Anda mungkin juga menyukai

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionDari EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionBelum ada peringkat

- SolutionChapter5 1Dokumen20 halamanSolutionChapter5 1Jan Reynan CadienteBelum ada peringkat

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionDari EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionBelum ada peringkat

- Adv Acc Chapter4Dokumen13 halamanAdv Acc Chapter4Reanne Claudine LagunaBelum ada peringkat

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionDari EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionBelum ada peringkat

- Answer Key TP PrefiDokumen2 halamanAnswer Key TP PrefiveriBelum ada peringkat

- Public Financial Management Systems—Indonesia: Key Elements from a Financial Management PerspectiveDari EverandPublic Financial Management Systems—Indonesia: Key Elements from a Financial Management PerspectivePenilaian: 5 dari 5 bintang5/5 (1)

- Dayag Chapter 4Dokumen17 halamanDayag Chapter 4Clifford Angel Matias71% (7)

- Aid for Trade in Asia and the Pacific: Promoting Connectivity for Inclusive DevelopmentDari EverandAid for Trade in Asia and the Pacific: Promoting Connectivity for Inclusive DevelopmentBelum ada peringkat

- Solution Chapter 4Dokumen14 halamanSolution Chapter 4Roselle Manlapaz Lorenzo100% (1)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionDari EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionBelum ada peringkat

- Accounting AssignmentDokumen16 halamanAccounting AssignmentMIKASABelum ada peringkat

- Strengthening Functional Urban Regions in Azerbaijan: National Urban Assessment 2017Dari EverandStrengthening Functional Urban Regions in Azerbaijan: National Urban Assessment 2017Belum ada peringkat

- Solution Chapter 5Dokumen22 halamanSolution Chapter 5Teresa GonzalesBelum ada peringkat

- Credit Union Revenues World Summary: Market Values & Financials by CountryDari EverandCredit Union Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Solution Chapter 5Dokumen22 halamanSolution Chapter 5Roselle Manlapaz LorenzoBelum ada peringkat

- Wiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsDari EverandWiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsBelum ada peringkat

- Chapter 5 Installment LiquidationDokumen25 halamanChapter 5 Installment LiquidationApple Jane Galisa Secula0% (2)

- Secondary Market Financing Revenues World Summary: Market Values & Financials by CountryDari EverandSecondary Market Financing Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Financial Accounting Suggested AnswersDokumen6 halamanFinancial Accounting Suggested Answersaqsa_22inBelum ada peringkat

- Economic Indicators for East Asia: Input–Output TablesDari EverandEconomic Indicators for East Asia: Input–Output TablesBelum ada peringkat

- Chapter 19 - Consol. Fs Part 4Dokumen17 halamanChapter 19 - Consol. Fs Part 4PutmehudgJasdBelum ada peringkat

- Small Money Big Impact: Fighting Poverty with MicrofinanceDari EverandSmall Money Big Impact: Fighting Poverty with MicrofinanceBelum ada peringkat

- Solution Chapter 5Dokumen22 halamanSolution Chapter 5ashleyBelum ada peringkat

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryDari EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Partnership Loss Realization Deficit Capital AccountsDokumen12 halamanPartnership Loss Realization Deficit Capital AccountsClarize R. Mabiog100% (2)

- Dayag - Chapter 5 PDFDokumen25 halamanDayag - Chapter 5 PDFKen ZafraBelum ada peringkat

- Sol. Man. Chapter 4 Partnership Liquidation 2020 EditionDokumen30 halamanSol. Man. Chapter 4 Partnership Liquidation 2020 EditionJennifer RelosoBelum ada peringkat

- Quiz Chapter7Dokumen3 halamanQuiz Chapter7Christine Jane RamosBelum ada peringkat

- Ratio AnalysisDokumen11 halamanRatio Analysisbhatriyan606Belum ada peringkat

- Accountancy Subject Code 30Dokumen14 halamanAccountancy Subject Code 30Praveen HaridasBelum ada peringkat

- Ruiz, Eric Gerard D.: Problem IDokumen9 halamanRuiz, Eric Gerard D.: Problem IMyAccntBelum ada peringkat

- Marking Scheme: Section ADokumen8 halamanMarking Scheme: Section Aaegean123Belum ada peringkat

- City of Windsor Capital Budget Documents For 2013.Dokumen362 halamanCity of Windsor Capital Budget Documents For 2013.windsorstarBelum ada peringkat

- Advanced Accounting CH 14, 15Dokumen16 halamanAdvanced Accounting CH 14, 15jessicaBelum ada peringkat

- Case Study 2022 FallDokumen3 halamanCase Study 2022 FallAppleDugarBelum ada peringkat

- Previous Year Question Paper (FSA)Dokumen16 halamanPrevious Year Question Paper (FSA)Alisha ShawBelum ada peringkat

- Solved ProblemsDokumen75 halamanSolved Problemsgut78Belum ada peringkat

- Quiz 1 partnership accounting problems and solutionsDokumen4 halamanQuiz 1 partnership accounting problems and solutionsdianel villarico100% (2)

- Module 15Dokumen3 halamanModule 15Jhon Ferdlee Bahandi BenitezBelum ada peringkat

- Quiz - Chapter 4 - Partnership Liquidation - 2021 EditionDokumen7 halamanQuiz - Chapter 4 - Partnership Liquidation - 2021 EditionYam SondayBelum ada peringkat

- Advanced Accounts Revision Notes by Jai Chawla Sir PDFDokumen100 halamanAdvanced Accounts Revision Notes by Jai Chawla Sir PDFRaghavendra PrasadBelum ada peringkat

- Maine Department Store Financial StatementsRef Debit Credit201 15001201500120 10001011000112 25004012500505 12001201200201 300120300120 20001012000Dokumen63 halamanMaine Department Store Financial StatementsRef Debit Credit201 15001201500120 10001011000112 25004012500505 12001201200201 300120300120 20001012000Protibibadi0% (1)

- CH 16Dokumen8 halamanCH 16Lex HerzhelBelum ada peringkat

- AnswersDokumen8 halamanAnswersTareq ChowdhuryBelum ada peringkat

- Partnership Liquidation Chapter 4 QuizDokumen3 halamanPartnership Liquidation Chapter 4 QuizKimberly Quin CañasBelum ada peringkat

- SophisticatesDokumen3 halamanSophisticatesLuis Melquiades P. GarciaBelum ada peringkat

- Adg8kk1) r8 Fq7''uDokumen6 halamanAdg8kk1) r8 Fq7''uThe makas AbababaBelum ada peringkat

- B.B.A., Sem.-IV CC-213: Corporate Financial StatementsDokumen4 halamanB.B.A., Sem.-IV CC-213: Corporate Financial StatementsJJ NayakBelum ada peringkat

- 04 Partnership LiquidationDokumen10 halaman04 Partnership LiquidationRoland jamesBelum ada peringkat

- PROBLEM 7 Solution AFAR1 - DonggoDokumen4 halamanPROBLEM 7 Solution AFAR1 - DonggoArj Sulit Centino DaquiBelum ada peringkat

- Consolidated Financial StatementsDokumen78 halamanConsolidated Financial StatementsAbid HussainBelum ada peringkat

- AP 59 FinPB - 5.06Dokumen8 halamanAP 59 FinPB - 5.06Anonymous Lih1laaxBelum ada peringkat

- LiquidationDokumen18 halamanLiquidationSamaica MontemayorBelum ada peringkat

- BusscomDokumen3 halamanBusscomneo14Belum ada peringkat

- Module 1 Assignment 2AAC Feb 2023Dokumen4 halamanModule 1 Assignment 2AAC Feb 2023Lorifel Antonette Laoreno TejeroBelum ada peringkat

- Acctg13 Midterm Exam TQ 2021 2022 2nd SemDokumen6 halamanAcctg13 Midterm Exam TQ 2021 2022 2nd SemGarp BarrocaBelum ada peringkat

- CH 14Dokumen6 halamanCH 14Aminul Haque RusselBelum ada peringkat

- 4 ModelDokumen3 halaman4 ModelnrellasBelum ada peringkat

- Tools of Financial Analysis & PlanningDokumen68 halamanTools of Financial Analysis & Planninganon_672065362100% (1)

- Research Study ArlynDokumen10 halamanResearch Study ArlynKunal SajnaniBelum ada peringkat

- Star BurnDokumen1 halamanStar BurnKunal SajnaniBelum ada peringkat

- Read MeDokumen1 halamanRead MeDiego HlchBelum ada peringkat

- Chapter2 ThesisDokumen17 halamanChapter2 ThesisJoe Yuan Julian Mambu67% (3)

- Toshiba CEO Resigns Over $1.2B Accounting ScandalDokumen4 halamanToshiba CEO Resigns Over $1.2B Accounting ScandalKunal SajnaniBelum ada peringkat

- Rubie Research StudyDokumen12 halamanRubie Research StudyKunal SajnaniBelum ada peringkat

- What Should Mr. Oberoi's Objective/target Be?: Specific Format For Accounting - Target To Be AchievedDokumen5 halamanWhat Should Mr. Oberoi's Objective/target Be?: Specific Format For Accounting - Target To Be AchievedKunal SajnaniBelum ada peringkat

- Accounting Transactions - Effect On The Fundamental Accounting EquationDokumen6 halamanAccounting Transactions - Effect On The Fundamental Accounting EquationKunal SajnaniBelum ada peringkat

- Business: Learn Accounting Through An ExampleDokumen6 halamanBusiness: Learn Accounting Through An ExampleKunal SajnaniBelum ada peringkat

- Day ThreeDokumen10 halamanDay ThreeKunal SajnaniBelum ada peringkat

- Work Immersion CGDokumen4 halamanWork Immersion CGαλβιν δε100% (16)

- Relevant Costing CPARDokumen13 halamanRelevant Costing CPARxxxxxxxxx100% (2)

- Tardiness in Relation To The Academic PeDokumen12 halamanTardiness in Relation To The Academic PeKunal Sajnani100% (1)

- Work Immersion PortfolioDokumen1 halamanWork Immersion PortfolioKunal SajnaniBelum ada peringkat

- Complete FsDokumen4 halamanComplete FsKunal SajnaniBelum ada peringkat

- Synthesis FraudDokumen3 halamanSynthesis FraudKunal SajnaniBelum ada peringkat

- BL 4 Reviewer LectureDokumen16 halamanBL 4 Reviewer LectureAleshanee Pearl Yavin-Cruz Knights-SchneiderBelum ada peringkat

- Case Study in MGT 4Dokumen4 halamanCase Study in MGT 4Kunal Sajnani100% (1)

- Book 1Dokumen4 halamanBook 1Kunal SajnaniBelum ada peringkat

- Web Developer App Letter SpinDokumen1 halamanWeb Developer App Letter SpinKunal SajnaniBelum ada peringkat

- Quantitative Techniques For BusinessDokumen142 halamanQuantitative Techniques For BusinessJudy Ann Paulan100% (1)

- Corp Reviewer - LadiaDokumen87 halamanCorp Reviewer - Ladiadpante100% (6)

- Ch09 - Statistical Sampling For Testing Control ProceduresDokumen19 halamanCh09 - Statistical Sampling For Testing Control Proceduresrain06021992100% (2)

- ch08 - Internal Control and Computer Based InformationDokumen23 halamanch08 - Internal Control and Computer Based InformationMJ YaconBelum ada peringkat

- Corporation Code of The Phils Batas Pambansa 68 PDFDokumen23 halamanCorporation Code of The Phils Batas Pambansa 68 PDFKunal SajnaniBelum ada peringkat

- CHAPTER 3 - RESEARCH METHODOLOGY: Data Collection Method and Research ToolsDokumen10 halamanCHAPTER 3 - RESEARCH METHODOLOGY: Data Collection Method and Research ToolsjeyemgiBelum ada peringkat

- The Two Blind MenDokumen6 halamanThe Two Blind MenKunal SajnaniBelum ada peringkat

- Philippines Corporation Code-1 PDFDokumen68 halamanPhilippines Corporation Code-1 PDFKunal SajnaniBelum ada peringkat

- ch08 - Internal Control and Computer Based InformationDokumen23 halamanch08 - Internal Control and Computer Based InformationMJ YaconBelum ada peringkat

- Partcor Reviewer PDFDokumen26 halamanPartcor Reviewer PDFKunal Sajnani100% (1)

- Multiple Choice. (Write Your Answers Before The Number. Use Capital Letter.)Dokumen4 halamanMultiple Choice. (Write Your Answers Before The Number. Use Capital Letter.)april bentadanBelum ada peringkat

- Lone Pine Cafe-CaseDokumen28 halamanLone Pine Cafe-CaseNadya Rizkita100% (2)

- 02-FI-02 - SDD - MSRDC - VBSL - Funds Creation Allocation - V1Dokumen13 halaman02-FI-02 - SDD - MSRDC - VBSL - Funds Creation Allocation - V1DanielpremassisBelum ada peringkat

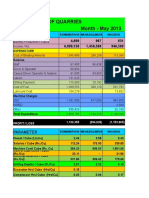

- Production of QuarriesDokumen114 halamanProduction of QuarriesSarinBelum ada peringkat

- LLP Form No. 8: Statement of Account & SolvencyDokumen5 halamanLLP Form No. 8: Statement of Account & SolvencyPadmini VasanthBelum ada peringkat

- Ratio Analysis Mapple Leaf & BestWay CementDokumen46 halamanRatio Analysis Mapple Leaf & BestWay CementUmer RashidBelum ada peringkat

- Chapter 15 PDFDokumen29 halamanChapter 15 PDFKimBelum ada peringkat

- SOCEBSKE2023 SERStatementof Expenseson Public RallyDokumen1 halamanSOCEBSKE2023 SERStatementof Expenseson Public Rallypmii.ldelcarmenBelum ada peringkat

- Part I Accounts QuestionDokumen11 halamanPart I Accounts QuestionAMIN BUHARI ABDUL KHADERBelum ada peringkat

- 2nd Quarter Exam-1Dokumen7 halaman2nd Quarter Exam-1Alona Nay Calumpit AgcaoiliBelum ada peringkat

- Trust Deed FormatDokumen12 halamanTrust Deed Formatprashant kapilBelum ada peringkat

- SAP Localization TurkeyDokumen30 halamanSAP Localization TurkeybenhzbBelum ada peringkat

- Fundamentals ActivitiesDokumen9 halamanFundamentals ActivitiesCris TineBelum ada peringkat

- Financial Plan Paper 1Dokumen12 halamanFinancial Plan Paper 1Samuel Grant ZabalaBelum ada peringkat

- Prepare statement of cash flow using direct methodDokumen2 halamanPrepare statement of cash flow using direct methodIrfan ghaniBelum ada peringkat

- CA Found. Accounts Book M-I & II English BookDokumen205 halamanCA Found. Accounts Book M-I & II English BookRaghav Somani100% (1)

- Chart of AccountsDokumen6 halamanChart of AccountsJenniferBelum ada peringkat

- RA 6615 Requires Emergency Medical AssistanceDokumen2 halamanRA 6615 Requires Emergency Medical AssistanceFides ServandaBelum ada peringkat

- Business Visitor - VAF1C - FormDokumen11 halamanBusiness Visitor - VAF1C - FormChindu Mathew KuruvillaBelum ada peringkat

- Restaurant MirchiDokumen32 halamanRestaurant MirchiDavidChenBelum ada peringkat

- AuditingDokumen21 halamanAuditingShilpan ShahBelum ada peringkat

- ACC 100 - Introduction To AccountingDokumen10 halamanACC 100 - Introduction To AccountingDevanand RamnarineBelum ada peringkat

- Cost Allocation Plans and Indirect Cost Rates GuideDokumen39 halamanCost Allocation Plans and Indirect Cost Rates GuideRitesh RamanBelum ada peringkat

- Prepaid ExpenseDokumen4 halamanPrepaid ExpenseEhsan Umer FarooqiBelum ada peringkat

- Projected Cash Flow Statement in ExcelDokumen19 halamanProjected Cash Flow Statement in ExcelfarshidianBelum ada peringkat

- Solutions To Problems: Pe On Estate TaxDokumen11 halamanSolutions To Problems: Pe On Estate TaxErica NicolasuraBelum ada peringkat

- SS 07 Quiz 2 - AnswersDokumen130 halamanSS 07 Quiz 2 - AnswersVan Le Ha100% (1)

- GROUP ASSIGNMENTDokumen12 halamanGROUP ASSIGNMENTAn Phan Thị HoàiBelum ada peringkat

- Final ReviewDokumen44 halamanFinal Reviewnidal charaf eddine50% (2)

- A191 Toturial 7 AnswersheetDokumen7 halamanA191 Toturial 7 AnswersheetMan yeeBelum ada peringkat