Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- BBA Introduction To Business Economics and Fundamental ConceptsDokumen30 halamanBBA Introduction To Business Economics and Fundamental ConceptsLeamae Lacsina Garcia100% (1)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- BCG Matrix Explained - Product Fitment (Neelkamal Chair)Dokumen12 halamanBCG Matrix Explained - Product Fitment (Neelkamal Chair)jaywilson3enBelum ada peringkat

- Consolidation of Financial Statments Final ProjectDokumen35 halamanConsolidation of Financial Statments Final ProjectK-Ayurveda WelexBelum ada peringkat

- LIM TONG LIM Vs CADokumen3 halamanLIM TONG LIM Vs CARoseannvalorie JaramillaBelum ada peringkat

- Business Plan of Stone BusinessDokumen16 halamanBusiness Plan of Stone BusinessFarhanChowdhuryMehdi0% (1)

- Square PharmaDokumen23 halamanSquare PharmaSabrina SamantaBelum ada peringkat

- Ing N.V. Metro Manila Branch Vs Cir DigestDokumen2 halamanIng N.V. Metro Manila Branch Vs Cir Digestbrian jay hernandezBelum ada peringkat

- Loan Disbursement and Recovery Procedures of BKBDokumen10 halamanLoan Disbursement and Recovery Procedures of BKBFarhanChowdhuryMehdiBelum ada peringkat

- Wasim Akram Zabin KhanDokumen70 halamanWasim Akram Zabin KhanamalremeshBelum ada peringkat

- CSR Strategy For Sustainable Business Samy Odemilin and BamptonDokumen16 halamanCSR Strategy For Sustainable Business Samy Odemilin and BamptonabbakaBelum ada peringkat

- Case Study of Luftansa PDFDokumen18 halamanCase Study of Luftansa PDFAnonymous gUySMcpSqBelum ada peringkat

- Top 100 Philippine Cooperatives for 2017Dokumen114 halamanTop 100 Philippine Cooperatives for 2017John aparte100% (1)

- GCE Business Studies May 2016 Unit 2 MSDokumen18 halamanGCE Business Studies May 2016 Unit 2 MSFarhanChowdhuryMehdiBelum ada peringkat

- Pu1473410272 PDFDokumen1 halamanPu1473410272 PDFFarhanChowdhuryMehdiBelum ada peringkat

- 2017 Autumn Routine PDFDokumen6 halaman2017 Autumn Routine PDFFarhanChowdhuryMehdiBelum ada peringkat

- IAL Business Studies May 2014 Unit 1 MSDokumen22 halamanIAL Business Studies May 2014 Unit 1 MSFarhanChowdhuryMehdiBelum ada peringkat

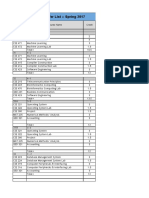

- Course Offer List For Spring-2017 CSE DAY and EVEDokumen6 halamanCourse Offer List For Spring-2017 CSE DAY and EVEFarhanChowdhuryMehdiBelum ada peringkat

- Deepa 2Dokumen13 halamanDeepa 2FarhanChowdhuryMehdiBelum ada peringkat

- GCE Business Studies May 2016 Unit 2 QPDokumen16 halamanGCE Business Studies May 2016 Unit 2 QPFarhanChowdhuryMehdiBelum ada peringkat

- Chapter 1 PowerpointDokumen33 halamanChapter 1 PowerpointFarhanChowdhuryMehdiBelum ada peringkat

- Course Offer List For Spring-2017 CSE DAY and EVEDokumen6 halamanCourse Offer List For Spring-2017 CSE DAY and EVEFarhanChowdhuryMehdiBelum ada peringkat

- Community Center (Sy-3)Dokumen18 halamanCommunity Center (Sy-3)FarhanChowdhuryMehdiBelum ada peringkat

- Deepa 2Dokumen13 halamanDeepa 2FarhanChowdhuryMehdiBelum ada peringkat

- ReportDokumen92 halamanReportFarhanChowdhuryMehdiBelum ada peringkat

- Class Routine For CSE DAY Spring-2017Dokumen8 halamanClass Routine For CSE DAY Spring-2017FarhanChowdhuryMehdiBelum ada peringkat

- Pu1473410272 PDFDokumen1 halamanPu1473410272 PDFFarhanChowdhuryMehdiBelum ada peringkat

- Govt Hospitals ResearchDokumen2 halamanGovt Hospitals ResearchFarhanChowdhuryMehdiBelum ada peringkat

- ISA 240 Is in Respect of Auditor's Responsibility To Consider Fraud Is An Audit ofDokumen12 halamanISA 240 Is in Respect of Auditor's Responsibility To Consider Fraud Is An Audit ofFarhanChowdhuryMehdiBelum ada peringkat

- SBI Bangladesh Trainee Assistant Officer Application FormDokumen4 halamanSBI Bangladesh Trainee Assistant Officer Application FormFarhanChowdhuryMehdiBelum ada peringkat

- Audit Report TypesDokumen5 halamanAudit Report TypesFarhanChowdhuryMehdiBelum ada peringkat

- Lecture20-Z Buffer PipelineDokumen35 halamanLecture20-Z Buffer PipelineFarhanChowdhuryMehdiBelum ada peringkat

- 2016 Summer Courses - Print RoutinehjDokumen6 halaman2016 Summer Courses - Print RoutinehjFarhanChowdhuryMehdiBelum ada peringkat

- Audit definition, fraud characteristics, and audit planningDokumen6 halamanAudit definition, fraud characteristics, and audit planningFarhanChowdhuryMehdiBelum ada peringkat

- Particulars Amount (TK) Amount (TK) Fixed Assets:: Balance SheetDokumen1 halamanParticulars Amount (TK) Amount (TK) Fixed Assets:: Balance SheetFarhanChowdhuryMehdiBelum ada peringkat

- CV TITLEDokumen10 halamanCV TITLEMd. Rezaul KarimBelum ada peringkat

- Exam on beach animalsDokumen6 halamanExam on beach animalsFarhanChowdhuryMehdiBelum ada peringkat

- AIS role in value chain and e-business effectsDokumen4 halamanAIS role in value chain and e-business effectsFarhanChowdhuryMehdiBelum ada peringkat

- Curriculum Vitae CV TemplatesDokumen6 halamanCurriculum Vitae CV TemplatesVeronica GeorgeBelum ada peringkat

- Nature of Ihrm & Strategic Ihrm: Jyoti Rekha Divya Ragendran Annie Thomas Nimmy Jose Priyanka G Shruthi S.PDokumen82 halamanNature of Ihrm & Strategic Ihrm: Jyoti Rekha Divya Ragendran Annie Thomas Nimmy Jose Priyanka G Shruthi S.PPreethi KrishnanBelum ada peringkat

- Lista Participanti SEAPDokumen648 halamanLista Participanti SEAPEusebiu IonescuBelum ada peringkat

- MIC Tanzania Supplier QuestionnaireDokumen11 halamanMIC Tanzania Supplier QuestionnaireBahati ValerianBelum ada peringkat

- AMFI Test Practice Questions for Mutual Fund ProfessionalsDokumen57 halamanAMFI Test Practice Questions for Mutual Fund ProfessionalsRanjana TrivediBelum ada peringkat

- Stock - Questionnaire For Internal ControlDokumen3 halamanStock - Questionnaire For Internal ControlBindu RaoBelum ada peringkat

- Inter-Firm ComparisonDokumen5 halamanInter-Firm Comparisonanon_672065362100% (1)

- Amendments Toc A 1965Dokumen260 halamanAmendments Toc A 1965NuHar MisranBelum ada peringkat

- Tourism Industry BreakdownDokumen4 halamanTourism Industry BreakdownAira Lonto100% (1)

- DBar Inc. Corporate BrandingDokumen73 halamanDBar Inc. Corporate Brandingshahna gargBelum ada peringkat

- Bharti's Easyday Retail Strategy and OperationsDokumen22 halamanBharti's Easyday Retail Strategy and OperationsNishant TyagiBelum ada peringkat

- BACH database overviewDokumen2 halamanBACH database overviewpaul_costasBelum ada peringkat

- DocumentDokumen2 halamanDocumentNorelkis Thais Perez ArangurenBelum ada peringkat

- Corporate Profile of Multimode GroupDokumen6 halamanCorporate Profile of Multimode GroupShaheen RahmanBelum ada peringkat

- Harga Mesin Jahit Typical:: Juki DDL 8100eDokumen2 halamanHarga Mesin Jahit Typical:: Juki DDL 8100eRismapleBelum ada peringkat

- CAG Report 2012/2013 - TanzaniaDokumen206 halamanCAG Report 2012/2013 - TanzaniaMaria Sarungi-TsehaiBelum ada peringkat

- Discounts For DCPS Teachers May 2014Dokumen4 halamanDiscounts For DCPS Teachers May 2014DC Public SchoolsBelum ada peringkat

- Company Accounting - Powerpoint PresentationDokumen29 halamanCompany Accounting - Powerpoint Presentationtammy_yau3199100% (1)

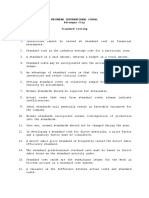

- Assignment 3 - Standard CostingDokumen4 halamanAssignment 3 - Standard CostingJayhan PalmonesBelum ada peringkat

- Chief Operating Officer in NYC Resume William HoganDokumen3 halamanChief Operating Officer in NYC Resume William HoganWilliamHoganBelum ada peringkat

- Gaming Final Report PDFDokumen250 halamanGaming Final Report PDFbhpliaoBelum ada peringkat