Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Pet Kingdom Tax ReturnDokumen26 halamanPet Kingdom Tax ReturnRaychael Ross100% (2)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Tax Deductions Explained: Interest, Taxes, LossesDokumen12 halamanTax Deductions Explained: Interest, Taxes, LossesJaneBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Awiral Kumar Offer LetterDokumen2 halamanAwiral Kumar Offer LetterAkansha AgrawalBelum ada peringkat

- Chapter Three Payroll Accounting 3.1. Importance of Payroll AccountingDokumen11 halamanChapter Three Payroll Accounting 3.1. Importance of Payroll Accountingyebegashet100% (2)

- Extended Revision Exercises: Number: Worksheet 17: Managing MoneyDokumen2 halamanExtended Revision Exercises: Number: Worksheet 17: Managing Moneymk hatBelum ada peringkat

- Processing Classes (SAP HCM)Dokumen5 halamanProcessing Classes (SAP HCM)chinnipappu1Belum ada peringkat

- Matter Group 2: I. Definition of Matter and Its ExampleDokumen8 halamanMatter Group 2: I. Definition of Matter and Its ExampleMichael S LeysonBelum ada peringkat

- 2Dokumen1 halaman2Michael S LeysonBelum ada peringkat

- TMP - 3404-Comparison Chart-27721623 PDFDokumen2 halamanTMP - 3404-Comparison Chart-27721623 PDFMichael S LeysonBelum ada peringkat

- The Continuum Identified Four Main Styles of LeadershipDokumen1 halamanThe Continuum Identified Four Main Styles of LeadershipMichael S LeysonBelum ada peringkat

- Stock SplitDokumen2 halamanStock SplitMichael S LeysonBelum ada peringkat

- Pru Life UK 2015 Annual Report HighlightsDokumen61 halamanPru Life UK 2015 Annual Report HighlightsMichael S LeysonBelum ada peringkat

- Practice Question: Cash Flow StatementDokumen4 halamanPractice Question: Cash Flow Statementtheultimate74% (19)

- Problems On Cash Flow StatementsDokumen12 halamanProblems On Cash Flow Statementsdevvratrajgopal73% (11)

- Formal LeadershipDokumen1 halamanFormal LeadershipMichael S LeysonBelum ada peringkat

- APB Partnership Liquidation Cash Distribution PlanDokumen2 halamanAPB Partnership Liquidation Cash Distribution PlanJose MataloBelum ada peringkat

- Stock SplitDokumen2 halamanStock SplitMichael S LeysonBelum ada peringkat

- Key PointsDokumen1 halamanKey PointsMichael S LeysonBelum ada peringkat

- Income Tax Department Income Tax Department: Non-Filing of Return Non-Filing of ReturnDokumen1 halamanIncome Tax Department Income Tax Department: Non-Filing of Return Non-Filing of ReturnSarvesh SamantBelum ada peringkat

- Qrmp-Scheme NovDokumen2 halamanQrmp-Scheme NovVishwanath HollaBelum ada peringkat

- Letter Template-1Dokumen21 halamanLetter Template-1QwertyBelum ada peringkat

- Estate Taxes 2Dokumen56 halamanEstate Taxes 2Patrick TanBelum ada peringkat

- MOHAMAD ARUL KHAIRULLAH Payroll Slip PT Nusantara Ekspres Kilat May 2022 UnlockedDokumen1 halamanMOHAMAD ARUL KHAIRULLAH Payroll Slip PT Nusantara Ekspres Kilat May 2022 UnlockedArul Mhmmd10Belum ada peringkat

- Draft Refund RulesDokumen7 halamanDraft Refund RulessridharanBelum ada peringkat

- Reimbursement Receipt FormDokumen2 halamanReimbursement Receipt Formsplef lguBelum ada peringkat

- Service Billed To:: Pt. KDB Tifa Finance TBKDokumen1 halamanService Billed To:: Pt. KDB Tifa Finance TBKBram MonoBelum ada peringkat

- Richard Pieris Exports PLCDokumen9 halamanRichard Pieris Exports PLCDPH ResearchBelum ada peringkat

- Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Dokumen1 halamanCertificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)halima halimaBelum ada peringkat

- Honoraria PayrollDokumen1 halamanHonoraria PayrollCharles Kenn Mantilla75% (4)

- BAR QUESTIONS (From 2005 To 2012 Bar Exams)Dokumen60 halamanBAR QUESTIONS (From 2005 To 2012 Bar Exams)Em LayronBelum ada peringkat

- File TDS return online for property saleDokumen3 halamanFile TDS return online for property saleAnand JaiswalBelum ada peringkat

- CSL Pi08144Dokumen1 halamanCSL Pi08144Alok SinghBelum ada peringkat

- Eris Therapeutics LTD: Salary Slip For December - 2022Dokumen1 halamanEris Therapeutics LTD: Salary Slip For December - 2022Raja ThakurBelum ada peringkat

- Garfield Company bonus calculation and Kaila Corporation debt restructuring journal entriesDokumen2 halamanGarfield Company bonus calculation and Kaila Corporation debt restructuring journal entriesvenice cambryBelum ada peringkat

- 1 CIR V Hambrecht - QuistDokumen2 halaman1 CIR V Hambrecht - Quistaspiringlawyer1234Belum ada peringkat

- IntaxationDokumen3 halamanIntaxationErinBelum ada peringkat

- Employee Declaration Form FY 2020-21Dokumen2 halamanEmployee Declaration Form FY 2020-21Harsha I100% (2)

- ANNUAL TAX STATEMENT 2021-22Dokumen1 halamanANNUAL TAX STATEMENT 2021-22adnan JamilBelum ada peringkat

- Report Mr. Tharun 936 25 16 Age 18 SA 500000Dokumen5 halamanReport Mr. Tharun 936 25 16 Age 18 SA 500000tharunshanmugam25Belum ada peringkat

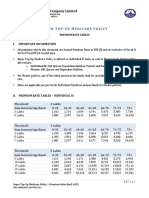

- Super Top-Up Medicare Policy Premium Chart - Including GSTDokumen6 halamanSuper Top-Up Medicare Policy Premium Chart - Including GSTvinay_814585077Belum ada peringkat

- Sterling Holiday Resorts September PaySlipDokumen1 halamanSterling Holiday Resorts September PaySlipNazir Ahmad GanieBelum ada peringkat

- Kama (Seepz) 0700Dokumen2 halamanKama (Seepz) 0700yogesh padilkarBelum ada peringkat