Anda mungkin juga menyukai

- Income Tax Law & PracticeDokumen60 halamanIncome Tax Law & Practicesebastianks94% (17)

- Purchases-Adlaw (Month of February 2019)Dokumen121 halamanPurchases-Adlaw (Month of February 2019)Giann Fritz AlvarezBelum ada peringkat

- Wired UK-January 2018 PDFDokumen176 halamanWired UK-January 2018 PDFishaan_gautam100% (1)

- TAX - LEAD BATCH 3 - Preweek 2Dokumen13 halamanTAX - LEAD BATCH 3 - Preweek 2Josiah ZeusBelum ada peringkat

- 1040 Exam Prep: Module I: The Form 1040 FormulaDari Everand1040 Exam Prep: Module I: The Form 1040 FormulaPenilaian: 1 dari 5 bintang1/5 (3)

- Compensation and BenefitsDokumen3 halamanCompensation and BenefitsBago Resilyn100% (1)

- Corporate TaxDokumen30 halamanCorporate TaxVijay KumarBelum ada peringkat

- JLN Pending, Kuching 1 30/11/22Dokumen4 halamanJLN Pending, Kuching 1 30/11/22Jue tingsBelum ada peringkat

- Gutierrez vs. CIR 1957: Taxation I Case Digest CompilationDokumen2 halamanGutierrez vs. CIR 1957: Taxation I Case Digest CompilationGyrsyl Jaisa GuerreroBelum ada peringkat

- Nikhil Equitas StatementDokumen2 halamanNikhil Equitas Statementprem yadav100% (1)

- Income Tax Law and PracticesDokumen148 halamanIncome Tax Law and PracticesUjjwal KandhaweBelum ada peringkat

- Applied Direct TaxationDokumen548 halamanApplied Direct TaxationVarun SinghBelum ada peringkat

- Taxation System in IndiaDokumen35 halamanTaxation System in IndiaSaif UddinBelum ada peringkat

- Basic Concept & Residential Status of ItDokumen15 halamanBasic Concept & Residential Status of ItKANNAN MBelum ada peringkat

- Tax Combined NotesDokumen48 halamanTax Combined NotesignatiousmugovaBelum ada peringkat

- Project Topic: Income Tax Systems in Pakistan, India & UKDokumen53 halamanProject Topic: Income Tax Systems in Pakistan, India & UKAfzal RocksxBelum ada peringkat

- Everything You Need to Know About Income TaxDokumen11 halamanEverything You Need to Know About Income TaxLAKSHMANARAO PBelum ada peringkat

- Gnesh - Thakkar.7 Ncometaxguru/ Ajigneshthakkar: Poured in by MeDokumen111 halamanGnesh - Thakkar.7 Ncometaxguru/ Ajigneshthakkar: Poured in by Mepandeyaman7608Belum ada peringkat

- Unit-1 IT 2023-24Dokumen11 halamanUnit-1 IT 2023-24avinashhpv7785Belum ada peringkat

- IncomeTax MaterialDokumen91 halamanIncomeTax MaterialSandeep JaiswalBelum ada peringkat

- 18878sm DTL Finalnew Cp1Dokumen28 halaman18878sm DTL Finalnew Cp1manisha maniBelum ada peringkat

- Tax Structure in IndiaDokumen37 halamanTax Structure in IndiaShiva Kumar BandaruBelum ada peringkat

- India's Investment Tax StructureDokumen15 halamanIndia's Investment Tax StructureassatputeBelum ada peringkat

- Income TaxDokumen51 halamanIncome TaxInternet 223Belum ada peringkat

- Business Taxation Unit 1Dokumen23 halamanBusiness Taxation Unit 1Akash GoreBelum ada peringkat

- Direct and Indirect Taxes ExplainedDokumen42 halamanDirect and Indirect Taxes ExplainedArpit MadaanBelum ada peringkat

- BCO 11 Block 03Dokumen70 halamanBCO 11 Block 03Al OkBelum ada peringkat

- Income Tax in India - Wikipedia, The Free EncyclopediaDokumen13 halamanIncome Tax in India - Wikipedia, The Free EncyclopediaAnonymous utfuIcnBelum ada peringkat

- Definition of Income TaxDokumen14 halamanDefinition of Income Taxms_ssachinBelum ada peringkat

- Tax Notes - 1Dokumen23 halamanTax Notes - 1POWER LINKBelum ada peringkat

- ITLA (UNIT 1) Basic Income Tax ConceptsDokumen11 halamanITLA (UNIT 1) Basic Income Tax ConceptsAbdul basitBelum ada peringkat

- INCOME TAX GUIDANCEDokumen27 halamanINCOME TAX GUIDANCEBariq BadarBelum ada peringkat

- Individual Txation FY 2019 20 With Demo of Return FilingDokumen73 halamanIndividual Txation FY 2019 20 With Demo of Return FilingGanesh PBelum ada peringkat

- DT IntroductionDokumen40 halamanDT Introductionprashanthreddy02234Belum ada peringkat

- Introduction to Indian Taxation SystemDokumen65 halamanIntroduction to Indian Taxation SystemDinesh VermaBelum ada peringkat

- Taxation System in IndiaDokumen5 halamanTaxation System in IndiaTanvi SanghaviBelum ada peringkat

- Taxation LawDokumen67 halamanTaxation LawAdv Sheetal SaylekarBelum ada peringkat

- Taxation Laws UNIT 1Dokumen13 halamanTaxation Laws UNIT 1Heena ManwaniBelum ada peringkat

- Indian Taxation System Project ReportDokumen59 halamanIndian Taxation System Project Reportniket_dattaniBelum ada peringkat

- Taxation Flow PresentationDokumen73 halamanTaxation Flow PresentationMohan ChoudharyBelum ada peringkat

- Ajit Kumar SatapathyDokumen32 halamanAjit Kumar Satapathyajitkumarsatapathy3Belum ada peringkat

- VND Openxmlformats-Officedocument Wordprocessingml Document&rendition 1-19Dokumen18 halamanVND Openxmlformats-Officedocument Wordprocessingml Document&rendition 1-192100 42 Shazma ShabanBelum ada peringkat

- Share TAX LAW 403 UNIT 1Dokumen15 halamanShare TAX LAW 403 UNIT 1Rajeev shuklaBelum ada peringkat

- The Tax Structure in India Is Divided Into Direct and Indirect TaxesDokumen9 halamanThe Tax Structure in India Is Divided Into Direct and Indirect TaxesUjjwal RustagiBelum ada peringkat

- Taxation On The Digital Economy in India An AnalysisDokumen16 halamanTaxation On The Digital Economy in India An AnalysisNUPUR MISHRABelum ada peringkat

- Incometaxact1961 130812110744 Phpapp02Dokumen23 halamanIncometaxact1961 130812110744 Phpapp02Let's Crack CATBelum ada peringkat

- Business Taxation Module 1&2Dokumen13 halamanBusiness Taxation Module 1&2Khushboo Parikh100% (1)

- Calculate your income taxDokumen24 halamanCalculate your income taxSupreet KaurBelum ada peringkat

- ProjectDokumen10 halamanProjectAyush JainBelum ada peringkat

- Income Tax, IndiaDokumen11 halamanIncome Tax, Indiahimanshu_mathur88Belum ada peringkat

- Basics of Taxation in India - Types, Rates and Key ConceptsDokumen7 halamanBasics of Taxation in India - Types, Rates and Key ConceptsmijjinBelum ada peringkat

- Taxation Notes 2021Dokumen135 halamanTaxation Notes 2021Viral MehtaBelum ada peringkat

- 603 - Taxation LawsDokumen41 halaman603 - Taxation LawsSiddhartha Singhal057Belum ada peringkat

- Taxation of Salaried EmployeesDokumen39 halamanTaxation of Salaried Employeessailolla30Belum ada peringkat

- Taxation - System in IndiaDokumen12 halamanTaxation - System in Indiaahil XO1BDBelum ada peringkat

- BASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmanDokumen14 halamanBASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmansaadmansheedyBelum ada peringkat

- Navjot Singh (BBA III Sem)Dokumen13 halamanNavjot Singh (BBA III Sem)Ramandeep SinghBelum ada peringkat

- DIRECT TAXES OVERVIEWDokumen60 halamanDIRECT TAXES OVERVIEWthangarajbala123Belum ada peringkat

- Assignment: Taxation System in India'Dokumen14 halamanAssignment: Taxation System in India'Devendra OjhaBelum ada peringkat

- Individual Taxation (Ay 2019-20)Dokumen29 halamanIndividual Taxation (Ay 2019-20)Mudit SinghBelum ada peringkat

- Presentation On Income Tax ActDokumen31 halamanPresentation On Income Tax ActJst DeepakBelum ada peringkat

- Income Tax: B C: Asic OnceptsDokumen35 halamanIncome Tax: B C: Asic OnceptsAbhinandan soniBelum ada peringkat

- Module 1, 2 & 3Dokumen30 halamanModule 1, 2 & 3JAGRITI SINGH JUBelum ada peringkat

- New Taxation ProjectDokumen10 halamanNew Taxation ProjectAkash BiradarBelum ada peringkat

- Hari Income Tax Department - Do CXDokumen12 halamanHari Income Tax Department - Do CXNelluri Surendhar ChowdaryBelum ada peringkat

- E Text Week 1 Module 1.2Dokumen5 halamanE Text Week 1 Module 1.2bsc slpBelum ada peringkat

- Indonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaDari EverandIndonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaBelum ada peringkat

- Critical ReasoningDokumen13 halamanCritical Reasoningishaan_gautamBelum ada peringkat

- What To Read - and What Not To Read - On GRE Reading Comprehension Passages - GREDokumen5 halamanWhat To Read - and What Not To Read - On GRE Reading Comprehension Passages - GREishaan_gautamBelum ada peringkat

- Vocabulary A2Dokumen36 halamanVocabulary A2ishaan_gautamBelum ada peringkat

- Assessing the Value of Challenging IdeasDokumen7 halamanAssessing the Value of Challenging Ideasishaan_gautamBelum ada peringkat

- Sample Issue (Parik Sir)Dokumen2 halamanSample Issue (Parik Sir)ishaan_gautamBelum ada peringkat

- Want To Do Better On GRE Quant - Put The Pen Down! - GREDokumen3 halamanWant To Do Better On GRE Quant - Put The Pen Down! - GREishaan_gautamBelum ada peringkat

- Governments Should Place FewDokumen4 halamanGovernments Should Place Fewishaan_gautamBelum ada peringkat

- Vocabulary A1Dokumen30 halamanVocabulary A1ishaan_gautamBelum ada peringkat

- Sample Argument (ETS)Dokumen7 halamanSample Argument (ETS)ishaan_gautam100% (1)

- Sample Argument (Parik Sir)Dokumen4 halamanSample Argument (Parik Sir)ishaan_gautamBelum ada peringkat

- GRE Word ThesaurusDokumen137 halamanGRE Word ThesaurusPhanidhar GubbalaBelum ada peringkat

- Frank Bruinsma, Eric Pels, Piet Rietveld, Hugo Priemus, Bert Van Wee (Auth.), Dr. Frank Bruinsma, Dr. Eric Pels, Prof. Dr. Piet Rietveld, Prof. Dr. Hugo Priemus, Prof. Dr. Bert Van Wee (Eds.)-RailwayDokumen427 halamanFrank Bruinsma, Eric Pels, Piet Rietveld, Hugo Priemus, Bert Van Wee (Auth.), Dr. Frank Bruinsma, Dr. Eric Pels, Prof. Dr. Piet Rietveld, Prof. Dr. Hugo Priemus, Prof. Dr. Bert Van Wee (Eds.)-Railwayishaan_gautamBelum ada peringkat

- Bert Van Wee PDFDokumen21 halamanBert Van Wee PDFishaan_gautamBelum ada peringkat

- Preferences For Modes, Residential Location and TravelDokumen12 halamanPreferences For Modes, Residential Location and Travelishaan_gautamBelum ada peringkat

- EconomicsDokumen32 halamanEconomicsgoodlucksarveshBelum ada peringkat

- Why Critical Thinking Is ImportantDokumen19 halamanWhy Critical Thinking Is ImportantVincent Hà Quốc DũngBelum ada peringkat

- January 2016Dokumen80 halamanJanuary 2016Apratim BhaskarBelum ada peringkat

- XAT 2016 Question Paper With Answer KeyDokumen31 halamanXAT 2016 Question Paper With Answer Keyishaan_gautamBelum ada peringkat

- Preferences For Modes, Residential Location and TravelDokumen12 halamanPreferences For Modes, Residential Location and Travelishaan_gautamBelum ada peringkat

- The Concept of MoneyDokumen8 halamanThe Concept of Moneyishaan_gautamBelum ada peringkat

- The Concept of MoneyDokumen8 halamanThe Concept of Moneyishaan_gautamBelum ada peringkat

- ME 8.machine DesignDokumen210 halamanME 8.machine DesignDurgaBelum ada peringkat

- January 2016Dokumen80 halamanJanuary 2016Apratim BhaskarBelum ada peringkat

- What Has Happened Since 1991 - An Assessment of Economic ReformsDokumen11 halamanWhat Has Happened Since 1991 - An Assessment of Economic ReformsKalpit ShahBelum ada peringkat

- Xuberance ReportDokumen9 halamanXuberance Reporttarunsrawal1Belum ada peringkat

- Universe and The Solar SystemDokumen12 halamanUniverse and The Solar Systemishaan_gautamBelum ada peringkat

- Inidan Economic Reforms by M.ahluwaliaDokumen12 halamanInidan Economic Reforms by M.ahluwaliababu4u10Belum ada peringkat

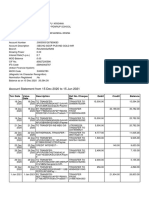

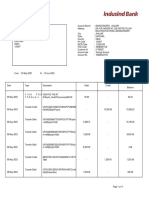

- Account statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021Dokumen9 halamanAccount statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021SRINIVASARAO JONNALABelum ada peringkat

- Bank StatementsDokumen7 halamanBank Statementszfh2b2tkv4Belum ada peringkat

- Project Cost and Profit Blank Estimate TemplateDokumen4 halamanProject Cost and Profit Blank Estimate Templateهيثم الحدادBelum ada peringkat

- Practice ExercisesDokumen2 halamanPractice ExercisesNikki Labial0% (1)

- China Bank Vs CIR Passive Investment IncomeDokumen7 halamanChina Bank Vs CIR Passive Investment IncomeThremzone17Belum ada peringkat

- Amrapali Spring Meadows 2 3 BHK Flats For Sale Noida Extension 2nd Phase Payment PlanDokumen1 halamanAmrapali Spring Meadows 2 3 BHK Flats For Sale Noida Extension 2nd Phase Payment PlanAhmad KhanBelum ada peringkat

- Ola Share 1016517059Dokumen3 halamanOla Share 1016517059jayasundarBelum ada peringkat

- SodaPDF-converted-3months StatementDokumen7 halamanSodaPDF-converted-3months StatementHariharanBelum ada peringkat

- Report 20230604125900Dokumen8 halamanReport 20230604125900AbhimanyuBelum ada peringkat

- Purchase synthetic oil quotationDokumen1 halamanPurchase synthetic oil quotationPANKAJ RAJBelum ada peringkat

- Additional Identified Skills Shortage Payment FactsheetDokumen2 halamanAdditional Identified Skills Shortage Payment FactsheetNick SalomoneBelum ada peringkat

- Tax Fundamentals True or False QuizDokumen13 halamanTax Fundamentals True or False QuizJuan CarlosBelum ada peringkat

- Facts:: Case Digest No. 65 of Lucky O. JavellanaDokumen8 halamanFacts:: Case Digest No. 65 of Lucky O. JavellanaluckyBelum ada peringkat

- International Double Taxation Content Consequences and AvoidanceDokumen11 halamanInternational Double Taxation Content Consequences and AvoidanceMstefBelum ada peringkat

- This Is A Computer Generated Statement and Does Not Require A SignatureDokumen1 halamanThis Is A Computer Generated Statement and Does Not Require A SignatureAbhishekChowdhuryBelum ada peringkat

- Mcgraw Hills Essentials of Federal Taxation 2019 10th Edition Spilker Solutions ManualDokumen26 halamanMcgraw Hills Essentials of Federal Taxation 2019 10th Edition Spilker Solutions ManualNicoleTuckeroajx100% (54)

- Tax on NGOs, Charities and ClubsDokumen5 halamanTax on NGOs, Charities and ClubsSaneej SamsudeenBelum ada peringkat

- Uj TSCM Cep Advdip Logistics Bridging Financials2023 A4 Insert OnlineDokumen1 halamanUj TSCM Cep Advdip Logistics Bridging Financials2023 A4 Insert OnlineOmolemo MnguniBelum ada peringkat

- PIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityDokumen1 halamanPIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue Authorityseres jakoBelum ada peringkat

- 2020 P T D 1908Dokumen2 halaman2020 P T D 1908haseeb AhsanBelum ada peringkat

- Ofssa Team InvoiceDokumen1 halamanOfssa Team Invoicevii3tstarBelum ada peringkat

- Banglore Hotel Bill - 08 JAN 2023Dokumen1 halamanBanglore Hotel Bill - 08 JAN 2023Devendar UradiBelum ada peringkat

- UmMwWHVzMFEwc3paWkRSWkVjS0o3Zz09 InvoiceDokumen2 halamanUmMwWHVzMFEwc3paWkRSWkVjS0o3Zz09 InvoiceNSTI AKKIBelum ada peringkat

- TY2020 - Fair Fight Action - Form 990-PDokumen78 halamanTY2020 - Fair Fight Action - Form 990-PWashington ExaminerBelum ada peringkat