Anda mungkin juga menyukai

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Top 10 Mistakes (FOREX TRADING)Dokumen12 halamanTop 10 Mistakes (FOREX TRADING)Marie Chris Abragan YañezBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- 3 ERP ArchitectureDokumen100 halaman3 ERP ArchitectureShriyanshi JaitlyBelum ada peringkat

- 4 ERP ImplementationDokumen116 halaman4 ERP ImplementationShriyanshi JaitlyBelum ada peringkat

- Humss 125 Week 1 20 by Ramon 2Dokumen240 halamanHumss 125 Week 1 20 by Ramon 2Francis Esperanza88% (17)

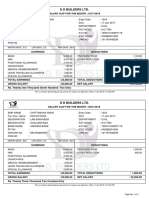

- Pay - Slip Oct. & Nov. 19Dokumen1 halamanPay - Slip Oct. & Nov. 19Atul Kumar MishraBelum ada peringkat

- Barclays Capital - The - W - Ides of MarchDokumen59 halamanBarclays Capital - The - W - Ides of MarchjonnathannBelum ada peringkat

- Corporation Law - Atty. Zarah Villanueva (Case List)Dokumen3 halamanCorporation Law - Atty. Zarah Villanueva (Case List)leizzhyBelum ada peringkat

- Hong, P. and Kwon, H.B., 2012. Emerging Issues of Procurement Management A Review and Prospect. International Journal of Procurement Management 4, 5 (4), pp.452-469.Dokumen19 halamanHong, P. and Kwon, H.B., 2012. Emerging Issues of Procurement Management A Review and Prospect. International Journal of Procurement Management 4, 5 (4), pp.452-469.Anonymous BJNqtknBelum ada peringkat

- ERP Functions and Historical PerspectivesDokumen26 halamanERP Functions and Historical PerspectivesShriyanshi JaitlyBelum ada peringkat

- Edelweiss Mutual-Funds Demo - CompressedDokumen38 halamanEdelweiss Mutual-Funds Demo - CompressedShriyanshi JaitlyBelum ada peringkat

- EIS Past Present and FutureDokumen18 halamanEIS Past Present and FutureShriyanshi JaitlyBelum ada peringkat

- 2 Types Insurance PoliciesDokumen10 halaman2 Types Insurance PoliciesShriyanshi JaitlyBelum ada peringkat

- ERP CoursePlanDokumen2 halamanERP CoursePlanShriyanshi JaitlyBelum ada peringkat

- Unit 2 Derivatives IncDokumen97 halamanUnit 2 Derivatives IncShriyanshi JaitlyBelum ada peringkat

- 1 BasicPrinciplesInsuranceDokumen24 halaman1 BasicPrinciplesInsuranceShriyanshi JaitlyBelum ada peringkat

- Forward Rate Agreement (FRA)Dokumen3 halamanForward Rate Agreement (FRA)Shriyanshi JaitlyBelum ada peringkat

- No Frills AccountDokumen1 halamanNo Frills AccountShriyanshi Jaitly100% (1)

- 1 BasicPrinciplesInsuranceDokumen24 halaman1 BasicPrinciplesInsuranceShriyanshi JaitlyBelum ada peringkat

- 7 CMA Format NewDokumen33 halaman7 CMA Format NewShriyanshi JaitlyBelum ada peringkat

- Lva1 App6892Dokumen28 halamanLva1 App6892Shriyanshi JaitlyBelum ada peringkat

- CI Principles of MacroeconomicsDokumen454 halamanCI Principles of MacroeconomicsHoury GostanianBelum ada peringkat

- 6021-P3-Lembar KerjaDokumen48 halaman6021-P3-Lembar KerjaikhwanBelum ada peringkat

- Risk Assessment For Grinding Work: Classic Builders and DevelopersDokumen3 halamanRisk Assessment For Grinding Work: Classic Builders and DevelopersradeepBelum ada peringkat

- 2022-11-13 2bat TDR Francesc MorenoDokumen76 halaman2022-11-13 2bat TDR Francesc MorenoFrancesc Moreno MorataBelum ada peringkat

- The End of Japanese-Style ManagementDokumen24 halamanThe End of Japanese-Style ManagementThanh Tung NguyenBelum ada peringkat

- Trade For Corporates OverviewDokumen47 halamanTrade For Corporates OverviewZayd Iskandar Dzolkarnain Al-HadramiBelum ada peringkat

- Using Operations To Create Value Nama: Muhamad Syaeful Anwar NIM: 432910Dokumen1 halamanUsing Operations To Create Value Nama: Muhamad Syaeful Anwar NIM: 432910MuhamadSyaefulAnwarBelum ada peringkat

- The Communistic Societies of The United StatesFrom Personal Visit and Observation by Nordhoff, Charles, 1830-1901Dokumen263 halamanThe Communistic Societies of The United StatesFrom Personal Visit and Observation by Nordhoff, Charles, 1830-1901Gutenberg.org100% (2)

- Funskool Case Study - Group 3Dokumen7 halamanFunskool Case Study - Group 3Megha MarwariBelum ada peringkat

- Mortgage 2 PDFDokumen5 halamanMortgage 2 PDFClerry SamuelBelum ada peringkat

- BlackBuck Looks To Disrupt B2B Logistics Market Apart From The Regular GPS-Enabled Freight Management, It Offers Features Such As Track and Trace, Truck Mapping - The Financial ExpressDokumen2 halamanBlackBuck Looks To Disrupt B2B Logistics Market Apart From The Regular GPS-Enabled Freight Management, It Offers Features Such As Track and Trace, Truck Mapping - The Financial ExpressPrashant100% (1)

- Mill Test Certificate: Run Date 21/12/2021 OR0019M - JAZ User ID E1037Dokumen1 halamanMill Test Certificate: Run Date 21/12/2021 OR0019M - JAZ User ID E1037RakeshParikhBelum ada peringkat

- World Bank Review Global AsiaDokumen5 halamanWorld Bank Review Global AsiaRadhakrishnanBelum ada peringkat

- Cargo MarDokumen6 halamanCargo MarJayadev S RBelum ada peringkat

- Activity 2 Applied Economics March 12 2024Dokumen1 halamanActivity 2 Applied Economics March 12 2024nadinebayransamonte02Belum ada peringkat

- IAS 2 InventoriesDokumen13 halamanIAS 2 InventoriesFritz MainarBelum ada peringkat

- Finance Process & Terms & ConditionsDokumen3 halamanFinance Process & Terms & ConditionsPalash PatankarBelum ada peringkat

- Difference Between EPF GPF & PPFDokumen3 halamanDifference Between EPF GPF & PPFSrikanth VsrBelum ada peringkat

- G20 Leaders to Agree on Trade, CurrencyDokumen5 halamanG20 Leaders to Agree on Trade, CurrencysunitbagadeBelum ada peringkat

- BankingDokumen99 halamanBankingNamrata KulkarniBelum ada peringkat

- Data Analysis of a Fabric Production JobDokumen3 halamanData Analysis of a Fabric Production Job孙诚0% (2)

- Rethinking Monetary Policy After the CrisisDokumen23 halamanRethinking Monetary Policy After the CrisisAlexDuarteVelasquezBelum ada peringkat

- Lecture Var SignrestrictionDokumen41 halamanLecture Var SignrestrictionTrang DangBelum ada peringkat