Anda mungkin juga menyukai

- Rate IncreaseDokumen1 halamanRate IncreaseJuliusBelum ada peringkat

- The Great Waves of Change - The New Message From GodDokumen4 halamanThe Great Waves of Change - The New Message From GodJuliusBelum ada peringkat

- A Message of Change - Bay Area Christian ChurchDokumen5 halamanA Message of Change - Bay Area Christian ChurchJuliusBelum ada peringkat

- Ec's Method Not Good Enough To Accomplish The Sc's OrderDokumen3 halamanEc's Method Not Good Enough To Accomplish The Sc's OrderJuliusBelum ada peringkat

- I Won't Name My Bribers' - Prof MarteyDokumen4 halamanI Won't Name My Bribers' - Prof MarteyJuliusBelum ada peringkat

- Rise Up and Be Heard #DumsormuststopDokumen3 halamanRise Up and Be Heard #DumsormuststopJuliusBelum ada peringkat

- Rome was not destroyed in a day: How innovation and empires evolve gradually over timeDokumen3 halamanRome was not destroyed in a day: How innovation and empires evolve gradually over timeJuliusBelum ada peringkat

- Taxation On Pensions Is UnjusticeDokumen2 halamanTaxation On Pensions Is UnjusticeJuliusBelum ada peringkat

- DownDokumen1 halamanDownJuliusBelum ada peringkat

- The HonDokumen2 halamanThe HonJuliusBelum ada peringkat

- Blackout in Ghana and Mango BusinessDokumen1 halamanBlackout in Ghana and Mango BusinessJuliusBelum ada peringkat

- 150 FEED 100 Clearing of PenDokumen1 halaman150 FEED 100 Clearing of PenJuliusBelum ada peringkat

- ThankDokumen1 halamanThankJuliusBelum ada peringkat

- CouponDokumen1 halamanCouponJuliusBelum ada peringkat

- CouponDokumen1 halamanCouponJuliusBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Economics Class 01 (Abc of Economics) PDFDokumen10 halamanEconomics Class 01 (Abc of Economics) PDFmakbul rahmanBelum ada peringkat

- Online Test 2 - Introductory Macroeconomics (ECON10003 - 2023 - SM2)Dokumen6 halamanOnline Test 2 - Introductory Macroeconomics (ECON10003 - 2023 - SM2)ducminhlnilesBelum ada peringkat

- Importance of Industry AnalysisDokumen15 halamanImportance of Industry AnalysisAbhin BhatBelum ada peringkat

- ECO-12 Unit 5.1Dokumen18 halamanECO-12 Unit 5.1Prabin KhanalBelum ada peringkat

- China Pharmaceuticals and Healthcare Report Q2 2019 PDFDokumen96 halamanChina Pharmaceuticals and Healthcare Report Q2 2019 PDFPranay SumblyBelum ada peringkat

- CH 29 The Monetary SystemDokumen43 halamanCH 29 The Monetary SystemNazeBelum ada peringkat

- Mckinsey On FinanceDokumen36 halamanMckinsey On FinanceRavi BabuBelum ada peringkat

- Chapter 3Dokumen44 halamanChapter 3zhaofangjie0510Belum ada peringkat

- Eco Prakash PDFDokumen10 halamanEco Prakash PDFPanwar SurajBelum ada peringkat

- LatinFocus Consensus Forecast - April 2020 PDFDokumen152 halamanLatinFocus Consensus Forecast - April 2020 PDFFelipe OrnellesBelum ada peringkat

- IGCSE BUSINESS STUDIES EXAMINES GOVERNMENT ECONOMIC POLICIESDokumen5 halamanIGCSE BUSINESS STUDIES EXAMINES GOVERNMENT ECONOMIC POLICIESSwagata DebnathBelum ada peringkat

- Exam Sana 2Dokumen5 halamanExam Sana 2Mahmoud HamedBelum ada peringkat

- Bba Semester I and II Part II and IIIDokumen62 halamanBba Semester I and II Part II and IIIAmandeep Singh BaaghiBelum ada peringkat

- Chapter 13Dokumen15 halamanChapter 13greenapl01Belum ada peringkat

- CH 08Dokumen27 halamanCH 08MiraBelum ada peringkat

- 06Dokumen9 halaman06Shubham RawatBelum ada peringkat

- GDP vs GNP: Key Differences ExplainedDokumen19 halamanGDP vs GNP: Key Differences ExplainedJoy PalBelum ada peringkat

- Globalization in The Asia Pacific and South AsiaDokumen3 halamanGlobalization in The Asia Pacific and South AsiaKaren Aniñon BarcelonBelum ada peringkat

- Vndirect Report - Vietnam 2022 GrowthDokumen227 halamanVndirect Report - Vietnam 2022 GrowthNGOC ANH NGUYENBelum ada peringkat

- Microeconomics: by Michael J. Buckle, PHD, James Seaton, PHD, Sandeep Singh, PHD, Cfa, Cipim, and Stephen Thomas, PHDDokumen28 halamanMicroeconomics: by Michael J. Buckle, PHD, James Seaton, PHD, Sandeep Singh, PHD, Cfa, Cipim, and Stephen Thomas, PHDDouglas ZimunyaBelum ada peringkat

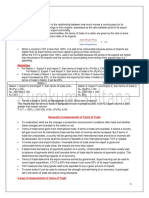

- Terms of Trade AnalysisDokumen4 halamanTerms of Trade AnalysisFatema SultanaBelum ada peringkat

- Capitalism vs. Socialism vs. CommunismDokumen16 halamanCapitalism vs. Socialism vs. CommunismEnrico Charles FajardoBelum ada peringkat

- Business Cycle, Unemployment and InflationDokumen59 halamanBusiness Cycle, Unemployment and InflationSerena VillarealBelum ada peringkat

- UGmacro2022 ps1Dokumen2 halamanUGmacro2022 ps1Chunming TangBelum ada peringkat

- Segmentation IllyDokumen8 halamanSegmentation IllyBella Dela RosaBelum ada peringkat

- ChoiceDokumen2 halamanChoiceTho ThoBelum ada peringkat

- Assignment Topics 2 - AEC 101 - 19-20 BatchDokumen3 halamanAssignment Topics 2 - AEC 101 - 19-20 BatchRubybharatBelum ada peringkat

- Relative Income HypothesisDokumen13 halamanRelative Income HypothesisTaruna Bajaj100% (1)

- The Shortrun Tradeoff Between Inflation and UnemploymentDokumen42 halamanThe Shortrun Tradeoff Between Inflation and UnemploymentJeremy SilaenBelum ada peringkat

- Fiscal PolicyDokumen13 halamanFiscal PolicyAakash SaxenaBelum ada peringkat