Anda mungkin juga menyukai

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Bpi vs. Yujuico (2015)Dokumen3 halamanBpi vs. Yujuico (2015)XyraKrezelGajeteBelum ada peringkat

- CIR Vs FisherDokumen61 halamanCIR Vs FisherXyraKrezelGajeteBelum ada peringkat

- Transcribe Notes Civil CodeDokumen4 halamanTranscribe Notes Civil CodeXyraKrezelGajeteBelum ada peringkat

- Steelcase, Inc. v. Design International Selections, Inc. (DISI) DigestDokumen4 halamanSteelcase, Inc. v. Design International Selections, Inc. (DISI) DigestXyraKrezelGajeteBelum ada peringkat

- GREGORIO PESTAÑO Vs SumayangDokumen54 halamanGREGORIO PESTAÑO Vs SumayangXyraKrezelGajeteBelum ada peringkat

- People Vs VillaricoDokumen4 halamanPeople Vs VillaricoXyraKrezelGajeteBelum ada peringkat

- Asia Vest Vs CADokumen27 halamanAsia Vest Vs CAXyraKrezelGajete100% (1)

- Pimentel Vs ComelecDokumen2 halamanPimentel Vs ComelecXyraKrezelGajete100% (2)

- Vda de Chua Vs CADokumen8 halamanVda de Chua Vs CAXyraKrezelGajeteBelum ada peringkat

- Tribiana Vs TribianaDokumen2 halamanTribiana Vs TribianaXyraKrezelGajeteBelum ada peringkat

- People Vs Lo Ho WingDokumen2 halamanPeople Vs Lo Ho WingXyraKrezelGajeteBelum ada peringkat

- BPI Vs CA DigestDokumen2 halamanBPI Vs CA DigestXyraKrezelGajeteBelum ada peringkat

- Corona Vs United Harbor PilotsDokumen2 halamanCorona Vs United Harbor PilotsXyraKrezelGajete0% (1)

- Arrow Transportation vs. Board of TransportationDokumen1 halamanArrow Transportation vs. Board of TransportationXyraKrezelGajeteBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- KBA - Accounting and BookkeepingDokumen8 halamanKBA - Accounting and BookkeepingKBA Accounting & Bookkeeping Services LLCBelum ada peringkat

- Badillo vs. Court of Appeals, 555 SCRA 435 (2008) - FulltextDokumen7 halamanBadillo vs. Court of Appeals, 555 SCRA 435 (2008) - FulltextNyla0% (1)

- Catholic Social Teaching & Its Key Principles: Sandie CornishDokumen27 halamanCatholic Social Teaching & Its Key Principles: Sandie Cornishportiadeportia100% (1)

- SPA - SampleDokumen2 halamanSPA - SampleAP GeotinaBelum ada peringkat

- UncitralDokumen16 halamanUncitralRubz JeanBelum ada peringkat

- ViolenceAgainstChildren by SOS Children VillagesDokumen44 halamanViolenceAgainstChildren by SOS Children VillagessofiabloemBelum ada peringkat

- SPIDokumen3 halamanSPIMichael EalaBelum ada peringkat

- Improve Your Word Power: Quick Test-1 Quick Test-3Dokumen1 halamanImprove Your Word Power: Quick Test-1 Quick Test-3Bugga Venkata Shanmukha SaiBelum ada peringkat

- Pleasantville:: An Existential Communication JourneyDokumen16 halamanPleasantville:: An Existential Communication JourneyFred StevensonBelum ada peringkat

- Draft PrintDokumen3 halamanDraft Printsumanth sharmaBelum ada peringkat

- Bay Al InahDokumen12 halamanBay Al InahAyu SetzianiBelum ada peringkat

- Air France vs. CarrascosoDokumen5 halamanAir France vs. CarrascosoMj BrionesBelum ada peringkat

- Goldenberg CaseDokumen3 halamanGoldenberg CaseFriendship GoalBelum ada peringkat

- Public Records Request Response From Santa Maria PD OnDokumen6 halamanPublic Records Request Response From Santa Maria PD OnDave MinskyBelum ada peringkat

- Counter Affidavit - Ernani Villazor1Dokumen8 halamanCounter Affidavit - Ernani Villazor1Maximo IsidroBelum ada peringkat

- Pepsi CoDokumen3 halamanPepsi CoCH Hanzala AmjadBelum ada peringkat

- Defences TortDokumen52 halamanDefences Tortspecies09Belum ada peringkat

- Art 171-172PRCDokumen2 halamanArt 171-172PRCDan SilBelum ada peringkat

- GhararDokumen5 halamanGhararSiti Naquiah Mohd JamelBelum ada peringkat

- Laguna State Polytechnic University: College ofDokumen12 halamanLaguna State Polytechnic University: College ofCharlyne Mari FloresBelum ada peringkat

- Law Entrance Exam: Mock Test 04Dokumen29 halamanLaw Entrance Exam: Mock Test 04Nikunj VatsBelum ada peringkat

- Sop Informed ConsentDokumen4 halamanSop Informed ConsentWelzha Meturan-kadmaerubunBelum ada peringkat

- Group Dynamics 1Dokumen12 halamanGroup Dynamics 1Varun Lalwani100% (2)

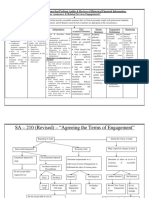

- 53 Standards On Auditing Flowcharts PDFDokumen22 halaman53 Standards On Auditing Flowcharts PDFSaloni100% (1)

- DLL For PhiloDokumen11 halamanDLL For Philosmhilez100% (1)

- Chap. 1 Strategic Vision, Mission and ObjectivesDokumen38 halamanChap. 1 Strategic Vision, Mission and ObjectivesOjantaBelum ada peringkat

- Delizo Until EmbradoDokumen86 halamanDelizo Until EmbradoValerie San MiguelBelum ada peringkat

- Legal Profession Reviewer MidtermsDokumen9 halamanLegal Profession Reviewer MidtermsShasharu Fei-fei LimBelum ada peringkat

- Dudjoms Prayer For Recognising Faults 2 PDFDokumen22 halamanDudjoms Prayer For Recognising Faults 2 PDFThiagoFerrettiBelum ada peringkat

- Gendron 2005Dokumen38 halamanGendron 2005Daniel WambuaBelum ada peringkat