Anda mungkin juga menyukai

- Banking and Capital MarketsDokumen1 halamanBanking and Capital Marketsshank16589Belum ada peringkat

- Control Diabetes Ebook by Guru MannDokumen8 halamanControl Diabetes Ebook by Guru MannGaurav Sharma100% (1)

- IT ServicesDokumen489 halamanIT Servicesshank16589Belum ada peringkat

- 2016 L1 SS10Dokumen2 halaman2016 L1 SS10shank16589Belum ada peringkat

- 2016 L1 SS12Dokumen3 halaman2016 L1 SS12shank16589Belum ada peringkat

- Prasthanam Movie ScreenplayDokumen191 halamanPrasthanam Movie ScreenplayAllTeluguFilms100% (2)

- 2016 L1 SS08Dokumen3 halaman2016 L1 SS08shank16589Belum ada peringkat

- 2016 L1 SS16Dokumen2 halaman2016 L1 SS16shank16589Belum ada peringkat

- 2016 L1 SS02 PDFDokumen4 halaman2016 L1 SS02 PDFXPloadTBelum ada peringkat

- 2016 L1 SS18Dokumen2 halaman2016 L1 SS18shank16589Belum ada peringkat

- 2016 L1 SS06Dokumen2 halaman2016 L1 SS06shank16589Belum ada peringkat

- CRISIL Research Ier Report Electrosteel 2014 Q3FY14fcDokumen10 halamanCRISIL Research Ier Report Electrosteel 2014 Q3FY14fcshank16589Belum ada peringkat

- Ethical and Professional Standards: Study SessionDokumen2 halamanEthical and Professional Standards: Study Sessionshank16589Belum ada peringkat

- Ethical and Professional Standards: Study SessionDokumen2 halamanEthical and Professional Standards: Study Sessionshank16589Belum ada peringkat

- M and ADokumen5 halamanM and Ashank16589Belum ada peringkat

- Adobe - Photoshop - Every - Tool.Explained PDFDokumen130 halamanAdobe - Photoshop - Every - Tool.Explained PDFsmachevaBelum ada peringkat

- Ambit Strategy Good & Clean 4.0 The Great 50Dokumen16 halamanAmbit Strategy Good & Clean 4.0 The Great 50Anoop RavindranBelum ada peringkat

- 2013 Annual ReportDokumen86 halaman2013 Annual Reportshank16589Belum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- 1GF S4hana1909 BPD en UsDokumen15 halaman1GF S4hana1909 BPD en UsBiji RoyBelum ada peringkat

- QUIZ - CHAPTER 1 - STATEMENT OF FINANCIAL POSITION With SolutionsDokumen9 halamanQUIZ - CHAPTER 1 - STATEMENT OF FINANCIAL POSITION With Solutionsfinn mertens100% (1)

- Parcor Chapter 1Dokumen6 halamanParcor Chapter 1Taylor SwiftBelum ada peringkat

- Kieso 14e PowerPoint Ch24Dokumen59 halamanKieso 14e PowerPoint Ch24James LeeBelum ada peringkat

- 2022 Special Olympics Missouri Annual ReportDokumen6 halaman2022 Special Olympics Missouri Annual ReportSpecial Olympics MissouriBelum ada peringkat

- Horizontal&Vertical Analysis Sample ProblemDokumen3 halamanHorizontal&Vertical Analysis Sample ProblemGenner RazBelum ada peringkat

- SOP Finance DepartmentDokumen21 halamanSOP Finance DepartmentAjay Kumar100% (1)

- Glen 2001097 KPNK4CDokumen3 halamanGlen 2001097 KPNK4CGlen ParadiseBelum ada peringkat

- Coso 2013 Internal Control Over External Financial Reporting - Integrate 1 PDFDokumen172 halamanCoso 2013 Internal Control Over External Financial Reporting - Integrate 1 PDFDora RodriguezBelum ada peringkat

- ACCA F3 Quiz 2 - RJDokumen2 halamanACCA F3 Quiz 2 - RJRahimBelum ada peringkat

- Business Com. Prelim ExamDokumen7 halamanBusiness Com. Prelim ExamJeane Mae BooBelum ada peringkat

- Chapter 5 Osama Mehmood Ali1 Erp Modules Alexis LeonDokumen44 halamanChapter 5 Osama Mehmood Ali1 Erp Modules Alexis LeonNikhil PrasannaBelum ada peringkat

- Unit 2: Financial Analysis 2.0 Aims and ObjectivesDokumen13 halamanUnit 2: Financial Analysis 2.0 Aims and ObjectiveshabtamuBelum ada peringkat

- RGU SyllabusDokumen3 halamanRGU SyllabusAnuran BordoloiBelum ada peringkat

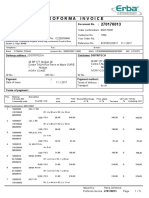

- FACTURE PRO FORMA ERBA PI 270170013 DistritechDokumen5 halamanFACTURE PRO FORMA ERBA PI 270170013 DistritechLuc YaoBelum ada peringkat

- Jawaban Intermediate Accounting Zaki Baridwan CertDokumen1 halamanJawaban Intermediate Accounting Zaki Baridwan Certnaomi devaBelum ada peringkat

- Audit Manual Part1Dokumen250 halamanAudit Manual Part1Romer Lesondato100% (2)

- DYBSAAgn313 - Accounting For Government & Non-Profit Organizations (MIDTERM MODULE) PDFDokumen11 halamanDYBSAAgn313 - Accounting For Government & Non-Profit Organizations (MIDTERM MODULE) PDFJonnafe Almendralejo IntanoBelum ada peringkat

- Financial Accounting Config S4HANADokumen64 halamanFinancial Accounting Config S4HANAalegpontonBelum ada peringkat

- Ficobbpfinalone10022011 120815114154 Phpapp02Dokumen146 halamanFicobbpfinalone10022011 120815114154 Phpapp02prashantaiwaleBelum ada peringkat

- CH 03 SolDokumen4 halamanCH 03 Solbhavin_tannaBelum ada peringkat

- Basic Accounting Reviewer Corpo PDFDokumen30 halamanBasic Accounting Reviewer Corpo PDFanthony lañaBelum ada peringkat

- Memo 097.9 082321 Internal Quality Audit IQA CY 2021 Advisory No.2Dokumen4 halamanMemo 097.9 082321 Internal Quality Audit IQA CY 2021 Advisory No.2David CastilloBelum ada peringkat

- ACCA Competency Framework How and When To Use 2020Dokumen6 halamanACCA Competency Framework How and When To Use 2020thanhloan1902Belum ada peringkat

- Full Download Ethics in Accounting A Decision Making Approach 1st Edition Solutions Klein PDF Full ChapterDokumen36 halamanFull Download Ethics in Accounting A Decision Making Approach 1st Edition Solutions Klein PDF Full Chapterapolloniccondylemoieax100% (13)

- Acctg 102 - Prelim Exams - 3048Dokumen3 halamanAcctg 102 - Prelim Exams - 3048AYAME MALINAO BSA19Belum ada peringkat

- Session 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureDokumen18 halamanSession 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureRheneir MoraBelum ada peringkat

- General Journal Entry - FABMDokumen10 halamanGeneral Journal Entry - FABMHannah SophiaBelum ada peringkat

- 7 IFRS 7 Financial Instruments - DisclosuresDokumen72 halaman7 IFRS 7 Financial Instruments - DisclosuresMihaelaBelum ada peringkat

- Users of Accounting Information-INTERNAL & EXTERNALDokumen3 halamanUsers of Accounting Information-INTERNAL & EXTERNALKayelle BelinoBelum ada peringkat