Anda mungkin juga menyukai

- IS LM AnalysisDokumen40 halamanIS LM AnalysisPrahaladh100% (1)

- Chaopte r34 NotesDokumen5 halamanChaopte r34 Noteschinsu6893Belum ada peringkat

- MECO Lecture11Dokumen23 halamanMECO Lecture11saif ur rehmanBelum ada peringkat

- Lecture 3Dokumen16 halamanLecture 3superzttBelum ada peringkat

- 11 Monetary Fiscal Policy AD C21Dokumen38 halaman11 Monetary Fiscal Policy AD C21minaevilBelum ada peringkat

- Review of The Previous LectureDokumen36 halamanReview of The Previous LectureMuhammad Usman AshrafBelum ada peringkat

- Revision Test 1Dokumen15 halamanRevision Test 1ndonithando2207Belum ada peringkat

- Chap 34Dokumen7 halamanChap 34mehmet nedimBelum ada peringkat

- Monetary Policy Implementation and OperationsDokumen38 halamanMonetary Policy Implementation and OperationskeeriofazlerabiBelum ada peringkat

- Ch-30 Money Growth & InflationDokumen37 halamanCh-30 Money Growth & InflationSnehal BhattBelum ada peringkat

- Macroeconomic Policy Instruments - IDokumen35 halamanMacroeconomic Policy Instruments - IAbdoukadirr SambouBelum ada peringkat

- Monetary and Fiscal PolicyDokumen31 halamanMonetary and Fiscal PolicyprasadzinjurdeBelum ada peringkat

- Session 17Dokumen16 halamanSession 17Sid Tushaar SiddharthBelum ada peringkat

- Determination of Interest RateDokumen35 halamanDetermination of Interest Rateznz17_78248Belum ada peringkat

- Unit 5 Is & LM AnalysisDokumen16 halamanUnit 5 Is & LM AnalysisAnshumaan PatroBelum ada peringkat

- Chapter 28 NotesDokumen4 halamanChapter 28 Notesburneymcb100% (1)

- The Keynesian System (Money, Interest and Income)Dokumen59 halamanThe Keynesian System (Money, Interest and Income)Almas100% (1)

- Lecture 07n FullDokumen40 halamanLecture 07n Fullcharlie simoBelum ada peringkat

- The Influence of Monetary and Fiscal Policy On Aggregate DemandDokumen37 halamanThe Influence of Monetary and Fiscal Policy On Aggregate DemandS. M. SAKIB RAIHAN Spring 20Belum ada peringkat

- MoneyDokumen46 halamanMoneyLuna VeraBelum ada peringkat

- Topic 8Dokumen26 halamanTopic 8Zayed Mohammad JohnyBelum ada peringkat

- ECONOMICS Exchange Rate DeterminationDokumen21 halamanECONOMICS Exchange Rate DeterminationMariya JasmineBelum ada peringkat

- Section 4 - Long-Run and Short-Run AnalysisDokumen64 halamanSection 4 - Long-Run and Short-Run AnalysisMbusoThabetheBelum ada peringkat

- Chapter 4Dokumen98 halamanChapter 4Chesta BrownBelum ada peringkat

- The IS - LM CurveDokumen28 halamanThe IS - LM CurveVikku AgarwalBelum ada peringkat

- Exchange Rate Determination: Prepared by Mariya Jasmine M YDokumen21 halamanExchange Rate Determination: Prepared by Mariya Jasmine M Ydeepika singhBelum ada peringkat

- The Demand For Money and Central Bank: - Item - Item - Item - EtcDokumen20 halamanThe Demand For Money and Central Bank: - Item - Item - Item - Etcvarun1785Belum ada peringkat

- Exchange Rate MechanismDokumen42 halamanExchange Rate Mechanismpriya nBelum ada peringkat

- The Role of Money in Macroeconomics: Chapter 19 (13 ED), 20 &21-LipseyDokumen62 halamanThe Role of Money in Macroeconomics: Chapter 19 (13 ED), 20 &21-LipseyKhuzaimah AhmadBelum ada peringkat

- Interest RateDokumen22 halamanInterest RateMimi mariyamBelum ada peringkat

- Money Growth and Inflation: The Meaning of MoneyDokumen29 halamanMoney Growth and Inflation: The Meaning of Moneysafdar2020Belum ada peringkat

- Lecture 4 - Central Banking - MBAIB5214 PDFDokumen28 halamanLecture 4 - Central Banking - MBAIB5214 PDFAsiri GunarathnaBelum ada peringkat

- ECO 104 Faculty: Asif Chowdhury: The Influence of Monetary & Fiscal Policy On Aggregate Demand (Part 1) (Ch:21 P.O.M.E)Dokumen9 halamanECO 104 Faculty: Asif Chowdhury: The Influence of Monetary & Fiscal Policy On Aggregate Demand (Part 1) (Ch:21 P.O.M.E)KaziRafiBelum ada peringkat

- IslmDokumen48 halamanIslmmendoza3rixBelum ada peringkat

- Monetary Policy PresentationDokumen21 halamanMonetary Policy PresentationAqib javed100% (2)

- b8.Makro-Monetary PolicyDokumen19 halamanb8.Makro-Monetary PolicyEvan AlviyanBelum ada peringkat

- Money: - What Is Money? - 3 Distinguishing Features of MoneyDokumen46 halamanMoney: - What Is Money? - 3 Distinguishing Features of MoneyabissembayBelum ada peringkat

- Monetary PolicyDokumen15 halamanMonetary Policyhimanshu_choudhary_2Belum ada peringkat

- Module 1 Central BankingDokumen25 halamanModule 1 Central BankingMaxene GabuteraBelum ada peringkat

- Module 2Dokumen28 halamanModule 2shubhamlakhani2003Belum ada peringkat

- L6L7 - Money, Price Level, and InflationDokumen42 halamanL6L7 - Money, Price Level, and InflationHalifa SyadidahBelum ada peringkat

- Chapter 3Dokumen41 halamanChapter 3nigusu deguBelum ada peringkat

- Worksheet For Chapter 13 (2023)Dokumen39 halamanWorksheet For Chapter 13 (2023)Ncebakazi DawedeBelum ada peringkat

- Aggregate Demand and Aggregate Supply EconomicsDokumen38 halamanAggregate Demand and Aggregate Supply EconomicsEsha ChaudharyBelum ada peringkat

- Chapter 2 Part 2 IFMDokumen15 halamanChapter 2 Part 2 IFMVaibhav PandeyBelum ada peringkat

- Intermediate Macroeconomics (Ecn 2215) : Money and Inflation Lecture Notes by Charles M. Banda Notes Extracted From MankiwDokumen25 halamanIntermediate Macroeconomics (Ecn 2215) : Money and Inflation Lecture Notes by Charles M. Banda Notes Extracted From MankiwYande ZuluBelum ada peringkat

- Role of Government in Economy.: Monetary PolicyDokumen16 halamanRole of Government in Economy.: Monetary PolicyDIPALI GOREGAONKAR�Belum ada peringkat

- Macroeconomics QuestionDokumen8 halamanMacroeconomics Questionmdkhairulalam19920Belum ada peringkat

- Macroeconomics1:: Inflation: Its Causes and Costs (Chapter 30)Dokumen32 halamanMacroeconomics1:: Inflation: Its Causes and Costs (Chapter 30)Donghun ShinBelum ada peringkat

- IS-LM ModelDokumen31 halamanIS-LM ModelAbdoukadirr SambouBelum ada peringkat

- International Adjustment and InterdependenceDokumen22 halamanInternational Adjustment and Interdependencekushal100% (2)

- Session 4 Money and Monetary PolicyDokumen50 halamanSession 4 Money and Monetary PolicyBiswajit PrustyBelum ada peringkat

- Monetary POLICYDokumen21 halamanMonetary POLICYSrishti VasdevBelum ada peringkat

- For Class InflationDokumen13 halamanFor Class InflationNagarjuna AtukuriBelum ada peringkat

- 5 WEEK GEHon Economics IIth Semeter Introductory MacroeconomicsDokumen14 halaman5 WEEK GEHon Economics IIth Semeter Introductory Macroeconomicskasturisahoo20Belum ada peringkat

- Financial Derivative and Energy Market Valuation: Theory and Implementation in MATLABDari EverandFinancial Derivative and Energy Market Valuation: Theory and Implementation in MATLABPenilaian: 3.5 dari 5 bintang3.5/5 (1)

- Financial Risk Management: A Simple IntroductionDari EverandFinancial Risk Management: A Simple IntroductionPenilaian: 4.5 dari 5 bintang4.5/5 (7)

- The Money Game Strategies to Win and ProsperDari EverandThe Money Game Strategies to Win and ProsperPenilaian: 5 dari 5 bintang5/5 (1)

- Economics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsDari EverandEconomics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsBelum ada peringkat

- Econ Course 202 Academy SayDokumen909 halamanEcon Course 202 Academy SayKoyakuBelum ada peringkat

- Investment and The Stock Market: Stock Capital Same Same StockDokumen32 halamanInvestment and The Stock Market: Stock Capital Same Same StockKoyakuBelum ada peringkat

- Example Example: (5.5) : Continuation of (5.4)Dokumen22 halamanExample Example: (5.5) : Continuation of (5.4)KoyakuBelum ada peringkat

- Wage Determination: Collective BargainingDokumen46 halamanWage Determination: Collective BargainingKoyakuBelum ada peringkat

- Current Labor MarketDokumen42 halamanCurrent Labor MarketKoyakuBelum ada peringkat

- Determination of The Optimal Capital InvestmentDokumen34 halamanDetermination of The Optimal Capital InvestmentKoyakuBelum ada peringkat

- Shifts of The Curve: Price Level Money Supply ExogenousDokumen28 halamanShifts of The Curve: Price Level Money Supply ExogenousKoyakuBelum ada peringkat

- Consumption: Disposable IncomeDokumen49 halamanConsumption: Disposable IncomeKoyakuBelum ada peringkat

- Bond Prices and Interest RatesDokumen27 halamanBond Prices and Interest RatesKoyakuBelum ada peringkat

- Monetary Policy and Open Market OperationsDokumen37 halamanMonetary Policy and Open Market OperationsKoyakuBelum ada peringkat

- Money: Assets PaymentDokumen25 halamanMoney: Assets PaymentKoyakuBelum ada peringkat

- Learning ObjectivesDokumen33 halamanLearning ObjectivesKoyakuBelum ada peringkat

- Borrowing Constraints: - SameDokumen29 halamanBorrowing Constraints: - SameKoyakuBelum ada peringkat

- The Government Sector: - Income Taxes and Automatic StabilizersDokumen44 halamanThe Government Sector: - Income Taxes and Automatic StabilizersKoyakuBelum ada peringkat

- The Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeDokumen33 halamanThe Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeKoyakuBelum ada peringkat

- Market For Goods in The Classical Model: Lower Discourages EncouragesDokumen28 halamanMarket For Goods in The Classical Model: Lower Discourages EncouragesKoyakuBelum ada peringkat

- Saving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantDokumen29 halamanSaving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantKoyakuBelum ada peringkat

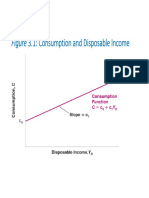

- Figure 3.1: Consumption and Disposable IncomeDokumen33 halamanFigure 3.1: Consumption and Disposable IncomeKoyakuBelum ada peringkat

- Income Tax Case List Exam Related PurposeDokumen9 halamanIncome Tax Case List Exam Related PurposeShubham PhophaliaBelum ada peringkat

- International Financial Management 13 Edition: by Jeff MaduraDokumen25 halamanInternational Financial Management 13 Edition: by Jeff MaduraAbdulaziz Al-amroBelum ada peringkat

- Utilization of IP and Need For ValuationDokumen15 halamanUtilization of IP and Need For ValuationBrain LeagueBelum ada peringkat

- TEST BANK For Government and Not For Profit Accounting Concepts and Practices 6th Edition by Granof Khumawala20190702 86031 1d2i3lg PDFDokumen16 halamanTEST BANK For Government and Not For Profit Accounting Concepts and Practices 6th Edition by Granof Khumawala20190702 86031 1d2i3lg PDFMaria Ceth SerranoBelum ada peringkat

- NMC GOLD FINANCE LIMITED - Forensic Report 1Dokumen11 halamanNMC GOLD FINANCE LIMITED - Forensic Report 1Anand KhotBelum ada peringkat

- PM Mudra Loan - How To Take Loan PDFDokumen9 halamanPM Mudra Loan - How To Take Loan PDFbhramaniBelum ada peringkat

- Peranan Bank Perkreditan Rakyat Binaan Bank Nagari Terhadap Kinerja Usaha Kecil Di Sumatera BaratDokumen200 halamanPeranan Bank Perkreditan Rakyat Binaan Bank Nagari Terhadap Kinerja Usaha Kecil Di Sumatera BaratPapan AjaBelum ada peringkat

- midChapterTest 1-1 1-4Dokumen1 halamanmidChapterTest 1-1 1-4VIPBelum ada peringkat

- PWB VR VUer 6 NW SG2 CDokumen5 halamanPWB VR VUer 6 NW SG2 CManeendra ManthinaBelum ada peringkat

- Cambridge International General Certificate of Secondary EducationDokumen9 halamanCambridge International General Certificate of Secondary Educationcheah_chinBelum ada peringkat

- Rencana TradingDokumen17 halamanRencana TradingArya PuwentaBelum ada peringkat

- Prelim Take-Home ExamDokumen12 halamanPrelim Take-Home ExamAmbassador WantedBelum ada peringkat

- Chapter - 1Dokumen69 halamanChapter - 1111induBelum ada peringkat

- Chapter 7 - Portfolio inDokumen12 halamanChapter 7 - Portfolio intemedebereBelum ada peringkat

- Chapter 11Dokumen23 halamanChapter 11narasimha50% (6)

- AccountStatement 3286686240 Aug04 185310 PDFDokumen2 halamanAccountStatement 3286686240 Aug04 185310 PDFDarren Joseph VivekBelum ada peringkat

- Case Law Seciton 23 Initial Allowance On Old Eleigible Depriciable AssetDokumen8 halamanCase Law Seciton 23 Initial Allowance On Old Eleigible Depriciable AssetBilal BashirBelum ada peringkat

- Bank StatementDokumen2 halamanBank StatementhanhBelum ada peringkat

- Assignment 12Dokumen4 halamanAssignment 12Joey BuddyBossBelum ada peringkat

- Health Insurance and Risk ManagementDokumen7 halamanHealth Insurance and Risk ManagementPritam BhowmickBelum ada peringkat

- Quotation - Hemas, SERVICE AND REPAIRS PDFDokumen2 halamanQuotation - Hemas, SERVICE AND REPAIRS PDFW GangenathBelum ada peringkat

- Transaction AnalysisDokumen33 halamanTransaction AnalysisIzzeah RamosBelum ada peringkat

- Jaya Property Annual Report 2015Dokumen169 halamanJaya Property Annual Report 2015KeziaBelum ada peringkat

- CIR Vs PhilamlifeDokumen2 halamanCIR Vs PhilamlifeBreAmberBelum ada peringkat

- Risk and Rates of Return ExerciseDokumen61 halamanRisk and Rates of Return ExerciseLee Wong100% (2)

- What Are Definition of Islamic Capital Market (ICM)Dokumen45 halamanWhat Are Definition of Islamic Capital Market (ICM)Zizie2014Belum ada peringkat

- U.S. Individual Income Tax Return: (See Instructions.)Dokumen2 halamanU.S. Individual Income Tax Return: (See Instructions.)Daniel RamirezBelum ada peringkat

- Chap 2 BafinDokumen5 halamanChap 2 BafinPhilip DizonBelum ada peringkat

- Cost - CH-1 Cma-IiDokumen14 halamanCost - CH-1 Cma-IiShimelis TesemaBelum ada peringkat

- Neuvoo Cert CanDokumen4 halamanNeuvoo Cert CaniansyaBelum ada peringkat