Anda mungkin juga menyukai

- SSDTDokumen1 halamanSSDTCeejay RosalesBelum ada peringkat

- Fill in The Blanks Business PlanDokumen19 halamanFill in The Blanks Business Plandarius318Belum ada peringkat

- Term1 Yr 11 BusinessDokumen12 halamanTerm1 Yr 11 BusinessayyazBelum ada peringkat

- Exercises and Problems - Merchandising BusinessDokumen4 halamanExercises and Problems - Merchandising BusinessNems PsycheBelum ada peringkat

- Payroll Format 1Dokumen1 halamanPayroll Format 1Synchrotek CorporationBelum ada peringkat

- SBIapplicationformDokumen5 halamanSBIapplicationformSufi DarweshBelum ada peringkat

- 0930-BH-BAF-19 Sem #8 Fee ChallanDokumen1 halaman0930-BH-BAF-19 Sem #8 Fee Challanmuhammad sajjadBelum ada peringkat

- 202 Things You Can Buy and Sell For Big Profits - James StephensonDokumen344 halaman202 Things You Can Buy and Sell For Big Profits - James StephensonKhôi PhanBelum ada peringkat

- Add 51 BFDokumen193 halamanAdd 51 BFMagedBelum ada peringkat

- MGT120 - Review: The Tutorial Is A Review Only and Not An Indication of What Will Be On The TestDokumen6 halamanMGT120 - Review: The Tutorial Is A Review Only and Not An Indication of What Will Be On The TestRaghav SharmaBelum ada peringkat

- Home Task 1: Important Accounting TermsDokumen3 halamanHome Task 1: Important Accounting TermsMalik Talha AhmadBelum ada peringkat

- FABMDokumen2 halamanFABMTinBelum ada peringkat

- Bank StatementDokumen3 halamanBank Statementsaravanan_sfp100% (1)

- Revised Company Loan FormDokumen2 halamanRevised Company Loan FormAubrey UbayBelum ada peringkat

- Home Task 2: Important Accounting PrinciplesDokumen2 halamanHome Task 2: Important Accounting PrinciplesMalik Talha AhmadBelum ada peringkat

- BP B1 Tests Unit4 LCCIDokumen1 halamanBP B1 Tests Unit4 LCCIthư lêBelum ada peringkat

- Handouts CVP AnalysisDokumen6 halamanHandouts CVP AnalysisAissa OrbitaBelum ada peringkat

- Fabm1 Module 6Dokumen20 halamanFabm1 Module 6Randy Magbudhi100% (4)

- 312 WorksheetDokumen24 halaman312 WorksheetPeter MasoesBelum ada peringkat

- ASAP Business BlueprintDokumen670 halamanASAP Business BlueprintidevaldoBelum ada peringkat

- Bond Application-CorporationDokumen5 halamanBond Application-CorporationDaniel BuenafeBelum ada peringkat

- Bond Application CorporationDokumen3 halamanBond Application Corporationdataprotection.puicBelum ada peringkat

- Acctg 13Dokumen23 halamanAcctg 13Fatima ZaharaBelum ada peringkat

- FABM 2 - Midterm ExamDokumen6 halamanFABM 2 - Midterm ExamJessica Esmeña100% (1)

- Economic SurveyDokumen4 halamanEconomic SurveyPAPAGRAND MOVERS CORP.Belum ada peringkat

- FABM2 Quarter 1 Module and WorksheetsDokumen27 halamanFABM2 Quarter 1 Module and WorksheetsHeart polvos100% (1)

- Application Form MPSSIRS 2014Dokumen5 halamanApplication Form MPSSIRS 2014Ar Raj YamgarBelum ada peringkat

- Cashier'S Report: Pares Retiro Food CorporationDokumen2 halamanCashier'S Report: Pares Retiro Food CorporationMaricel CamachoBelum ada peringkat

- CHAPTERS 1& 2 Class ExeerciseDokumen4 halamanCHAPTERS 1& 2 Class ExeerciseBigAsianPapiBelum ada peringkat

- PQR Limited-Depreciation AccountingDokumen1 halamanPQR Limited-Depreciation AccountingSakshi SodhiBelum ada peringkat

- Add 50Dokumen228 halamanAdd 50MagedBelum ada peringkat

- Notes: Eastern Silk Industries LTDDokumen30 halamanNotes: Eastern Silk Industries LTDNaveen KumarBelum ada peringkat

- 2019 June 03 Chapter 2 Problems and SolutionDokumen23 halaman2019 June 03 Chapter 2 Problems and SolutionZisanBelum ada peringkat

- Leave Conversion FormDokumen1 halamanLeave Conversion FormLorraine CuribBelum ada peringkat

- 1002-BH-ECON-19 Sem #8 Fee ChallanDokumen1 halaman1002-BH-ECON-19 Sem #8 Fee ChallanKhan XadaBelum ada peringkat

- Ley1116 TesisDokumen41 halamanLey1116 TesisAngelicaOrozcoBelum ada peringkat

- BSA1B Activity 1Dokumen2 halamanBSA1B Activity 1ShorinBelum ada peringkat

- Accounting Journalizing ProblemDokumen3 halamanAccounting Journalizing ProblemPHEGIEL MAGAMAYBelum ada peringkat

- 2372-BH-PHE-19 Sem #8 Fee ChallanDokumen1 halaman2372-BH-PHE-19 Sem #8 Fee ChallanNoor Warsi KhanBelum ada peringkat

- Vendors Pre-Qualification FormDokumen2 halamanVendors Pre-Qualification FormHaroon AhmedBelum ada peringkat

- Retiree Request Form OR NoDokumen1 halamanRetiree Request Form OR NoFranco SalazarBelum ada peringkat

- Budget Request Form - PACUCOA Defrayment of Publication CostDokumen1 halamanBudget Request Form - PACUCOA Defrayment of Publication CostIan PalmaBelum ada peringkat

- Chapter 3/unit 4 Review Sheet 4/preparing The Income StatementDokumen2 halamanChapter 3/unit 4 Review Sheet 4/preparing The Income Statementkamaljeet kaurBelum ada peringkat

- Accounting Terms RevisionDokumen3 halamanAccounting Terms Revisionbrandon.dube2026Belum ada peringkat

- Assignment 02Dokumen2 halamanAssignment 02Vincent CapulongBelum ada peringkat

- Review Center Interview QuestionsDokumen6 halamanReview Center Interview QuestionsDcimasaBelum ada peringkat

- Rmo03 03anxaDokumen1 halamanRmo03 03anxaMario AgoncilloBelum ada peringkat

- Assignment 2 Barilla Submit b4 2400 19.10.2022Dokumen5 halamanAssignment 2 Barilla Submit b4 2400 19.10.2022Ka Ki LauBelum ada peringkat

- Sample Requisition SlipDokumen1 halamanSample Requisition SlipRhea CalooyBelum ada peringkat

- Tax Law Sumary NotesDokumen72 halamanTax Law Sumary Notesannpurna pathakBelum ada peringkat

- Airtel Money QuizDokumen2 halamanAirtel Money QuizOmyjayd KeBelum ada peringkat

- Companies and Intellectual Property Commission Republic of South Africa - Form Cor 14.1Dokumen1 halamanCompanies and Intellectual Property Commission Republic of South Africa - Form Cor 14.1Lefa Doctormann RalethohlaneBelum ada peringkat

- The Stress-Free Guide to Parenting a Child With ADHD: Effective and Proven Strategies for Alleviating Anxiety and Forming Strong Bonds Without the HassleDari EverandThe Stress-Free Guide to Parenting a Child With ADHD: Effective and Proven Strategies for Alleviating Anxiety and Forming Strong Bonds Without the HassleBelum ada peringkat

- Hacking for Beginners: Comprehensive Guide on Hacking Websites, Smartphones, Wireless Networks, Conducting Social Engineering, Performing a Penetration Test, and Securing Your Network (2022)Dari EverandHacking for Beginners: Comprehensive Guide on Hacking Websites, Smartphones, Wireless Networks, Conducting Social Engineering, Performing a Penetration Test, and Securing Your Network (2022)Belum ada peringkat

- Tools to Beat Budget - A Proven Program for Club PerformanceDari EverandTools to Beat Budget - A Proven Program for Club PerformanceBelum ada peringkat

- Clinton Iraq EmailDokumen4 halamanClinton Iraq EmailandrewperezdcBelum ada peringkat

- Paper 16Dokumen71 halamanPaper 16pkaul1Belum ada peringkat

- Capital, Property, and FundsDokumen5 halamanCapital, Property, and FundsRichard Lee Gines100% (1)

- Banking-Law-Mid NotesDokumen11 halamanBanking-Law-Mid NotesVince Clarck F. AñabiezaBelum ada peringkat

- FABM-1 Summary ExaminationDokumen7 halamanFABM-1 Summary ExaminationSheldon Bazinga67% (3)

- Excerpt TCS Business Process Outsourcing Services: in Pursuit of ExcellenceDokumen23 halamanExcerpt TCS Business Process Outsourcing Services: in Pursuit of ExcellencenikitajoseBelum ada peringkat

- Deposist AccountDokumen6 halamanDeposist AccountwaheedarifBelum ada peringkat

- Zaid Ahmad PDFDokumen1 halamanZaid Ahmad PDFzaidBelum ada peringkat

- Union BankDokumen2 halamanUnion Bankvignesh ACSBelum ada peringkat

- Hotel Details Check in Check Out Rooms: Guest Name: DateDokumen1 halamanHotel Details Check in Check Out Rooms: Guest Name: DatevickyBelum ada peringkat

- 1allianz PDFDokumen26 halaman1allianz PDFFarah Najeehah ZolkalpliBelum ada peringkat

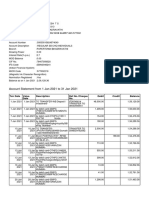

- Account Statement From 1 Jan 2021 To 31 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen2 halamanAccount Statement From 1 Jan 2021 To 31 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancevenkBelum ada peringkat

- Bank AccountDokumen3 halamanBank AccountIshrat KhanBelum ada peringkat

- Meeting ChecklistDokumen11 halamanMeeting ChecklistYogesh ChhaprooBelum ada peringkat

- Ross4ppt ch19Dokumen36 halamanRoss4ppt ch19씨나젬Belum ada peringkat

- MBA Finance ProjectDokumen73 halamanMBA Finance Projectsabaris477Belum ada peringkat

- Bus Law Mcqs 2016Dokumen6 halamanBus Law Mcqs 2016Anonymous 03JIPKRkBelum ada peringkat

- Chapter 1-5Dokumen46 halamanChapter 1-5Mohammed Abu ShaibuBelum ada peringkat

- Model ContractDokumen9 halamanModel ContractBren SanCorBelum ada peringkat

- 21 Edillon V Manila Bankers Life Insurance CorporationDokumen2 halaman21 Edillon V Manila Bankers Life Insurance CorporationVia Monina ValdepeñasBelum ada peringkat

- Merger Report of HDFC-CBOP by Atmakuri RammohanDokumen23 halamanMerger Report of HDFC-CBOP by Atmakuri RammohanRam Mohan Atmakuri100% (21)

- PNBONE Mpassbook 114911 5-5-2023 28-11-2023 1780XXXXXXXX83Dokumen5 halamanPNBONE Mpassbook 114911 5-5-2023 28-11-2023 1780XXXXXXXX83jattkhatri4Belum ada peringkat

- Bitcoin Investment Trust Spencer NeedhamDokumen8 halamanBitcoin Investment Trust Spencer NeedhamPete Rizzo100% (1)

- Signature Elpiniki Bechakas On Assignment RoboDokumen3 halamanSignature Elpiniki Bechakas On Assignment RoboRichard A. Guttman100% (1)

- Case Study SipDokumen3 halamanCase Study SipVikashBelum ada peringkat

- Audit of Cash and Cash EquivalentsDokumen2 halamanAudit of Cash and Cash EquivalentsJhedz Cartas0% (1)

- Non Resident Account: Tax InvoiceDokumen2 halamanNon Resident Account: Tax InvoiceEmanuelsön Caverä BreezÿBelum ada peringkat

- January 2020Dokumen100 halamanJanuary 2020ICCFA StaffBelum ada peringkat

- Accounts Finalization of PL and Bs StepsDokumen5 halamanAccounts Finalization of PL and Bs StepsKhalid MahmoodBelum ada peringkat

- Loan Amortization Calculation: Sonali Bank Bangabandhu Avenue BranchDokumen2 halamanLoan Amortization Calculation: Sonali Bank Bangabandhu Avenue BranchsagarsbhBelum ada peringkat