Anda mungkin juga menyukai

- CCP Ordinance 2009Dokumen33 halamanCCP Ordinance 2009Farukh NaveedBelum ada peringkat

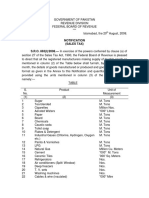

- 2008sro863 - Special ReturnDokumen2 halaman2008sro863 - Special ReturnFarukh NaveedBelum ada peringkat

- DGC Khan Cement Cost Audit Report 2007-2008Dokumen49 halamanDGC Khan Cement Cost Audit Report 2007-2008Farukh NaveedBelum ada peringkat

- Implementation of Microsoft GP 2010Dokumen2 halamanImplementation of Microsoft GP 2010Farukh NaveedBelum ada peringkat

- T I C A P: Final Examinations Winter 2007Dokumen2 halamanT I C A P: Final Examinations Winter 2007Farukh NaveedBelum ada peringkat

- PF Trust DocumentDokumen62 halamanPF Trust DocumentFarukh NaveedBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Introduction To Green Economy Syllabus PDFDokumen13 halamanIntroduction To Green Economy Syllabus PDFNatalia Lara100% (1)

- Accenture The Process of Process ManagementDokumen12 halamanAccenture The Process of Process ManagementTomas JeffersonBelum ada peringkat

- Tourism and Biodiversity - Mapping Tourism's Global FootprintDokumen66 halamanTourism and Biodiversity - Mapping Tourism's Global FootprintInnovaPeruConsultingBelum ada peringkat

- Tier Standard-Operational-Sustainabilitypdf PDFDokumen17 halamanTier Standard-Operational-Sustainabilitypdf PDFPanos Cayafas100% (1)

- Micromobility White Paper-ENDokumen62 halamanMicromobility White Paper-ENSid100% (1)

- CORPORATE SOCIAL RESPONSABILITY - FINAL EXAM ( Click Here) - Revisión Del IntentoDokumen6 halamanCORPORATE SOCIAL RESPONSABILITY - FINAL EXAM ( Click Here) - Revisión Del IntentoAntonella Rondon TantaBelum ada peringkat

- Living in The IT Era Prelims (28 - 30)Dokumen3 halamanLiving in The IT Era Prelims (28 - 30)Mark Errol75% (4)

- Aerospace NDTDokumen7 halamanAerospace NDTSAI JITHENDRA GONJIBelum ada peringkat

- Community Service Guideline Harmonized Final - BDU 2Dokumen77 halamanCommunity Service Guideline Harmonized Final - BDU 2Abera Ayalew100% (1)

- Quiz 1 - FinalDokumen3 halamanQuiz 1 - FinalMohamed AboustitBelum ada peringkat

- Environmental Law NotesDokumen37 halamanEnvironmental Law NotesAkhil SomanBelum ada peringkat

- Detailed Life Cycle Assessment of Bounty Paper Towel - 2016 - Journal of CleaneDokumen14 halamanDetailed Life Cycle Assessment of Bounty Paper Towel - 2016 - Journal of CleanePrashant GaradBelum ada peringkat

- Globalization and The Challenges of Public Administration Governance by Globalization and The Challenges of Public Administration GovernanceDokumen10 halamanGlobalization and The Challenges of Public Administration Governance by Globalization and The Challenges of Public Administration Governancevivek kumar singhBelum ada peringkat

- 2018 Integrated Annual Report BbvaDokumen628 halaman2018 Integrated Annual Report BbvaedgarmerchanBelum ada peringkat

- Food Security Food Justice or Food SovereigntyDokumen4 halamanFood Security Food Justice or Food SovereigntyEric Holt-GimenezBelum ada peringkat

- Modern Energy Services For Health Facilities in Resource-Constrained Settings WHO ReportDokumen104 halamanModern Energy Services For Health Facilities in Resource-Constrained Settings WHO ReportKelvin FuBelum ada peringkat

- Journal of Cleaner Production: Wim Lambrechts, Ingrid Mulà, Kim Ceulemans, Ingrid Molderez, Veerle GaeremynckDokumen9 halamanJournal of Cleaner Production: Wim Lambrechts, Ingrid Mulà, Kim Ceulemans, Ingrid Molderez, Veerle Gaeremynckairish21081501Belum ada peringkat

- Press Release Moe Objection LetterDokumen3 halamanPress Release Moe Objection LetterSTOP THE QUARRYBelum ada peringkat

- Stiftungsbroschuere Bayer Engl Ansicht 2Dokumen48 halamanStiftungsbroschuere Bayer Engl Ansicht 2RezaNoegrahaBelum ada peringkat

- Peace Education Grade 4Dokumen50 halamanPeace Education Grade 4Sto. Rosario ES (R III - Pampanga)Belum ada peringkat

- Article Sample IOPDokumen9 halamanArticle Sample IOPGilang BuditamaBelum ada peringkat

- National Rural Housing and Habitat PolicyDokumen15 halamanNational Rural Housing and Habitat PolicyBasim AhmedBelum ada peringkat

- Sustainable Biomaterials and Their Applications - A Short ReviewDokumen9 halamanSustainable Biomaterials and Their Applications - A Short ReviewvalentinaBelum ada peringkat

- Green Mark Resi v4.1Dokumen13 halamanGreen Mark Resi v4.1Suresh DBelum ada peringkat

- Host City Cape Town Green Goal Action Plan (PDF) V - 1 PDFDokumen63 halamanHost City Cape Town Green Goal Action Plan (PDF) V - 1 PDFKifle mandefroBelum ada peringkat

- GRI 3 Material Topics 2021Dokumen30 halamanGRI 3 Material Topics 2021Alfita PutrimasiBelum ada peringkat

- National Strategy For Eco TourismDokumen26 halamanNational Strategy For Eco TourismSahilBelum ada peringkat

- Huntsville Official Plan March 2020Dokumen252 halamanHuntsville Official Plan March 2020Taylor BellBelum ada peringkat

- Format For Thesis Approval BarchDokumen2 halamanFormat For Thesis Approval BarchyazBelum ada peringkat

- Captain GopinathDokumen7 halamanCaptain GopinathanshulleoBelum ada peringkat