Anda mungkin juga menyukai

- Maximize Profits for Hospital Supply IncDokumen3 halamanMaximize Profits for Hospital Supply Incmade3875% (4)

- Davey Brothers Watch Co. SubmissionDokumen13 halamanDavey Brothers Watch Co. SubmissionEkta Derwal PGP 2022-24 BatchBelum ada peringkat

- MAC Davey Brothers - AkshatDokumen4 halamanMAC Davey Brothers - AkshatPRIKSHIT SAINI IPM 2019-24 BatchBelum ada peringkat

- LP Formulation - Chandpur Enterprises LimitedDokumen10 halamanLP Formulation - Chandpur Enterprises LimitedMagaly Stefany Sáenz CárdenasBelum ada peringkat

- Varun Nagar Cooperative Society: (Document Subtitle)Dokumen9 halamanVarun Nagar Cooperative Society: (Document Subtitle)Vedansh DubeyBelum ada peringkat

- Hospital Supply Inc Cost AnalysisDokumen5 halamanHospital Supply Inc Cost AnalysisMEERA JOSHY 192743633% (3)

- Group - 9 - Sec - B - IQDM - Merton - Truck - CompanyDokumen8 halamanGroup - 9 - Sec - B - IQDM - Merton - Truck - CompanyMANVENDRA SINGH PGP 2019-21 BatchBelum ada peringkat

- Case Analysis Rosemont Hill Health Center V3 PDFDokumen8 halamanCase Analysis Rosemont Hill Health Center V3 PDFPoorvi SinghalBelum ada peringkat

- WCM QuestionsDokumen5 halamanWCM QuestionsBhavin BaxiBelum ada peringkat

- Case 16 Answers - Hospital Supply IncDokumen14 halamanCase 16 Answers - Hospital Supply IncRaul Carrera, Jr.100% (3)

- Case Study 2 - ChandpurDokumen11 halamanCase Study 2 - Chandpurpriyaa03100% (3)

- Chapter 16 PDFDokumen43 halamanChapter 16 PDFAdaad As0% (1)

- Amaranth Disaster: How One Trader Lost $6B in 30 DaysDokumen15 halamanAmaranth Disaster: How One Trader Lost $6B in 30 DaysRani ZahrBelum ada peringkat

- Chandpur Enterprise Limited - Steel DivisionDokumen3 halamanChandpur Enterprise Limited - Steel DivisionVinodSingh100% (1)

- Ch10solution ManualDokumen31 halamanCh10solution ManualJyunde WuBelum ada peringkat

- EZ Trailers Production OptimizationDokumen3 halamanEZ Trailers Production OptimizationSomething ChicBelum ada peringkat

- Symphony Orchestra Case StudyDokumen3 halamanSymphony Orchestra Case StudyBrandon ElkinsBelum ada peringkat

- LP Formulation - Alpha Steels - Hiring Temp Workers To Minimise CostDokumen3 halamanLP Formulation - Alpha Steels - Hiring Temp Workers To Minimise CostGautham0% (1)

- Satish M: Corporate Finance 2: MBA 2020-22Dokumen49 halamanSatish M: Corporate Finance 2: MBA 2020-22Keerthi PaulBelum ada peringkat

- Interest (1 - (1+r) - N/R) + PV of The Principal AmountDokumen2 halamanInterest (1 - (1+r) - N/R) + PV of The Principal AmountBellapu Durga vara prasadBelum ada peringkat

- Case Study of D.LIGHT DESIGN IN INDIADokumen10 halamanCase Study of D.LIGHT DESIGN IN INDIAKRook NitsBelum ada peringkat

- Case Study15Dokumen6 halamanCase Study15Arpita SahuBelum ada peringkat

- Problems & Solutions - RNSDokumen28 halamanProblems & Solutions - RNSAyushi0% (1)

- Duration: 2 Hours Total Marks: 30 Term-II Instructions: All Questions Are CompulsaryDokumen13 halamanDuration: 2 Hours Total Marks: 30 Term-II Instructions: All Questions Are CompulsaryAdiBelum ada peringkat

- Group 4 Symphony FinalDokumen10 halamanGroup 4 Symphony FinalSachin RajgorBelum ada peringkat

- Taxing Situations Two Cases On Income Taxes - An Accounting Case StudyDokumen5 halamanTaxing Situations Two Cases On Income Taxes - An Accounting Case Studyfossaceca80% (5)

- Case Study: Danshui Plant No2Dokumen3 halamanCase Study: Danshui Plant No2Abdelhamid JenzriBelum ada peringkat

- Mansa Building Case Study AnalysisDokumen14 halamanMansa Building Case Study AnalysisRikki DasBelum ada peringkat

- Financial Statement Framework for Evaluating Financial PerformanceDokumen9 halamanFinancial Statement Framework for Evaluating Financial PerformanceMalik Fahad YounasBelum ada peringkat

- Alberta Gauge Company CaseDokumen2 halamanAlberta Gauge Company Casenidhu291Belum ada peringkat

- Persuasive Essay Rocky Mountain Mutual CaseDokumen2 halamanPersuasive Essay Rocky Mountain Mutual Casegoldust0100% (1)

- Northboro Machine Tools CorporationDokumen9 halamanNorthboro Machine Tools Corporationsheersha kkBelum ada peringkat

- Lilac Flour Mills: Managerial Accounting and Control - IIDokumen9 halamanLilac Flour Mills: Managerial Accounting and Control - IISoni Kumari50% (4)

- Star Engineering CompanyDokumen5 halamanStar Engineering CompanyMarilou GabayaBelum ada peringkat

- Daud Engine Parts CompanyDokumen3 halamanDaud Engine Parts CompanyJawadBelum ada peringkat

- Amaranth Advisors: Burning Six Billion in Thirty DaysDokumen24 halamanAmaranth Advisors: Burning Six Billion in Thirty DaysRosalina MaharanaBelum ada peringkat

- Landau CompanyDokumen4 halamanLandau Companyrond_2728Belum ada peringkat

- Chapter 5Dokumen30 halamanChapter 5فاطمه حسينBelum ada peringkat

- Solutions (Chapters 9 and 10)Dokumen4 halamanSolutions (Chapters 9 and 10)Manabendra Das100% (1)

- Hospital Supply Inc.Dokumen4 halamanHospital Supply Inc.alomelo100% (2)

- CVPDokumen3 halamanCVPRajShekarReddyBelum ada peringkat

- Marketing Management (Session 3) : Case: Reinventing Adobe. by Nilanjan Mukherjee (PGP13156) Section CDokumen2 halamanMarketing Management (Session 3) : Case: Reinventing Adobe. by Nilanjan Mukherjee (PGP13156) Section CNILANJAN MUKHERJEE100% (1)

- Indian Institute of Management Kozhikode, Post Graduate Programme PGP 24 - Section BDokumen10 halamanIndian Institute of Management Kozhikode, Post Graduate Programme PGP 24 - Section BParas MavaniBelum ada peringkat

- Break Even AnalysisDokumen5 halamanBreak Even Analysisblue_mugBelum ada peringkat

- Midterm: (15 Points) : Indian Institute of Management Bangalore Decision Science II Old ExamsDokumen72 halamanMidterm: (15 Points) : Indian Institute of Management Bangalore Decision Science II Old ExamsNitishBelum ada peringkat

- 7-2 John Holtz (C) Case Study SolutionsDokumen14 halaman7-2 John Holtz (C) Case Study SolutionsAashima Grover100% (1)

- Statistika Ekonomi Bisnis Anderson 11th Edition, Chapter 1-6Dokumen56 halamanStatistika Ekonomi Bisnis Anderson 11th Edition, Chapter 1-6yunitaknBelum ada peringkat

- Additional Case-Lets For Practice-April 17-RaoDokumen13 halamanAdditional Case-Lets For Practice-April 17-RaoSankalp BhagatBelum ada peringkat

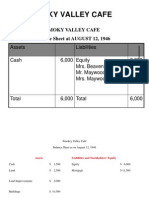

- Smokey Valley Cafe Balance Sheets 1946Dokumen3 halamanSmokey Valley Cafe Balance Sheets 1946mohit_namanBelum ada peringkat

- Classic Pen Company Activity Based CostingDokumen16 halamanClassic Pen Company Activity Based CostingIndahKusumawardhaniBelum ada peringkat

- Maximizing Surplus for VNACSDokumen6 halamanMaximizing Surplus for VNACSSrishti JainBelum ada peringkat

- 14 Additional Solved Problems 13Dokumen17 halaman14 Additional Solved Problems 13PIYUSH CHANDRAVANSHIBelum ada peringkat

- Forest City Tennis Club General Ledger and Financial StatementsDokumen9 halamanForest City Tennis Club General Ledger and Financial StatementsAhmedNiaz100% (1)

- Varun Nagar Agricultural Cooperative Society at 2 Am On 1st JuneDokumen6 halamanVarun Nagar Agricultural Cooperative Society at 2 Am On 1st JuneTushar KumarBelum ada peringkat

- Color ScopeDokumen12 halamanColor Scopeprincemech2004100% (1)

- CAN Submission-Unilever in India: Hindustan Lever's Project Shakti - Marketing FMCG To The Rural ConsumerDokumen3 halamanCAN Submission-Unilever in India: Hindustan Lever's Project Shakti - Marketing FMCG To The Rural ConsumerRitik MaheshwariBelum ada peringkat

- Cost I Chapter 4 Bproviding End To End Reliable Communication Is The Function of The TransportDokumen19 halamanCost I Chapter 4 Bproviding End To End Reliable Communication Is The Function of The TransportTahir DestaBelum ada peringkat

- Cost-Chapter 4 NewDokumen18 halamanCost-Chapter 4 NewYonas AyeleBelum ada peringkat

- MANAC Session-4Dokumen29 halamanMANAC Session-4Aastha SharmaBelum ada peringkat

- C.A-I Chapter-3Dokumen38 halamanC.A-I Chapter-3Tariku KolchaBelum ada peringkat

- Laws of Wages Lyst7869Dokumen10 halamanLaws of Wages Lyst7869Shreyansh PriyamBelum ada peringkat

- Trade Union Act 1926 Lyst7284Dokumen18 halamanTrade Union Act 1926 Lyst7284Shreyansh PriyamBelum ada peringkat

- AdvertisementsDokumen364 halamanAdvertisementsMayank AgrawalBelum ada peringkat

- Print 1Dokumen5 halamanPrint 1Shreyansh PriyamBelum ada peringkat

- Notes Chapter 1 Meaning and Objectives of AccountingDokumen16 halamanNotes Chapter 1 Meaning and Objectives of AccountingANMOL MISHRABelum ada peringkat

- How To Write A Book ReviewDokumen6 halamanHow To Write A Book ReviewNuzul ImranBelum ada peringkat

- Chapter 1 Law of Welfare and Working Conditions Factories Act 1948 Lyst4116Dokumen33 halamanChapter 1 Law of Welfare and Working Conditions Factories Act 1948 Lyst4116Shreyansh PriyamBelum ada peringkat

- Industrial Disputes Act 1947 SummaryDokumen36 halamanIndustrial Disputes Act 1947 SummaryShreyansh PriyamBelum ada peringkat

- History AssignmentDokumen32 halamanHistory AssignmentShreyansh PriyamBelum ada peringkat

- DischargeDokumen41 halamanDischargeShreyansh PriyamBelum ada peringkat

- Development Meaning and DefinitionDokumen18 halamanDevelopment Meaning and DefinitionShreyansh PriyamBelum ada peringkat

- DEVELOPMENT Communication .....Dokumen24 halamanDEVELOPMENT Communication .....Shreyansh PriyamBelum ada peringkat

- Research ProcessDokumen30 halamanResearch ProcessShreyansh PriyamBelum ada peringkat

- Dev Comm & Extension ApproachDokumen22 halamanDev Comm & Extension ApproachShreyansh PriyamBelum ada peringkat

- How To Write A Book ReviewDokumen6 halamanHow To Write A Book ReviewNuzul ImranBelum ada peringkat

- Creative BriefDokumen3 halamanCreative BriefShreyansh PriyamBelum ada peringkat

- Qualitative Versus Quantitative ResearchDokumen18 halamanQualitative Versus Quantitative ResearchShreyansh PriyamBelum ada peringkat

- Sampling: SR - Lecturer C.P.RashmiDokumen18 halamanSampling: SR - Lecturer C.P.RashmiShreyansh PriyamBelum ada peringkat

- Revenue Budget PreparationDokumen2 halamanRevenue Budget PreparationShreyansh PriyamBelum ada peringkat

- Media SchedulingDokumen4 halamanMedia SchedulingShreyansh PriyamBelum ada peringkat

- Sponsorship Proposal South AfricaDokumen14 halamanSponsorship Proposal South AfricanamitabaindoorBelum ada peringkat

- Budget Format - Cost AccountingDokumen5 halamanBudget Format - Cost AccountingShreyansh PriyamBelum ada peringkat

- Business Communication Assignment (Barriers of Communication - Summary)Dokumen2 halamanBusiness Communication Assignment (Barriers of Communication - Summary)Shreyansh PriyamBelum ada peringkat

- NewspaperDokumen11 halamanNewspaperКристина ОрёлBelum ada peringkat

- Sarvali On DigbalaDokumen14 halamanSarvali On DigbalapiyushBelum ada peringkat

- Katie Tiller ResumeDokumen4 halamanKatie Tiller Resumeapi-439032471Belum ada peringkat

- The European Journal of Applied Economics - Vol. 16 #2Dokumen180 halamanThe European Journal of Applied Economics - Vol. 16 #2Aleksandar MihajlovićBelum ada peringkat

- ERP Complete Cycle of ERP From Order To DispatchDokumen316 halamanERP Complete Cycle of ERP From Order To DispatchgynxBelum ada peringkat

- Skuld List of CorrespondentDokumen351 halamanSkuld List of CorrespondentKASHANBelum ada peringkat

- Site Visit Risk Assessment FormDokumen3 halamanSite Visit Risk Assessment FormAmanuelGirmaBelum ada peringkat

- Malware Reverse Engineering Part 1 Static AnalysisDokumen27 halamanMalware Reverse Engineering Part 1 Static AnalysisBik AshBelum ada peringkat

- Axe Case Study - Call Me NowDokumen6 halamanAxe Case Study - Call Me NowvirgoashishBelum ada peringkat

- Theory of Linear Programming: Standard Form and HistoryDokumen42 halamanTheory of Linear Programming: Standard Form and HistoryJayakumarBelum ada peringkat

- Survey Course OverviewDokumen3 halamanSurvey Course OverviewAnil MarsaniBelum ada peringkat

- Pom Final On Rice MillDokumen21 halamanPom Final On Rice MillKashif AliBelum ada peringkat

- AATCC 100-2004 Assesment of Antibacterial Dinishes On Textile MaterialsDokumen3 halamanAATCC 100-2004 Assesment of Antibacterial Dinishes On Textile MaterialsAdrian CBelum ada peringkat

- GLF550 Normal ChecklistDokumen5 halamanGLF550 Normal ChecklistPetar RadovićBelum ada peringkat

- Mtle - Hema 1Dokumen50 halamanMtle - Hema 1Leogene Earl FranciaBelum ada peringkat

- Acne Treatment Strategies and TherapiesDokumen32 halamanAcne Treatment Strategies and TherapiesdokterasadBelum ada peringkat

- Conv VersationDokumen4 halamanConv VersationCharmane Barte-MatalaBelum ada peringkat

- Sentinel 2 Products Specification DocumentDokumen510 halamanSentinel 2 Products Specification DocumentSherly BhengeBelum ada peringkat

- AZ-900T00 Microsoft Azure Fundamentals-01Dokumen21 halamanAZ-900T00 Microsoft Azure Fundamentals-01MgminLukaLayBelum ada peringkat

- Quantification of Dell S Competitive AdvantageDokumen3 halamanQuantification of Dell S Competitive AdvantageSandeep Yadav50% (2)

- Circular Flow of Process 4 Stages Powerpoint Slides TemplatesDokumen9 halamanCircular Flow of Process 4 Stages Powerpoint Slides TemplatesAryan JainBelum ada peringkat

- ITU SURVEY ON RADIO SPECTRUM MANAGEMENT 17 01 07 Final PDFDokumen280 halamanITU SURVEY ON RADIO SPECTRUM MANAGEMENT 17 01 07 Final PDFMohamed AliBelum ada peringkat

- Chapter 3 of David CrystalDokumen3 halamanChapter 3 of David CrystalKritika RamchurnBelum ada peringkat

- Ancient Greek Divination by Birthmarks and MolesDokumen8 halamanAncient Greek Divination by Birthmarks and MolessheaniBelum ada peringkat

- Chennai Metro Rail BoQ for Tunnel WorksDokumen6 halamanChennai Metro Rail BoQ for Tunnel WorksDEBASIS BARMANBelum ada peringkat

- Os PPT-1Dokumen12 halamanOs PPT-1Dhanush MudigereBelum ada peringkat

- DLL - The Firm and Its EnvironmentDokumen5 halamanDLL - The Firm and Its Environmentfrances_peña_7100% (2)

- Ensayo Bim - Jaime Alejandro Martinez Uribe PDFDokumen3 halamanEnsayo Bim - Jaime Alejandro Martinez Uribe PDFAlejandro MartinezBelum ada peringkat

- IGCSE Chemistry Section 5 Lesson 3Dokumen43 halamanIGCSE Chemistry Section 5 Lesson 3Bhawana SinghBelum ada peringkat