Guide Has Been Developed To Provide A Synopsis of The Most Important Tax, Duty and Levy Related Information For 2015/16Dokumen2 halamanThis SARS Pocket Tax Guide Has Been Developed To Provide A Synopsis of The Most Important Tax, Duty and Levy Related Information For 2015/16singhjpBelum ada peringkat

- Finance Budget 2023Dokumen4 halamanFinance Budget 2023SakshamBelum ada peringkat

- Tax Reckoner 2011 - 2012Dokumen2 halamanTax Reckoner 2011 - 2012pgshah79Belum ada peringkat

- Budget 14 AnalysisDokumen19 halamanBudget 14 AnalysisSaurav BharadwajBelum ada peringkat

- Taxation 2012 1Dokumen44 halamanTaxation 2012 1mudassarBelum ada peringkat

- BudgetDokumen21 halamanBudgetshweta_narkhede01Belum ada peringkat

- Budget Red Eye 2013Dokumen5 halamanBudget Red Eye 2013Envisage123Belum ada peringkat

- Current Tax Rates and Provisions NigeriaDokumen6 halamanCurrent Tax Rates and Provisions NigeriaVikky MehtaBelum ada peringkat

- Income Tax Rules for Agricultural Income and Property Tax DeductionsDokumen9 halamanIncome Tax Rules for Agricultural Income and Property Tax DeductionsHeraldWilsonBelum ada peringkat

- Service Tax Report on Key Provisions and ComplianceDokumen19 halamanService Tax Report on Key Provisions and CompliancemayankkrishnaBelum ada peringkat

- AcvdvdDokumen4 halamanAcvdvdvivek kasamBelum ada peringkat

- 49 Tax Rates For A y 2011 12Dokumen8 halaman49 Tax Rates For A y 2011 12shitalBelum ada peringkat

- Income Tax ReturnDokumen57 halamanIncome Tax ReturnMalik WasimBelum ada peringkat

- TRAIN LAW - 3.9.18 - Laguna ChapterDokumen408 halamanTRAIN LAW - 3.9.18 - Laguna ChapterDeoshel AlagonBelum ada peringkat

- PWC DTC 2010 SnapshotDokumen7 halamanPWC DTC 2010 SnapshotGs ShikshaBelum ada peringkat

- Budget-Dtc-Tax Exemption IncomeDokumen35 halamanBudget-Dtc-Tax Exemption IncomeAnkit MachharBelum ada peringkat

- Highlights of Union Budget 2010 Income Tax ProposalsDokumen8 halamanHighlights of Union Budget 2010 Income Tax ProposalsparthsomaiyaBelum ada peringkat

- CHAPTER 5 Corporate Income Taxation Regular Corporations ModuleDokumen10 halamanCHAPTER 5 Corporate Income Taxation Regular Corporations ModuleShane Mark CabiasaBelum ada peringkat

- Salient Features: Customs Budgetary Measures 2008-09Dokumen16 halamanSalient Features: Customs Budgetary Measures 2008-09sadiajanBelum ada peringkat

- RSM South Africa Tax Guide 2023-24Dokumen10 halamanRSM South Africa Tax Guide 2023-24mkhize.christian.21Belum ada peringkat

- Tax Proposals in Financial Budget 2013-14: Ravi ChhatwaniDokumen4 halamanTax Proposals in Financial Budget 2013-14: Ravi ChhatwanirockyrrBelum ada peringkat

- Budget Tax Guide 2022Dokumen18 halamanBudget Tax Guide 2022PoesBelum ada peringkat

- Income Tax Methods in KenyaDokumen3 halamanIncome Tax Methods in KenyaMercy NamboBelum ada peringkat

- Quick Tax Guide 2023-2024Dokumen26 halamanQuick Tax Guide 2023-2024RobertKimtaiBelum ada peringkat

- Tax System in SyngaporeDokumen21 halamanTax System in SyngaporeMaria BulgaruBelum ada peringkat

- BDO Budget Snapshot - 2012-13Dokumen9 halamanBDO Budget Snapshot - 2012-13Pulluri Ravikumar YugandarBelum ada peringkat

- Upload 2Dokumen27 halamanUpload 2NAGESH PORWALBelum ada peringkat

- Latest Income Tax Slabs and Rates For FY 2013-14 and AS 2014-15Dokumen6 halamanLatest Income Tax Slabs and Rates For FY 2013-14 and AS 2014-15Michaelben MichaelbenBelum ada peringkat

- Budget 2018 Highlights Direct Tax ChangesDokumen5 halamanBudget 2018 Highlights Direct Tax ChangesSrushti BhattBelum ada peringkat

- 53.income Tax Compliance Check ListDokumen5 halaman53.income Tax Compliance Check ListmercatuzBelum ada peringkat

- Tax RateDokumen10 halamanTax Rateusha chimariyaBelum ada peringkat

- 1 .Income Tax On Salaries - (01.06.2015)Dokumen57 halaman1 .Income Tax On Salaries - (01.06.2015)yvBelum ada peringkat

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionDari EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionBelum ada peringkat

- Admin TQMDokumen28 halamanAdmin TQMManuel Sanchez QuispeBelum ada peringkat

- Kenya's 2016/17 Budget Statement focuses on consolidating economic gainsDokumen35 halamanKenya's 2016/17 Budget Statement focuses on consolidating economic gainsMwende KyaniaBelum ada peringkat

- Motor Vehicles Cycle Mc-2013rrrDokumen1 halamanMotor Vehicles Cycle Mc-2013rrrKalGeorgeBelum ada peringkat

- Value Added TaxDokumen27 halamanValue Added TaxKalGeorgeBelum ada peringkat

- Work Injury Benefits ACT 2007Dokumen49 halamanWork Injury Benefits ACT 2007KalGeorge100% (1)

- Tax Procedures Act, 2015 FullDokumen82 halamanTax Procedures Act, 2015 FullKalGeorgeBelum ada peringkat

- 2015 Syllabus PDFDokumen5 halaman2015 Syllabus PDFKalGeorgeBelum ada peringkat

- Manual TransmissionDokumen16 halamanManual TransmissionKalGeorgeBelum ada peringkat

- Taxation of Unit TrustsDokumen1 halamanTaxation of Unit TrustsKalGeorgeBelum ada peringkat

- Seed Catolgue 2014-1 PDFDokumen12 halamanSeed Catolgue 2014-1 PDFKalGeorgeBelum ada peringkat

- Print - Minimum Wage Rates in KenyaDokumen2 halamanPrint - Minimum Wage Rates in KenyaKalGeorgeBelum ada peringkat

- 01 H 20120814135404Dokumen1 halaman01 H 20120814135404KalGeorgeBelum ada peringkat

- Retirement BenefitsDokumen4 halamanRetirement BenefitsKalGeorgeBelum ada peringkat

- Vat Act 2008Dokumen150 halamanVat Act 2008Githinji GatheruBelum ada peringkat

- Enabling Multiple Currency in Tally: Operations Alteration ScreenDokumen15 halamanEnabling Multiple Currency in Tally: Operations Alteration ScreenKalGeorgeBelum ada peringkat

- Accountanct Firm RankingDokumen3 halamanAccountanct Firm RankingKalGeorgeBelum ada peringkat

- A Guide To Property Law in UgandaDokumen60 halamanA Guide To Property Law in UgandaEmmanuel OtengBelum ada peringkat

- Hague Proceedings 7th April 2011Dokumen4 halamanHague Proceedings 7th April 2011KalGeorgeBelum ada peringkat

- 8 Steps For Redeeming MARRIAGEDokumen3 halaman8 Steps For Redeeming MARRIAGEKalGeorgeBelum ada peringkat

- Free Water BillDokumen1 halamanFree Water BillDuurgaaBelum ada peringkat

- Negotiable Instruments Types & PartiesDokumen4 halamanNegotiable Instruments Types & PartiesPraveen KumarBelum ada peringkat

- CIR v. Isabela Cultural Corp GR No. 17223, 12 Feb 2007Dokumen5 halamanCIR v. Isabela Cultural Corp GR No. 17223, 12 Feb 2007Marge OstanBelum ada peringkat

- A Guide To Taxation in The PhilippinesDokumen5 halamanA Guide To Taxation in The PhilippinesNathaniel MartinezBelum ada peringkat

- QESCO BILL NewDokumen1 halamanQESCO BILL NewBilal AhmedBelum ada peringkat

- Bank StatementDokumen29 halamanBank StatementhfcoachrohitBelum ada peringkat

- Ms Cynthia Ntombenkosi Lenong Ward 09 Newrest Sterkspruit 9762Dokumen2 halamanMs Cynthia Ntombenkosi Lenong Ward 09 Newrest Sterkspruit 9762Steev Howard QuinnBelum ada peringkat

- NAAF041ENDokumen1 halamanNAAF041ENdriveralotBelum ada peringkat

- Regional Evaluation Board (Reb) Resolution On The Application For Compromise Settlement or For Abatement/ Cancellation of AssessmentDokumen3 halamanRegional Evaluation Board (Reb) Resolution On The Application For Compromise Settlement or For Abatement/ Cancellation of AssessmentHanabishi RekkaBelum ada peringkat

- Icome Regime of AgriDokumen13 halamanIcome Regime of AgriZ_JahangeerBelum ada peringkat

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokumen1 halamanTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Kiran PeddavoraBelum ada peringkat

- F 706Dokumen31 halamanF 706Bogdan PraščevićBelum ada peringkat

- Case 3 - 1: Maynard Company (B) : DR Ashish Varma / IMTDokumen4 halamanCase 3 - 1: Maynard Company (B) : DR Ashish Varma / IMTkunalBelum ada peringkat

- PGBP New SlidesDokumen40 halamanPGBP New SlidesSachin Jain100% (2)

- Taxation ProjectDokumen15 halamanTaxation ProjectTanya SinglaBelum ada peringkat

- Interface Error RepositoryDokumen9 halamanInterface Error RepositorynagalakshmiBelum ada peringkat

- OOIDA Cost Per Mile CalculatorDokumen8 halamanOOIDA Cost Per Mile CalculatorgowthamkumaarBelum ada peringkat

- Constitutional Framework of GST in IndiaDokumen20 halamanConstitutional Framework of GST in IndiaABBelum ada peringkat

- C1 - A New Hire, S Dilemma Reporting CorruptionDokumen3 halamanC1 - A New Hire, S Dilemma Reporting CorruptionNutanBelum ada peringkat

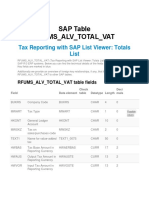

- RFUMSDokumen2 halamanRFUMSSivakumar ThangarajanBelum ada peringkat