Anda mungkin juga menyukai

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Indian Contract Act 1872Dokumen84 halamanIndian Contract Act 1872Satya KumarBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Unit IDokumen5 halamanUnit ISatya KumarBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Digital Payments EnglishDokumen45 halamanDigital Payments EnglishSatya KumarBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Analysis of Fintech Startups in India DissertationDokumen52 halamanAnalysis of Fintech Startups in India DissertationSatya KumarBelum ada peringkat

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Dr. K V R Satya Kumar Assoc Professor Dept of Management Studies, VJIT & Dr. Seema Nazneen Assoc Professor Som, AuDokumen26 halamanDr. K V R Satya Kumar Assoc Professor Dept of Management Studies, VJIT & Dr. Seema Nazneen Assoc Professor Som, AuSatya KumarBelum ada peringkat

- Day 1 RegressionDokumen30 halamanDay 1 RegressionSatya KumarBelum ada peringkat

- Unit 1: - Investment Environment in India - Overview of Indian Financial System - Investment AlternativesDokumen35 halamanUnit 1: - Investment Environment in India - Overview of Indian Financial System - Investment AlternativesSatya KumarBelum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Analysis of Fintech Startups in India DissertationDokumen52 halamanAnalysis of Fintech Startups in India DissertationSatya KumarBelum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- World FinTech Report WFTR 2019 WebDokumen36 halamanWorld FinTech Report WFTR 2019 WebKen N.100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Day 3 ModerationDokumen25 halamanDay 3 ModerationSatya KumarBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Chapter 3 - Methodology Final Visalakshi PDFDokumen34 halamanChapter 3 - Methodology Final Visalakshi PDFSatya KumarBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Top 10 Mobile Wallets in IndiaDokumen39 halamanTop 10 Mobile Wallets in IndiaSatya KumarBelum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- IFM - Evolution of IMSDokumen31 halamanIFM - Evolution of IMSSatya KumarBelum ada peringkat

- 5s and KaizenDokumen28 halaman5s and KaizenSatya KumarBelum ada peringkat

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Cyber Law of IndiaDokumen14 halamanCyber Law of IndiaSatya KumarBelum ada peringkat

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Mefa Course Outcomes:: Course Objectives:-To Enable The Student To Understand, With A Practical InsightDokumen3 halamanMefa Course Outcomes:: Course Objectives:-To Enable The Student To Understand, With A Practical InsightSatya KumarBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Evaluation Criteria of DemingDokumen5 halamanEvaluation Criteria of DemingSatya KumarBelum ada peringkat

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- IFM - Problem On BopDokumen6 halamanIFM - Problem On BopSatya KumarBelum ada peringkat

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- 5S Kaizen Pokayoke: Business Structures and Processes PresentationDokumen20 halaman5S Kaizen Pokayoke: Business Structures and Processes PresentationSatya KumarBelum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- MEFA Unit Wise Imp QuestionsDokumen6 halamanMEFA Unit Wise Imp QuestionsSatya KumarBelum ada peringkat

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Synphosis On Project FinanceDokumen3 halamanSynphosis On Project FinanceSatya KumarBelum ada peringkat

- Invoice Flomih & Vio Bussines SRL: CX Ref: 18911926 Invoice No.: 151140-838 Invoice Date: 29 Nov 2019Dokumen1 halamanInvoice Flomih & Vio Bussines SRL: CX Ref: 18911926 Invoice No.: 151140-838 Invoice Date: 29 Nov 2019calinmusceleanuBelum ada peringkat

- 11 Acc CH 1 Introduction To Accounting 23-24Dokumen15 halaman11 Acc CH 1 Introduction To Accounting 23-24Nathan DavidBelum ada peringkat

- Alekseev Innokenty 2002Dokumen66 halamanAlekseev Innokenty 2002Harpott GhantaBelum ada peringkat

- Imports With Letter of Credit in SAP ERPDokumen8 halamanImports With Letter of Credit in SAP ERPMohamed QamarBelum ada peringkat

- SUBJECT MATTER 6 - QuizDokumen4 halamanSUBJECT MATTER 6 - QuizKingChryshAnneBelum ada peringkat

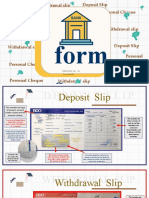

- Form S: Deposit Slip Withdrawal Slip Deposit Slip Personal ChequeDokumen4 halamanForm S: Deposit Slip Withdrawal Slip Deposit Slip Personal ChequeNathalia LeonadoBelum ada peringkat

- Comparative Study of Loans and Advances of Commercial BanksDokumen22 halamanComparative Study of Loans and Advances of Commercial BanksNoaman AkbarBelum ada peringkat

- Digital Payments Driving Financial InclusionDokumen73 halamanDigital Payments Driving Financial InclusionAyush NahakBelum ada peringkat

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Request For NOC To Avail LoanDokumen3 halamanRequest For NOC To Avail LoanShirish63% (8)

- Capital Bridge 9% IFISA BondDokumen24 halamanCapital Bridge 9% IFISA BondhyenadogBelum ada peringkat

- Anant Ekka, Roll No.26, Sec-A, Law of InsuranceDokumen18 halamanAnant Ekka, Roll No.26, Sec-A, Law of InsuranceAnantHimanshuEkkaBelum ada peringkat

- Cash Flow Statement - HODokumen7 halamanCash Flow Statement - HOAditi VermaBelum ada peringkat

- K-A-K Accruals & Prepayments QuestionsDokumen3 halamanK-A-K Accruals & Prepayments QuestionsUmer Farooq0% (1)

- Kalviseithi - 6,7,8 Lesson Plan Term 2 - All Subject PDFDokumen220 halamanKalviseithi - 6,7,8 Lesson Plan Term 2 - All Subject PDFJalagandeeswaran KalimuthuBelum ada peringkat

- Account Statement As of 23-10-2020 09:17:02 GMT +0530Dokumen19 halamanAccount Statement As of 23-10-2020 09:17:02 GMT +0530padma princessBelum ada peringkat

- Delta Spinners 2010Dokumen41 halamanDelta Spinners 2010bari.sarkarBelum ada peringkat

- In ProgressDokumen12 halamanIn ProgressQamarulArifinBelum ada peringkat

- Kwitansi Receipt: Pola TeknikDokumen1 halamanKwitansi Receipt: Pola Teknikꓰꓡ ꓖꓴꓮꓣꓣꓳꓟꓮꓠꓔꓲꓚꓳꓳBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- 3rd Case DigestDokumen3 halaman3rd Case DigestNoela Glaze Abanilla DivinoBelum ada peringkat

- Axis Bank - Financial Overview of Axis Bank & Comparative Study of Current Account and Saving AccDokumen103 halamanAxis Bank - Financial Overview of Axis Bank & Comparative Study of Current Account and Saving Accपं रामजी विदुआ हेमन्तBelum ada peringkat

- Accuflow Cash Disbursements ProcessDokumen3 halamanAccuflow Cash Disbursements ProcessRini Susanty100% (2)

- Executive Summary: Rizal Commercial Banking CorporationDokumen6 halamanExecutive Summary: Rizal Commercial Banking CorporationMon Toribio AtractivoBelum ada peringkat

- Titan Company Ltd. (India) : SourceDokumen6 halamanTitan Company Ltd. (India) : SourceDivyagarapatiBelum ada peringkat

- Chapter 7 in Class Practice SolutionDokumen12 halamanChapter 7 in Class Practice Solution919282902Belum ada peringkat

- KARUNANITHI SRINIVASAN1647319871895-credit-reportDokumen26 halamanKARUNANITHI SRINIVASAN1647319871895-credit-reportHaritUchilBelum ada peringkat

- Dividend Policy QuestionsDokumen8 halamanDividend Policy QuestionsRonmaty VixBelum ada peringkat

- Audited Consolidated Financial StatementDokumen42 halamanAudited Consolidated Financial StatementAbigail EjiroBelum ada peringkat

- A3 Signature CardDokumen2 halamanA3 Signature CardSteve LimBelum ada peringkat

- Issues in Financial Accounting 15th Edition Henderson Test BankDokumen7 halamanIssues in Financial Accounting 15th Edition Henderson Test BankJosephGlasswosmrBelum ada peringkat

- Question Compilation - 230316 - 072454Dokumen9 halamanQuestion Compilation - 230316 - 072454Ranjan DhakalBelum ada peringkat

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDari Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNPenilaian: 4.5 dari 5 bintang4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDari EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisPenilaian: 5 dari 5 bintang5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDari EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaPenilaian: 3.5 dari 5 bintang3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDari EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (14)