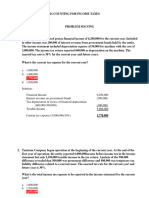

Anda mungkin juga menyukai

- ACT150 Assignment DIMAAMPAODokumen4 halamanACT150 Assignment DIMAAMPAOJeromeBelum ada peringkat

- Exercises IAS 8 SolutionDokumen5 halamanExercises IAS 8 SolutionLê Xuân HồBelum ada peringkat

- Tutorial 2: Exercise 12.2 Calculation of Current TaxDokumen13 halamanTutorial 2: Exercise 12.2 Calculation of Current TaxKim FloresBelum ada peringkat

- EXAMPLE 12.1 (Current Tax Liability)Dokumen8 halamanEXAMPLE 12.1 (Current Tax Liability)KaiWenNgBelum ada peringkat

- AnswersDokumen8 halamanAnswersTareq ChowdhuryBelum ada peringkat

- HI5020 Tutorial Question Assignment T3 2020 FinalDokumen7 halamanHI5020 Tutorial Question Assignment T3 2020 FinalAamirBelum ada peringkat

- T01 - Income Tax QuestionsDokumen7 halamanT01 - Income Tax QuestionsLijing CheBelum ada peringkat

- Answers To Week 1 HomeworkDokumen6 halamanAnswers To Week 1 Homeworkmzvette234Belum ada peringkat

- Special Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureDokumen4 halamanSpecial Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureNoorodden50% (2)

- ACC108 - Tutorial 13-14Dokumen40 halamanACC108 - Tutorial 13-14Shivati Singh KahlonBelum ada peringkat

- Seminar 12.2 Outline - Auditing of Group Financial Statements IIDokumen6 halamanSeminar 12.2 Outline - Auditing of Group Financial Statements IIJasmine TayBelum ada peringkat

- 01 Audit of Income Tax Exercise SetDokumen2 halaman01 Audit of Income Tax Exercise SetBecky GonzagaBelum ada peringkat

- Financial Statements PreparationDokumen6 halamanFinancial Statements Preparationana lopezBelum ada peringkat

- Lamagan, Kyla T. BSA 401 Intermediate Acct. 2 Final Output Problem 16-13 (IAA)Dokumen14 halamanLamagan, Kyla T. BSA 401 Intermediate Acct. 2 Final Output Problem 16-13 (IAA)lana del reyBelum ada peringkat

- Quiz 2 - Finals - Cash Flow Statement-Intermediate Accounting 3Dokumen3 halamanQuiz 2 - Finals - Cash Flow Statement-Intermediate Accounting 3kanroji1923Belum ada peringkat

- Solutions Chapter 23Dokumen11 halamanSolutions Chapter 23Avi SeligBelum ada peringkat

- Problems Accouting For Deferred Taxes Webinar ReoDokumen7 halamanProblems Accouting For Deferred Taxes Webinar ReocrookshanksBelum ada peringkat

- 06 Taxation - Deferred s20 Final-1Dokumen44 halaman06 Taxation - Deferred s20 Final-150902849Belum ada peringkat

- Special Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureDokumen5 halamanSpecial Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureClarisse AlimotBelum ada peringkat

- Financial Accounting ProjectDokumen9 halamanFinancial Accounting ProjectL.a. LadoresBelum ada peringkat

- Income Statement: Format: Single Step: List All Revenues and SubtotalDokumen2 halamanIncome Statement: Format: Single Step: List All Revenues and SubtotalRabia RabiaBelum ada peringkat

- Mpu3123 Titas c2Dokumen36 halamanMpu3123 Titas c2Beatrice Tan100% (2)

- Answers Quiz Chapter 4Dokumen4 halamanAnswers Quiz Chapter 4Anthony MartinezBelum ada peringkat

- Activity 1 Calculations Using The Tax-Payable MethodDokumen10 halamanActivity 1 Calculations Using The Tax-Payable MethodJohn TomBelum ada peringkat

- CFS Company Has The Following Details For Two-Year Period, 2019 and 2018Dokumen7 halamanCFS Company Has The Following Details For Two-Year Period, 2019 and 2018MiconBelum ada peringkat

- Faisal WorksheetDokumen5 halamanFaisal WorksheetAbdul MateenBelum ada peringkat

- Accounting CycleDokumen5 halamanAccounting Cycleruth san jose100% (1)

- Chapter #1 Tutorial Class: Faculty of Economics and Administration Accounting Department ACCT 117Dokumen47 halamanChapter #1 Tutorial Class: Faculty of Economics and Administration Accounting Department ACCT 117hazem 00Belum ada peringkat

- FABM 210 Fundamentals of Accounting Part 2: Lyceum-Northwestern UniversityDokumen10 halamanFABM 210 Fundamentals of Accounting Part 2: Lyceum-Northwestern UniversityAmie Jane MirandaBelum ada peringkat

- Exercises cms-3: 1. ABC Corporation Has Developed The Following Standards For One of Its ProductsDokumen2 halamanExercises cms-3: 1. ABC Corporation Has Developed The Following Standards For One of Its ProductsThaa Manitha DinataBelum ada peringkat

- Practice QuestionsDokumen19 halamanPractice QuestionsAbdul Qayyum Qayyum0% (2)

- Sample Financial Management ProblemsDokumen8 halamanSample Financial Management ProblemsJasper Andrew AdjaraniBelum ada peringkat

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDokumen7 halamanAccounting For Managers (Assignment One (E-Finance) ) Question OnehananBelum ada peringkat

- Interim Financial Reporting and Operating Segment Discussion Problems and Answer KeyDokumen4 halamanInterim Financial Reporting and Operating Segment Discussion Problems and Answer Keyprincess QBelum ada peringkat

- Income TaxesDokumen3 halamanIncome TaxesCENTENO, JOAN R.Belum ada peringkat

- F7 - IPRO - Mock 1 - AnswersDokumen14 halamanF7 - IPRO - Mock 1 - AnswerspavishneBelum ada peringkat

- Solutions Ch07Dokumen15 halamanSolutions Ch07KyleBelum ada peringkat

- Interim Financial ReportingDokumen4 halamanInterim Financial Reportingbelle crisBelum ada peringkat

- Section 9-4 QADokumen3 halamanSection 9-4 QAZeinab MohamadBelum ada peringkat

- Handsout 06 Chap 03 Part 02Dokumen4 halamanHandsout 06 Chap 03 Part 02Shane VeiraBelum ada peringkat

- p1 Quiz With TheoryDokumen16 halamanp1 Quiz With TheoryRica RegorisBelum ada peringkat

- Solution - Accounting For Income TaxesDokumen12 halamanSolution - Accounting For Income TaxesKlarissemay MontallanaBelum ada peringkat

- Soal Acc Income TaxDokumen2 halamanSoal Acc Income TaxVidya IntaniBelum ada peringkat

- Chapter 18 Govt GrantsDokumen6 halamanChapter 18 Govt Grantsrobinady dollaga100% (2)

- Assignment 6Dokumen8 halamanAssignment 6Muhammad AdilBelum ada peringkat

- Unit 1 - Essay QuestionsDokumen7 halamanUnit 1 - Essay QuestionsJaijuBelum ada peringkat

- Activity 3 CAMINGAWAN BSMA 2B PDFDokumen7 halamanActivity 3 CAMINGAWAN BSMA 2B PDFMiconBelum ada peringkat

- SolutionQuestionnaireUNIT 3 - 2020Dokumen5 halamanSolutionQuestionnaireUNIT 3 - 2020LiBelum ada peringkat

- Additional (Accelerated) Depreciation: Illustration PageDokumen4 halamanAdditional (Accelerated) Depreciation: Illustration PageAmer Wagdy GergesBelum ada peringkat

- Review Problems AnswersDokumen4 halamanReview Problems AnswersFranchette Yvonne JulianBelum ada peringkat

- IAS 12: Practice Questions AnswersDokumen8 halamanIAS 12: Practice Questions AnswersTaffy Isheanesu BgoniBelum ada peringkat

- 1) Answer Any Five Question From The Following .Each Question Carries Two MarksDokumen14 halaman1) Answer Any Five Question From The Following .Each Question Carries Two Marksmanasa k pBelum ada peringkat

- Thor Semiconductor Is An Exporter of Transistors To The United StatesDokumen6 halamanThor Semiconductor Is An Exporter of Transistors To The United StatesSophia KeratinBelum ada peringkat

- Chapter 18 CompilationDokumen21 halamanChapter 18 CompilationMaria Licuanan0% (1)

- Acct6005 Company Accounting: Assessment 2 Case StudyDokumen8 halamanAcct6005 Company Accounting: Assessment 2 Case StudyRuhan SinghBelum ada peringkat

- Chapter 11 Advacc 1 DayagDokumen17 halamanChapter 11 Advacc 1 Dayagchangevela67% (6)

- Final Exam Review QuestionsDokumen16 halamanFinal Exam Review QuestionsAj201819Belum ada peringkat

- Sol. Man. Chapter 4 Partnership Liquidation 2020 EditionDokumen30 halamanSol. Man. Chapter 4 Partnership Liquidation 2020 EditionJennifer RelosoBelum ada peringkat

- IFRS Week 6Dokumen4 halamanIFRS Week 6AleksandraBelum ada peringkat

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsDari EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsBelum ada peringkat

- Skene Albanians 1850Dokumen24 halamanSkene Albanians 1850VMROBelum ada peringkat

- 2006 018 389.01.02 People To People Actions JSPFDokumen16 halaman2006 018 389.01.02 People To People Actions JSPFVMROBelum ada peringkat

- 2014 1st Place in Teaching History March 2015 0Dokumen6 halaman2014 1st Place in Teaching History March 2015 0VMROBelum ada peringkat

- New Balkan Politics The Balkan Muslim Di PDFDokumen12 halamanNew Balkan Politics The Balkan Muslim Di PDFVMROBelum ada peringkat

- Whose Language? Exploring The Attitudes of Bulgaria's Media Elite Toward Macedonia's Linguistic Self-IdentificationDokumen22 halamanWhose Language? Exploring The Attitudes of Bulgaria's Media Elite Toward Macedonia's Linguistic Self-IdentificationVMROBelum ada peringkat

- Jane SandanskiDokumen1 halamanJane SandanskiVMROBelum ada peringkat

- A Return To SocratesDokumen3 halamanA Return To SocratesVMROBelum ada peringkat

- MacedoniaPoliticsofEthnicityandConflict PDFDokumen21 halamanMacedoniaPoliticsofEthnicityandConflict PDFVMROBelum ada peringkat

- Declassified DocumentsDokumen340 halamanDeclassified DocumentsVMROBelum ada peringkat

- TermsDokumen7 halamanTermsVMROBelum ada peringkat

- NooseaDokumen166 halamanNooseaVMROBelum ada peringkat

- MinorityDokumen13 halamanMinorityVMROBelum ada peringkat

- SorosDokumen59 halamanSorosVMROBelum ada peringkat

- Xero AnnualDokumen66 halamanXero AnnualVMROBelum ada peringkat

- 01 GrigorievaDokumen9 halaman01 GrigorievaVMROBelum ada peringkat

- This Is The Published VersionDokumen12 halamanThis Is The Published VersionVMROBelum ada peringkat

- Albanian Grammar: Studies On Albanian and Other Balkan Language by Victor A. Friedman Peja: Dukagjini. 2004Dokumen17 halamanAlbanian Grammar: Studies On Albanian and Other Balkan Language by Victor A. Friedman Peja: Dukagjini. 2004RaulySilvaBelum ada peringkat

- Macedonia, The Lung of Greece Fighting An Uphill Battle BlackDokumen29 halamanMacedonia, The Lung of Greece Fighting An Uphill Battle BlackVMROBelum ada peringkat

- Lecture Text May 18, 2008Dokumen11 halamanLecture Text May 18, 2008VMROBelum ada peringkat

- Panslavism PDFDokumen109 halamanPanslavism PDFVMROBelum ada peringkat

- Generalsketchofp 00 InneuoftDokumen440 halamanGeneralsketchofp 00 InneuoftVMROBelum ada peringkat

- Warranty Card For Australia - EnglishDokumen3 halamanWarranty Card For Australia - EnglishVMROBelum ada peringkat

- The Tsars Loyal Greeks The Russian Diplo PDFDokumen15 halamanThe Tsars Loyal Greeks The Russian Diplo PDFVMROBelum ada peringkat

- MACEDONIADokumen4 halamanMACEDONIAVMROBelum ada peringkat

- Eastern EuropeDokumen1 halamanEastern EuropeVMROBelum ada peringkat

- Haemus 1 - 2012Dokumen240 halamanHaemus 1 - 2012Siniša KrznarBelum ada peringkat

- Make DonDokumen1 halamanMake DonVMROBelum ada peringkat

- MyLocker User Manual v1.0 (Mode 8)Dokumen18 halamanMyLocker User Manual v1.0 (Mode 8)gika12345Belum ada peringkat

- Macedonian MushroomsDokumen3 halamanMacedonian MushroomsVMROBelum ada peringkat

- Possession Demand LetterDokumen4 halamanPossession Demand LetterVileshBelum ada peringkat

- PdataDokumen6 halamanPdataRazor11111Belum ada peringkat

- Corporate Tax PlanningDokumen8 halamanCorporate Tax PlanningTumie Lets0% (1)

- Drucker Vs CommissionerDokumen1 halamanDrucker Vs CommissionerAthena SantosBelum ada peringkat

- Invoice: Sustaincert SaDokumen1 halamanInvoice: Sustaincert SaNorato XerindaBelum ada peringkat

- GST Invoice: Shubham Engineering Works - (2019-20)Dokumen3 halamanGST Invoice: Shubham Engineering Works - (2019-20)vinodBelum ada peringkat

- GET - Indicative Compensation Details - B.TechsDokumen1 halamanGET - Indicative Compensation Details - B.Techskush 9031Belum ada peringkat

- Refund of IGST On Export of Goods PDFDokumen7 halamanRefund of IGST On Export of Goods PDFCA Rahul ModiBelum ada peringkat

- Sitel Philippines Corporation V CIR G.R. No 201326 - February 8, 2017 FactsDokumen2 halamanSitel Philippines Corporation V CIR G.R. No 201326 - February 8, 2017 FactsTicia Co So100% (3)

- Cir V. Pilipinas Shell Petroleum Facts:: Exemption Provided in Sec. 135 Attaches To The PetroleumDokumen5 halamanCir V. Pilipinas Shell Petroleum Facts:: Exemption Provided in Sec. 135 Attaches To The PetroleumDennis Aran Tupaz AbrilBelum ada peringkat

- 961028.CD FTH Brosura Pages 1 425Dokumen5 halaman961028.CD FTH Brosura Pages 1 425Luka VukicBelum ada peringkat

- Quiz #3Dokumen4 halamanQuiz #3Jenny BernardinoBelum ada peringkat

- Payslip 2022 2023 9 Inf0047318 ISSINDIADokumen1 halamanPayslip 2022 2023 9 Inf0047318 ISSINDIAManohar NMBelum ada peringkat

- Reen LawnsDokumen8 halamanReen LawnsAshish BhallaBelum ada peringkat

- 8 Sison Vs AnchetaDokumen1 halaman8 Sison Vs AnchetarjBelum ada peringkat

- AK Personal 1Dokumen13 halamanAK Personal 1erniBelum ada peringkat

- Service Description: Internet Access ServiceDokumen1 halamanService Description: Internet Access ServiceYatnaBelum ada peringkat

- Paseo Realty Vs Court of AppealsDokumen9 halamanPaseo Realty Vs Court of AppealsChristelle Ayn BaldosBelum ada peringkat

- Chapter 11Dokumen5 halamanChapter 11张心怡Belum ada peringkat

- Adyen Invoice BR202111001041.Company - Frubana BRDokumen2 halamanAdyen Invoice BR202111001041.Company - Frubana BRBruno Tescaro RomaBelum ada peringkat

- PPSC Lecturer Recruitment 2015 Math Mcqs For Lecturer Test 2015Dokumen7 halamanPPSC Lecturer Recruitment 2015 Math Mcqs For Lecturer Test 2015ALI ASGHERBelum ada peringkat

- Blinkit-Offer Letter-Yashas Nag. U!-SignedDokumen2 halamanBlinkit-Offer Letter-Yashas Nag. U!-Signedvijaybhaskar damireddy100% (1)

- Tax Invoice: Page 1 of 2Dokumen2 halamanTax Invoice: Page 1 of 2nirooBelum ada peringkat

- Topic 1 - Budget ConstraintsDokumen76 halamanTopic 1 - Budget ConstraintsAhmad MahmoodBelum ada peringkat

- Paystub TjmaxxDokumen1 halamanPaystub Tjmaxxyishii258000Belum ada peringkat

- Lladoc vs. CIR (G.R. No. L-19201 June 16, 1965) - H DIGESTDokumen1 halamanLladoc vs. CIR (G.R. No. L-19201 June 16, 1965) - H DIGESTHarleneBelum ada peringkat

- InvoiceDokumen1 halamanInvoiceLIBU GEORGE B 16PHD0594Belum ada peringkat

- Business Tax Laws in The PhilippinesDokumen12 halamanBusiness Tax Laws in The PhilippinesEthel Joi Manalac MendozaBelum ada peringkat

- Astha Nirman SewaDokumen3 halamanAstha Nirman SewaDibas BaniyaBelum ada peringkat

- eFPS Home - Efiling and Payment System AprilDokumen2 halamaneFPS Home - Efiling and Payment System AprilRenalynBelum ada peringkat