Anda mungkin juga menyukai

- Intrinsic Value Calculator Adam KhOODokumen3 halamanIntrinsic Value Calculator Adam KhOOShereeAnnTorres25% (8)

- Case Study - Hill Country Snack Foods Co.Dokumen2 halamanCase Study - Hill Country Snack Foods Co.Spencer123455678967% (3)

- Detect Payroll FraudDokumen7 halamanDetect Payroll FraudSheree SandersBelum ada peringkat

- Finance Simulation: Estimated Equity Value of Bel Vino CorporationDokumen4 halamanFinance Simulation: Estimated Equity Value of Bel Vino Corporationvardhan73% (11)

- Williams, 2002 SolutionDokumen16 halamanWilliams, 2002 Solutionimtehan_chowdhury0% (3)

- Winfield Refuse ManagementDokumen13 halamanWinfield Refuse ManagementAnshul Sehgal100% (3)

- Group 4 Williams SFMDokumen7 halamanGroup 4 Williams SFMthisissick100% (3)

- Winfield ManagementDokumen5 halamanWinfield Managementmadhav1111Belum ada peringkat

- Dividend Decision at Linear TechnologyDokumen8 halamanDividend Decision at Linear TechnologyNikhilaBelum ada peringkat

- Loewen Group CaseDokumen2 halamanLoewen Group CaseSu_NeilBelum ada peringkat

- OM Scott Case AnalysisDokumen20 halamanOM Scott Case AnalysissushilkhannaBelum ada peringkat

- Submitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Dokumen3 halamanSubmitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Aurva BhardwajBelum ada peringkat

- Analyzing Mercury Athletic Footwear AcquisitionDokumen5 halamanAnalyzing Mercury Athletic Footwear AcquisitionCuong NguyenBelum ada peringkat

- Case Study: Hill Country Snack Foods " HCSF " (With Soluion )Dokumen12 halamanCase Study: Hill Country Snack Foods " HCSF " (With Soluion )Kamran Shabbir50% (2)

- 454K Loan for Cartwright Lumber CoDokumen5 halaman454K Loan for Cartwright Lumber CoRushil Surapaneni50% (2)

- 13 Earned Value ManagementDokumen9 halaman13 Earned Value ManagementAbhinandan Singh100% (1)

- Teuer Furniture (A)Dokumen14 halamanTeuer Furniture (A)Abhinandan SinghBelum ada peringkat

- Case Study 4 Winfield Refuse Management, Inc.: Raising Debt vs. EquityDokumen5 halamanCase Study 4 Winfield Refuse Management, Inc.: Raising Debt vs. EquityAditya DashBelum ada peringkat

- Hill CountryDokumen8 halamanHill CountryAtif Raza AkbarBelum ada peringkat

- Winfield Refuse ManagementDokumen13 halamanWinfield Refuse Managementnishant JaiswalBelum ada peringkat

- Strides Arcolab's $650-700M dividend payout decisionDokumen15 halamanStrides Arcolab's $650-700M dividend payout decisionNAMI100% (1)

- JetBlue 2012 Fuel Hedging StrategyDokumen3 halamanJetBlue 2012 Fuel Hedging StrategyPritam Karmakar0% (1)

- Hill Country Snack Foods CoDokumen9 halamanHill Country Snack Foods CoZjiajiajiajiaPBelum ada peringkat

- Hill Country Snack Foods Co - UDokumen4 halamanHill Country Snack Foods Co - Unipun9143Belum ada peringkat

- Hill Country Snack Foods CoDokumen1 halamanHill Country Snack Foods CoKriti AhujaBelum ada peringkat

- Williams CEO evaluates $900M financing offer and long-term strategyDokumen1 halamanWilliams CEO evaluates $900M financing offer and long-term strategyYun Clare Yang0% (1)

- Updated Stone Container PaperDokumen6 halamanUpdated Stone Container Paperonetime699100% (1)

- Finance Case - Blaine Kitchenware - GRP - 11Dokumen4 halamanFinance Case - Blaine Kitchenware - GRP - 11Shona Baroi100% (3)

- New Heritage Doll Company Report: Design Your Own Doll Project Best ChoiceDokumen5 halamanNew Heritage Doll Company Report: Design Your Own Doll Project Best ChoiceRahul LalwaniBelum ada peringkat

- Case Summary Financial Management-II: "The Loewen Group, Inc. (Abridged) "Dokumen4 halamanCase Summary Financial Management-II: "The Loewen Group, Inc. (Abridged) "Rishabh Kothari100% (1)

- Hill Country Snack Foods Co - UDokumen4 halamanHill Country Snack Foods Co - Unipun9143Belum ada peringkat

- WilliamsDokumen20 halamanWilliamsUmesh GuptaBelum ada peringkat

- FIN 370 Final Exam 30 Questions With AnswersDokumen11 halamanFIN 370 Final Exam 30 Questions With Answersassignmentsehelp0% (1)

- Use More SoapsDokumen9 halamanUse More SoapsAbhinandan SinghBelum ada peringkat

- Valuation of 5000 stock options using Black Scholes model over 5 yearsDokumen4 halamanValuation of 5000 stock options using Black Scholes model over 5 yearsAbhinandan Singh0% (2)

- Job Satisfaction and Employee Engagement Case StudyDokumen11 halamanJob Satisfaction and Employee Engagement Case StudyMuneeb Ur-Rehman0% (1)

- Mccaw Cellular Communications - The At& Amp T - Mccaw Merger Negotiation - Free EssaysDokumen7 halamanMccaw Cellular Communications - The At& Amp T - Mccaw Merger Negotiation - Free EssaysGrey StephensonBelum ada peringkat

- FINANCE MANAGEMENT FIN420 CHP 6Dokumen52 halamanFINANCE MANAGEMENT FIN420 CHP 6Yanty IbrahimBelum ada peringkat

- Winfieldpresentationfinal 130212133845 Phpapp02Dokumen26 halamanWinfieldpresentationfinal 130212133845 Phpapp02Sukanta JanaBelum ada peringkat

- Hospital Corporation Of America Maintains A RatingDokumen16 halamanHospital Corporation Of America Maintains A RatingDhruv Kalia50% (2)

- Winfield PPT 27 FEB 13Dokumen13 halamanWinfield PPT 27 FEB 13prem_kumar83g100% (4)

- Continental Carriers Debt vs EquityDokumen10 halamanContinental Carriers Debt vs Equitynipun9143Belum ada peringkat

- Hill Country SnackDokumen8 halamanHill Country Snackkiller dramaBelum ada peringkat

- ClarksonDokumen22 halamanClarksonfrankstandaert8714Belum ada peringkat

- Winfield Refuse. - Case QuestionsDokumen1 halamanWinfield Refuse. - Case QuestionsthoroftedalBelum ada peringkat

- Case Background: Kaustav Dey B18088Dokumen9 halamanCase Background: Kaustav Dey B18088Kaustav DeyBelum ada peringkat

- Hill Country Snack Food Co. Optimal Capital StructureDokumen7 halamanHill Country Snack Food Co. Optimal Capital StructureAnish NarulaBelum ada peringkat

- Winfield Refuse Management Inc. Raising Debt vs. EquityDokumen13 halamanWinfield Refuse Management Inc. Raising Debt vs. EquitynmenalopezBelum ada peringkat

- Case StudyDokumen10 halamanCase StudyEvelyn VillafrancaBelum ada peringkat

- Lex Service PLC - Cost of Capital1Dokumen4 halamanLex Service PLC - Cost of Capital1Ravi VatsaBelum ada peringkat

- Williams Seeks $900M Financing to Address Liquidity CrisisDokumen4 halamanWilliams Seeks $900M Financing to Address Liquidity CrisisAnirudh SurendranBelum ada peringkat

- This Study Resource Was: 1 Hill Country Snack Foods CoDokumen9 halamanThis Study Resource Was: 1 Hill Country Snack Foods CoPavithra TamilBelum ada peringkat

- LinearDokumen6 halamanLinearjackedup211Belum ada peringkat

- MEG CV 2 CaseDokumen10 halamanMEG CV 2 Casegabal_m50% (2)

- Corporate Finance - Hill Country Snack FoodDokumen11 halamanCorporate Finance - Hill Country Snack FoodNell MizunoBelum ada peringkat

- Marriott Cost of Capital Analysis for Lodging DivisionDokumen3 halamanMarriott Cost of Capital Analysis for Lodging DivisionPabloCaicedoArellanoBelum ada peringkat

- Ethical Dilemma of Conflict On Trading FloorDokumen10 halamanEthical Dilemma of Conflict On Trading FloorManpreet0711Belum ada peringkat

- HAMPTON MACHINE TOOL Case - PresentationDokumen7 halamanHAMPTON MACHINE TOOL Case - PresentationChaitanya90% (10)

- Hill Country Snack Foods CompanyDokumen14 halamanHill Country Snack Foods CompanyVeni GuptaBelum ada peringkat

- Continental CarriersDokumen6 halamanContinental CarriersVishwas Nandan100% (1)

- Linear Technology Dividend Policy and Shareholder ValueDokumen4 halamanLinear Technology Dividend Policy and Shareholder ValueAmrinder SinghBelum ada peringkat

- Maximizing Shareholder Value Through Optimal Dividend and Buyback PolicyDokumen2 halamanMaximizing Shareholder Value Through Optimal Dividend and Buyback PolicyRichBrook7Belum ada peringkat

- case-UST IncDokumen10 halamancase-UST Incnipun9143Belum ada peringkat

- Strategy Consulting: Session 4 Declining Industries Buffet'S Bid For Media General'S NewspapersDokumen13 halamanStrategy Consulting: Session 4 Declining Industries Buffet'S Bid For Media General'S NewspapersPrashant JhakarwarBelum ada peringkat

- Calculate WACC and Cost of Common EquityDokumen24 halamanCalculate WACC and Cost of Common EquityAdirtnBelum ada peringkat

- WinfieldDokumen4 halamanWinfieldMOHIT SINGHBelum ada peringkat

- FIN222 Autumn2016 Tutorials Tutorial 8Dokumen8 halamanFIN222 Autumn2016 Tutorials Tutorial 8HELENABelum ada peringkat

- FIN 370 Final Exam - AssignmentDokumen11 halamanFIN 370 Final Exam - AssignmentstudentehelpBelum ada peringkat

- Name: Meenakshi MBA-II Semester MB0029 Financial ManagementDokumen10 halamanName: Meenakshi MBA-II Semester MB0029 Financial Managementbaku85Belum ada peringkat

- Merchandise Presentation in Retail Store - Intro, Demo, Floor Layout and SignageDokumen26 halamanMerchandise Presentation in Retail Store - Intro, Demo, Floor Layout and SignageAbhinandan SinghBelum ada peringkat

- Starbucks Deliveringcustomerservice 160222181028Dokumen11 halamanStarbucks Deliveringcustomerservice 160222181028Abhinandan SinghBelum ada peringkat

- World CSR Congress: Integrating Sustainability Into A Global OrganizationDokumen12 halamanWorld CSR Congress: Integrating Sustainability Into A Global OrganizationAbhinandan SinghBelum ada peringkat

- Merve BEKTAŞ Didem ŞAHİN Sara OsmanoğluDokumen22 halamanMerve BEKTAŞ Didem ŞAHİN Sara OsmanoğluAbhinandan SinghBelum ada peringkat

- Mortein Vaporizer Marketing StrategyDokumen26 halamanMortein Vaporizer Marketing Strategymukesh chavanBelum ada peringkat

- Positioning Book ReviewDokumen35 halamanPositioning Book ReviewSmat JacerBelum ada peringkat

- G GeniusDokumen26 halamanG GeniusAbhinandan SinghBelum ada peringkat

- Category Management 2Dokumen9 halamanCategory Management 2Abhinandan SinghBelum ada peringkat

- Stratergic Management Case Study On StarbucksDokumen30 halamanStratergic Management Case Study On StarbucksRahul Sttud50% (2)

- Visualmerchandising 121126111353 Phpapp02Dokumen145 halamanVisualmerchandising 121126111353 Phpapp02Abhinandan SinghBelum ada peringkat

- 5 Fastest Frontend Web Dev Frameworks - Fonbell SolutionDokumen13 halaman5 Fastest Frontend Web Dev Frameworks - Fonbell SolutionAbhinandan SinghBelum ada peringkat

- Starbucks: Delivering Customer ServiceDokumen23 halamanStarbucks: Delivering Customer ServiceVishakha Rl RanaBelum ada peringkat

- Leading Supply Chain Without Suits and TiesDokumen11 halamanLeading Supply Chain Without Suits and TiesAnoop AgrawalBelum ada peringkat

- Batiste 2in1 Dry Shampoo & Conditioner: Refreshes Roots and Targets Dryness For Gorgeously Soft, Conditioned HairDokumen11 halamanBatiste 2in1 Dry Shampoo & Conditioner: Refreshes Roots and Targets Dryness For Gorgeously Soft, Conditioned HairAbhinandan SinghBelum ada peringkat

- The Wonder of Mumbai Dabbawallas Inspiration of ManagementDokumen23 halamanThe Wonder of Mumbai Dabbawallas Inspiration of ManagementSeema Mehta SharmaBelum ada peringkat

- Product Palaning Refe1Dokumen58 halamanProduct Palaning Refe1rafiq5002Belum ada peringkat

- FINAL - New Product Development and Feasibility PDFDokumen7 halamanFINAL - New Product Development and Feasibility PDFRenz PamintuanBelum ada peringkat

- General Motors and Its SuppliersDokumen8 halamanGeneral Motors and Its SuppliersAbhinandan SinghBelum ada peringkat

- Six Sigma - IDokumen133 halamanSix Sigma - INitin PatelBelum ada peringkat

- XLRI Strategic Management of Apple Inc. in 2015Dokumen6 halamanXLRI Strategic Management of Apple Inc. in 2015Abhinandan SinghBelum ada peringkat

- Freelancing ListDokumen29 halamanFreelancing ListAbhinandan SinghBelum ada peringkat

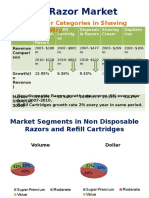

- US Razor Market ParamountDokumen17 halamanUS Razor Market ParamountAbhinandan SinghBelum ada peringkat

- TR EB Data Breach ResponseDokumen5 halamanTR EB Data Breach ResponseAbhinandan SinghBelum ada peringkat

- Saatchi&SaatchiDokumen5 halamanSaatchi&SaatchiAbhinandan SinghBelum ada peringkat

- Atlantic Computer - A Bundling of Pricing OptionsDokumen15 halamanAtlantic Computer - A Bundling of Pricing OptionsAbhinandan SinghBelum ada peringkat

- Slides2 StudentsDokumen41 halamanSlides2 StudentsSkirata75Belum ada peringkat

- Chapter 3 Bond Valuation Edited (Student)Dokumen14 halamanChapter 3 Bond Valuation Edited (Student)Nguyễn Thái Minh ThưBelum ada peringkat

- Sources & Cost of CapitalDokumen123 halamanSources & Cost of Capitaliamjith133680% (5)

- Financial Statement Analysis - Concept Questions and Solutions - Chapter 1Dokumen13 halamanFinancial Statement Analysis - Concept Questions and Solutions - Chapter 1ObydulRanaBelum ada peringkat

- IFRS13 Fair Value MeasurementDokumen79 halamanIFRS13 Fair Value MeasurementAnep ZainuldinBelum ada peringkat

- Master Input Sheet: InputsDokumen37 halamanMaster Input Sheet: Inputsminhthuc203Belum ada peringkat

- Mckinsey Appraisal - AppraisalDokumen8 halamanMckinsey Appraisal - Appraisalalex.nogueira396Belum ada peringkat

- IBPS RRB Office Assistant Mains 2018Dokumen23 halamanIBPS RRB Office Assistant Mains 2018Debadutta SethiBelum ada peringkat

- Fixed Rate Mortgage Homework ProblemsDokumen2 halamanFixed Rate Mortgage Homework ProblemscjBelum ada peringkat

- The error is in the second part of the sentence. The correct part is:The Prime Minister will announce the scheme if the Cabinet approves itDokumen50 halamanThe error is in the second part of the sentence. The correct part is:The Prime Minister will announce the scheme if the Cabinet approves itPawan Patankar100% (1)

- Promissory Notes, Simple Discount Notes, and The Discount ProcessDokumen18 halamanPromissory Notes, Simple Discount Notes, and The Discount ProcessAnnie VBelum ada peringkat

- Equity Valuation BookDokumen3 halamanEquity Valuation BookooppaaBelum ada peringkat

- Financial Management Lecture 2Dokumen27 halamanFinancial Management Lecture 2Tesfaye ejetaBelum ada peringkat

- Understanding Treasury BillsDokumen2 halamanUnderstanding Treasury BillsAnav AggarwalBelum ada peringkat

- Bonds Payable Accounting & ReportingDokumen12 halamanBonds Payable Accounting & ReportingJehPoyBelum ada peringkat

- Chapter 2Dokumen22 halamanChapter 2Tiến ĐứcBelum ada peringkat

- AEC 210 FinalRequirementDokumen9 halamanAEC 210 FinalRequirementALMA MORENABelum ada peringkat

- OCC Interest Rate RiskDokumen74 halamanOCC Interest Rate RiskSara HumayunBelum ada peringkat

- Investments: Chapter Learning ObjectivesDokumen44 halamanInvestments: Chapter Learning ObjectivesRahma NadhifaBelum ada peringkat

- Outlook Profit On L&T-1Dokumen10 halamanOutlook Profit On L&T-1Tentu VenkataramanaBelum ada peringkat

- CH 17 InvestmentsDokumen117 halamanCH 17 InvestmentsSamiHadadBelum ada peringkat

- Sampa Video G3 - SecBDokumen3 halamanSampa Video G3 - SecBEina GuptaBelum ada peringkat

- Current Liabilities - ProvisionsDokumen9 halamanCurrent Liabilities - ProvisionsJerome_JadeBelum ada peringkat

- A Comparative Study of Public and Private Sector Banks in IndiaDokumen10 halamanA Comparative Study of Public and Private Sector Banks in IndiaEditor IJRITCC100% (1)

- Final Exam Cfas WoDokumen11 halamanFinal Exam Cfas WoAndrei GoBelum ada peringkat

- Mock Exam September 2020 Attempt AFM - AnswerDokumen6 halamanMock Exam September 2020 Attempt AFM - AnswerKubBelum ada peringkat