Anda mungkin juga menyukai

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- PWC A4 Data Governance ResultsDokumen36 halamanPWC A4 Data Governance ResultsHoangdhBelum ada peringkat

- Best Practices For Data Risk Management - Talk BusinessDokumen5 halamanBest Practices For Data Risk Management - Talk BusinessHoangdhBelum ada peringkat

- BCBS 239 Principles For Effective Risk Data Aggregation and Risk ReportingDokumen2 halamanBCBS 239 Principles For Effective Risk Data Aggregation and Risk ReportingHoangdhBelum ada peringkat

- The Implementation of Basel Committee BCBS 239: Short Analysis of The New Rules For Data ManagementDokumen16 halamanThe Implementation of Basel Committee BCBS 239: Short Analysis of The New Rules For Data ManagementHoangdhBelum ada peringkat

- Data Governance - What, Why, How, Who & 15 Best PracticesDokumen13 halamanData Governance - What, Why, How, Who & 15 Best PracticesHoangdhBelum ada peringkat

- What Drives The NewZeland DollarDokumen14 halamanWhat Drives The NewZeland DollarHoangdhBelum ada peringkat

- The Application of Basel II To Trading Activities and Treatment of Double Defult Effects BISDokumen91 halamanThe Application of Basel II To Trading Activities and Treatment of Double Defult Effects BISHoangdhBelum ada peringkat

- Vol2B3 CA Part3 Final 18 Aug 2014Dokumen53 halamanVol2B3 CA Part3 Final 18 Aug 2014HoangdhBelum ada peringkat

- Xlwings and ExcelDokumen19 halamanXlwings and ExcelHoangdh0% (1)

- Tidy QuantDokumen33 halamanTidy QuantHoangdhBelum ada peringkat

- Derivatives in Plain WordsDokumen172 halamanDerivatives in Plain WordsHoangdhBelum ada peringkat

- Applied Microsoft SQL Server 2008 Reporting Services PDFDokumen770 halamanApplied Microsoft SQL Server 2008 Reporting Services PDFOberto Jorge Santín CuestaBelum ada peringkat

- Systemic Risk of European Banks - Regulators and MarketsDokumen26 halamanSystemic Risk of European Banks - Regulators and MarketsHoangdhBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Exercise 8-7: Fadrigalan, Mia P. Gragasin, Charlie S. Gutierrez, Erica Anne N. Hamco, Gian Carlo G. Ibuna, Niño SDokumen7 halamanExercise 8-7: Fadrigalan, Mia P. Gragasin, Charlie S. Gutierrez, Erica Anne N. Hamco, Gian Carlo G. Ibuna, Niño Svomawew647Belum ada peringkat

- CITADEL SECURITIES Australia Pty LTD - Financial Report To 31-12-2020Dokumen22 halamanCITADEL SECURITIES Australia Pty LTD - Financial Report To 31-12-2020Brendan OswaldBelum ada peringkat

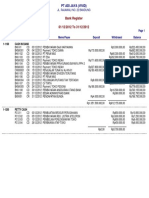

- Bank RegisterDokumen1 halamanBank RegisterVivid SariBelum ada peringkat

- Module I. Business Combination - Date of Acquisition (NA)Dokumen13 halamanModule I. Business Combination - Date of Acquisition (NA)Melanie SamsonaBelum ada peringkat

- MULTIPLE CHOICE-CPA AdaptedDokumen4 halamanMULTIPLE CHOICE-CPA AdaptedEdiane QuilezaBelum ada peringkat

- Case Digest Roman Catholic V LRCDokumen2 halamanCase Digest Roman Catholic V LRCIvy PazBelum ada peringkat

- Suggested Answers Section A: 1 CRG 660 JAN 2018Dokumen10 halamanSuggested Answers Section A: 1 CRG 660 JAN 2018auni fildzahBelum ada peringkat

- Securities Regulation Code of The Philippines (R.A. 8799) PurposeDokumen11 halamanSecurities Regulation Code of The Philippines (R.A. 8799) PurposeWilmar AbriolBelum ada peringkat

- A Study On Different Kinds of Business Entities and Their Advantages and DisadvantagesDokumen13 halamanA Study On Different Kinds of Business Entities and Their Advantages and DisadvantagesmanjuashokBelum ada peringkat

- Chapter 19 - Consol. Fs Part 4Dokumen17 halamanChapter 19 - Consol. Fs Part 4PutmehudgJasdBelum ada peringkat

- CategoryofShareholders31March2016 PDFDokumen18 halamanCategoryofShareholders31March2016 PDFGhulamMahyyudinBelum ada peringkat

- Articles of Incorporation of Stock CorporationDokumen4 halamanArticles of Incorporation of Stock CorporationInnoKalBelum ada peringkat

- RBS Controls FSA 2008Dokumen106 halamanRBS Controls FSA 2008Marc TaymansBelum ada peringkat

- STRICTLY PRIVATE and CONFIDENTIAL ChiefDokumen56 halamanSTRICTLY PRIVATE and CONFIDENTIAL ChiefFaidz FuadBelum ada peringkat

- Amendment Process For SEC-registered Corporations (Philippines)Dokumen1 halamanAmendment Process For SEC-registered Corporations (Philippines)Ian Leoj GumbanBelum ada peringkat

- Fraud ScenariosDokumen7 halamanFraud ScenariosElvisPresliiBelum ada peringkat

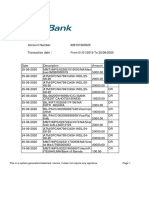

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDokumen15 halamanThis Is A System-Generated Statement. Hence, It Does Not Require Any SignaturemohitBelum ada peringkat

- A Director Is An Agent of The Company For The Conduct of The Business of The CompanyDokumen3 halamanA Director Is An Agent of The Company For The Conduct of The Business of The CompanyRanjeet SinghBelum ada peringkat

- Types of DebenturesDokumen3 halamanTypes of DebenturesMadhumitaSinghBelum ada peringkat

- Zambia: Doing Business in ZambiaDokumen4 halamanZambia: Doing Business in ZambiaKajal N Jignesh PatelBelum ada peringkat

- Puatnelson 2011Dokumen22 halamanPuatnelson 2011Bidang 3 HimaktaBelum ada peringkat

- Jindal Saw-AR-2017-18-NET PDFDokumen274 halamanJindal Saw-AR-2017-18-NET PDFshahavBelum ada peringkat

- Multinational Business Finance 10th Edition Solution ManualDokumen8 halamanMultinational Business Finance 10th Edition Solution ManualrspkamalgmailcomBelum ada peringkat

- Corporation Law: JGA Medina Bus. Org II, Philippine Law SchoolDokumen14 halamanCorporation Law: JGA Medina Bus. Org II, Philippine Law Schoolaprilaries78Belum ada peringkat

- Agency, Trust & Partnership Reviewer - 1837-1886 (Cambri Notes)Dokumen5 halamanAgency, Trust & Partnership Reviewer - 1837-1886 (Cambri Notes)Arvin FigueroaBelum ada peringkat

- Disbursement Voucher: LBP AlabelDokumen14 halamanDisbursement Voucher: LBP AlabelJames Hydoe ElanBelum ada peringkat

- Financial Scandal of ParmalatDokumen30 halamanFinancial Scandal of ParmalatMahmudul Hassan50% (2)

- Borrowing Powers of Directors of Public Limited CompaniesDokumen14 halamanBorrowing Powers of Directors of Public Limited CompaniesMuhammad Saeed BabarBelum ada peringkat

- Unit 1 Company Law Unit 1 Company LawDokumen40 halamanUnit 1 Company Law Unit 1 Company LawRanjan BaradurBelum ada peringkat

- Read Business Law Online by Robert W. Emerson - BooksDokumen1 halamanRead Business Law Online by Robert W. Emerson - Booksaminjamal0% (2)