Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

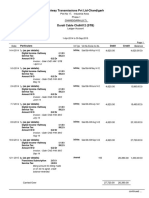

- Friends Cable Network-Jassi CHDH015Dokumen11 halamanFriends Cable Network-Jassi CHDH015Kanishk YadavBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Freinds Cable Jaspal 22281 STBDokumen1 halamanFreinds Cable Jaspal 22281 STBKanishk YadavBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Friends Cable Nw-CHDH015 (STB)Dokumen1 halamanFriends Cable Nw-CHDH015 (STB)Kanishk YadavBelum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Friends Cable Network-Jassi CHDH015Dokumen11 halamanFriends Cable Network-Jassi CHDH015Kanishk YadavBelum ada peringkat

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- New Gill Cable - 22275 - CommDokumen3 halamanNew Gill Cable - 22275 - CommKanishk YadavBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Friends CBL Jaspal Ph-1-22281Dokumen8 halamanFriends CBL Jaspal Ph-1-22281Kanishk YadavBelum ada peringkat

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Friends Cable NW - CHDH016 (STB)Dokumen2 halamanFriends Cable NW - CHDH016 (STB)Kanishk YadavBelum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Friends Cable Jaswinder-24539Dokumen8 halamanFriends Cable Jaswinder-24539Kanishk YadavBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Friends Cable NW - CHDH016 (STB)Dokumen2 halamanFriends Cable NW - CHDH016 (STB)Kanishk YadavBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Friends Cable Network CHDH016 CommDokumen4 halamanFriends Cable Network CHDH016 CommKanishk YadavBelum ada peringkat

- Friends Cable Network-Jaswinder CHDH016Dokumen11 halamanFriends Cable Network-Jaswinder CHDH016Kanishk YadavBelum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Friends Cable Network 24539 COMMDokumen3 halamanFriends Cable Network 24539 COMMKanishk YadavBelum ada peringkat

- Durali Cable SA C 0029 10Dokumen2 halamanDurali Cable SA C 0029 10Kanishk YadavBelum ada peringkat

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- B&W EntDokumen8 halamanB&W EntKanishk YadavBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Durali Cable Durali SA C 0019 09Dokumen4 halamanDurali Cable Durali SA C 0019 09Kanishk YadavBelum ada peringkat

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- 20150430175941ISTC Information Brochure - 2015 PDFDokumen28 halaman20150430175941ISTC Information Brochure - 2015 PDFKanishk YadavBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- 20150430175941ISTC Information Brochure - 2015 PDFDokumen28 halaman20150430175941ISTC Information Brochure - 2015 PDFKanishk YadavBelum ada peringkat

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- B&W EntDokumen8 halamanB&W EntKanishk YadavBelum ada peringkat

- Durali Cable Chdh012Dokumen3 halamanDurali Cable Chdh012Kanishk YadavBelum ada peringkat

- Durali Cable Chdh012 (STB)Dokumen2 halamanDurali Cable Chdh012 (STB)Kanishk YadavBelum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- New Microsoft Office Word DocumentDokumen8 halamanNew Microsoft Office Word DocumentKanishk YadavBelum ada peringkat

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- DSCN-Arora Cable (Half Year)Dokumen15 halamanDSCN-Arora Cable (Half Year)Kanishk YadavBelum ada peringkat

- 12th ExemplerDokumen359 halaman12th Exemplergiophilip100% (1)

- B&W SCN Rs. 67 LacDokumen6 halamanB&W SCN Rs. 67 LacKanishk YadavBelum ada peringkat

- DSCN Lco DraftDokumen6 halamanDSCN Lco DraftKanishk YadavBelum ada peringkat

- Landran Cable NetworkDokumen6 halamanLandran Cable NetworkKanishk YadavBelum ada peringkat

- Friends Cable (Tony)Dokumen6 halamanFriends Cable (Tony)Kanishk YadavBelum ada peringkat

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

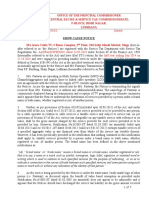

- The Commissioner, Central Excise Commissionerate, Chandigarh - IIDokumen3 halamanThe Commissioner, Central Excise Commissionerate, Chandigarh - IIKanishk YadavBelum ada peringkat

- Cargas Termicas HapDokumen2 halamanCargas Termicas HapArq Alfonso RicoBelum ada peringkat

- Status of Implementation of Prior Years' Audit RecommendationsDokumen10 halamanStatus of Implementation of Prior Years' Audit RecommendationsJoy AcostaBelum ada peringkat

- Iata 2008 - Annex ADokumen11 halamanIata 2008 - Annex Agurungbhim100% (1)

- Solar Smart Irrigation SystemDokumen22 halamanSolar Smart Irrigation SystemSubhranshu Mohapatra100% (1)

- Mathswatch Student GuideDokumen8 halamanMathswatch Student Guideolamideidowu021Belum ada peringkat

- Tower BridgeDokumen6 halamanTower BridgeCalvin PratamaBelum ada peringkat

- Trapatt ModeDokumen30 halamanTrapatt Modebchaitanya_555100% (1)

- Lateral Pile Paper - Rev01Dokumen6 halamanLateral Pile Paper - Rev01YibinGongBelum ada peringkat

- Plewa2016 - Reputation in Higher Education: A Fuzzy Set Analysis of Resource ConfigurationsDokumen9 halamanPlewa2016 - Reputation in Higher Education: A Fuzzy Set Analysis of Resource ConfigurationsAlice ChenBelum ada peringkat

- Key GroupsDokumen11 halamanKey GroupsJose RodríguezBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Abstract 2 TonesDokumen8 halamanAbstract 2 TonesFilip FilipovicBelum ada peringkat

- Contracts Act, 2010Dokumen59 halamanContracts Act, 2010Sam KBelum ada peringkat

- Operations Management: Green Facility Location: Case StudyDokumen23 halamanOperations Management: Green Facility Location: Case StudyBhavya KhattarBelum ada peringkat

- Internet Phone Services Simplified (VoIP)Dokumen176 halamanInternet Phone Services Simplified (VoIP)sumanth83137Belum ada peringkat

- Sky 1Dokumen14 halamanSky 1Vũ Quang HưngBelum ada peringkat

- Icd-10 CM Step by Step Guide SheetDokumen12 halamanIcd-10 CM Step by Step Guide SheetEdel DurdallerBelum ada peringkat

- Bacnet Today: W W W W WDokumen8 halamanBacnet Today: W W W W Wmary AzevedoBelum ada peringkat

- Thesun 2009-07-09 Page05 Ex-Pka Director Sues Nine For rm11mDokumen1 halamanThesun 2009-07-09 Page05 Ex-Pka Director Sues Nine For rm11mImpulsive collectorBelum ada peringkat

- 2008 Almocera vs. OngDokumen11 halaman2008 Almocera vs. OngErika C. DizonBelum ada peringkat

- COEN 252 Computer Forensics: Incident ResponseDokumen39 halamanCOEN 252 Computer Forensics: Incident ResponseDudeviswaBelum ada peringkat

- Asmsc 1119 PDFDokumen9 halamanAsmsc 1119 PDFAstha WadhwaBelum ada peringkat

- Enterprise Management System: Reference W.S.JawadekarDokumen34 halamanEnterprise Management System: Reference W.S.JawadekarPolice stationBelum ada peringkat

- Woodworking SyllabusDokumen3 halamanWoodworking SyllabusLeonard Andrew ManuevoBelum ada peringkat

- Type SAP Usage / Definition Example Procurement RotablesDokumen4 halamanType SAP Usage / Definition Example Procurement Rotablessabya1411Belum ada peringkat

- METHODOLOG1Dokumen3 halamanMETHODOLOG1Essa M RoshanBelum ada peringkat

- Environmental Life Cycle AssessmentDokumen1 halamanEnvironmental Life Cycle Assessmentkayyappan1957Belum ada peringkat

- Asus P8Z68-V PRO GEN3 ManualDokumen146 halamanAsus P8Z68-V PRO GEN3 ManualwkfanBelum ada peringkat

- Cost Justifying HRIS InvestmentsDokumen21 halamanCost Justifying HRIS InvestmentsNilesh MandlikBelum ada peringkat

- Is LNG Still Competitive With Other Liquid Fuels?: Proceedings, Ascope'97 ConferenceDokumen18 halamanIs LNG Still Competitive With Other Liquid Fuels?: Proceedings, Ascope'97 Conferencemanolo8catalanBelum ada peringkat

- Macaw Recovery Network - Výroční Zpráva 2022Dokumen20 halamanMacaw Recovery Network - Výroční Zpráva 2022Jan.PotucekBelum ada peringkat