Anda mungkin juga menyukai

- Tax BillDokumen1 halamanTax BillBrenda SorensonBelum ada peringkat

- Financial Modeling by Corporate BriddgeDokumen55 halamanFinancial Modeling by Corporate BriddgecorporatebridgeBelum ada peringkat

- 4 Memorandum of AssociationDokumen38 halaman4 Memorandum of Associationkhuranaamanpreet7gmailcom100% (1)

- Starbucks Corporation Analysis Executive SummaryDokumen32 halamanStarbucks Corporation Analysis Executive Summarylarry_forsberg100% (4)

- Ratio Analysis ProjectDokumen65 halamanRatio Analysis Projectshivap13210% (1)

- Introduction To Cost AccountingDokumen2 halamanIntroduction To Cost AccountingHunson AbadeerBelum ada peringkat

- Delpher Trades Corp v. IACDokumen2 halamanDelpher Trades Corp v. IACkfv05100% (3)

- A Study On Nri Banking Services in IndiaDokumen55 halamanA Study On Nri Banking Services in IndiaJayanti KappalBelum ada peringkat

- Types of SharesDokumen9 halamanTypes of SharesArnav bharadiaBelum ada peringkat

- Impact of GST On Retail Business With Repect To Airoli, Maharashtra PDFDokumen91 halamanImpact of GST On Retail Business With Repect To Airoli, Maharashtra PDFOmkar PatoleBelum ada peringkat

- Stock Market and Indian EconomyDokumen62 halamanStock Market and Indian Economyswapnilr85Belum ada peringkat

- Money Market in India: A Project Report ONDokumen35 halamanMoney Market in India: A Project Report ONLovely SharmaBelum ada peringkat

- Topic: Leadership Style in Banking Sector: Presented byDokumen17 halamanTopic: Leadership Style in Banking Sector: Presented byPriyanshi TalesraBelum ada peringkat

- A Presentation On HR Policies : Singh Ankit Jitendra Sristi Biswas Vivek KumarDokumen9 halamanA Presentation On HR Policies : Singh Ankit Jitendra Sristi Biswas Vivek KumarAnkit SinghBelum ada peringkat

- Assessment of Tax For FirmsDokumen18 halamanAssessment of Tax For FirmsOrko AbirBelum ada peringkat

- Impact of GST On WholesellerDokumen59 halamanImpact of GST On Wholesellermovie latest kadamBelum ada peringkat

- Working Capital Management of SectrixDokumen50 halamanWorking Capital Management of SectrixsectrixBelum ada peringkat

- Analysis of Indian Debt MarketDokumen45 halamanAnalysis of Indian Debt Marketmichelle_susan_dsa100% (1)

- Dayrit v. CA DigestDokumen3 halamanDayrit v. CA DigestJosh BersaminaBelum ada peringkat

- Bombay Mercantile Co-Operative Bank LTDDokumen78 halamanBombay Mercantile Co-Operative Bank LTDaadil shaikhBelum ada peringkat

- Part II Audit ProjecDokumen36 halamanPart II Audit ProjecSagar Zine100% (1)

- Amalgamation of CompaniesDokumen8 halamanAmalgamation of CompaniesVikram NaniBelum ada peringkat

- The Indian Partnership Act, 1932Dokumen17 halamanThe Indian Partnership Act, 1932Engineer100% (1)

- Innovations in InsuranceDokumen47 halamanInnovations in InsuranceDouglas StoneBelum ada peringkat

- Project On HDFC BankDokumen67 halamanProject On HDFC BankAarti YadavBelum ada peringkat

- A Case Study On The Corporate Social Responsibility of The Selected Indian CompaniesDokumen55 halamanA Case Study On The Corporate Social Responsibility of The Selected Indian CompaniesRohit KerkarBelum ada peringkat

- CRM Complete ProjectDokumen61 halamanCRM Complete ProjectPratik GosaviBelum ada peringkat

- "Merger and Consolidation of Icici Ltd. and Icici Bank": A Project Report ONDokumen90 halaman"Merger and Consolidation of Icici Ltd. and Icici Bank": A Project Report ONRidhima SharmaBelum ada peringkat

- Amalgamation of Firms ProjectDokumen5 halamanAmalgamation of Firms ProjectkalaswamiBelum ada peringkat

- Difference Between Entrepreneur and ManagerDokumen7 halamanDifference Between Entrepreneur and ManagerSantosh ChaudharyBelum ada peringkat

- Ind As 1Dokumen64 halamanInd As 1vijaykumartaxBelum ada peringkat

- Effect of Stock Market On Indian EconomyDokumen28 halamanEffect of Stock Market On Indian Economyanshu009767% (3)

- Recent Trend in New Issue MarketDokumen14 halamanRecent Trend in New Issue MarketAbhi SinhaBelum ada peringkat

- A Study The Compatative of Income Tax For Partnership Firm With Reference To KDMC AreaDokumen49 halamanA Study The Compatative of Income Tax For Partnership Firm With Reference To KDMC AreaTasmay EnterprisesBelum ada peringkat

- Dena BankDokumen25 halamanDena BankJaved ShaikhBelum ada peringkat

- Marketing of Financial ServicesDokumen43 halamanMarketing of Financial ServicesSaiparesh Walawalkar100% (1)

- Article On Financial PlanningDokumen16 halamanArticle On Financial PlanningShyam KumarBelum ada peringkat

- Functions of Asset Management CompanyDokumen4 halamanFunctions of Asset Management CompanyAayushi PatelBelum ada peringkat

- ON "A Study On Investment Pattern of Women Investors In: DissertationDokumen50 halamanON "A Study On Investment Pattern of Women Investors In: DissertationKrishna Sharma100% (1)

- A Study On Risk and Return Analysis of Selected FMCGDokumen13 halamanA Study On Risk and Return Analysis of Selected FMCGKavya posanBelum ada peringkat

- Project ReportDokumen53 halamanProject ReportAbhishek MishraBelum ada peringkat

- A Study On Receivable Management & Its ImpactDokumen70 halamanA Study On Receivable Management & Its Impactlmbhagya100% (2)

- CRM in BankDokumen78 halamanCRM in BankSaurabh MaheshwariBelum ada peringkat

- Comparative Analysis of SHAREKHAN and Other Stock Broker HouseDokumen78 halamanComparative Analysis of SHAREKHAN and Other Stock Broker Housedishank jain0% (1)

- Non Performing AssetsDokumen11 halamanNon Performing AssetssudheerBelum ada peringkat

- Sbi Mutual FundDokumen44 halamanSbi Mutual FundUtkarsh NolkhaBelum ada peringkat

- International Financial Reporting StandardsDokumen31 halamanInternational Financial Reporting StandardsKewal GalaBelum ada peringkat

- A Study of Factors Influencing The Consumer Behavior Towards Direct Selling Companies With Special Reference To RCM Products1Dokumen78 halamanA Study of Factors Influencing The Consumer Behavior Towards Direct Selling Companies With Special Reference To RCM Products1Anil kadamBelum ada peringkat

- The Narasimham CommitteeDokumen18 halamanThe Narasimham CommitteeParul SaxenaBelum ada peringkat

- CAclubindia News - Managerial Remuneration (In A Simple Way) PDFDokumen3 halamanCAclubindia News - Managerial Remuneration (In A Simple Way) PDFVivek ReddyBelum ada peringkat

- Institute of Management, Nirma University: Group Assignment-Reliance Power's IPODokumen7 halamanInstitute of Management, Nirma University: Group Assignment-Reliance Power's IPOCJKBelum ada peringkat

- An Overview of Financial SystemDokumen6 halamanAn Overview of Financial SystemAshwani BhallaBelum ada peringkat

- Project On Working Capital ManagementDokumen59 halamanProject On Working Capital ManagementMotasim ParkarBelum ada peringkat

- Comperative Analysis of Products & Services of Axis Bank Wiith Its Competitors Ayushi AgarwalDokumen62 halamanComperative Analysis of Products & Services of Axis Bank Wiith Its Competitors Ayushi AgarwalAnonymous CUwjARBelum ada peringkat

- Mergers Indian Banking Sector AluminiDokumen72 halamanMergers Indian Banking Sector AluminiAvinash Pal SuryavanshiBelum ada peringkat

- India's Balance of Payments Crisis and It's ImpactsDokumen62 halamanIndia's Balance of Payments Crisis and It's ImpactsAkhil RupaniBelum ada peringkat

- Depository System in IndiaDokumen19 halamanDepository System in IndiaAlisha GuptaBelum ada peringkat

- Black Book 05Dokumen68 halamanBlack Book 05vishal vhatkarBelum ada peringkat

- The Four Walls: Live Like the Wind, Free, Without HindrancesDari EverandThe Four Walls: Live Like the Wind, Free, Without HindrancesPenilaian: 5 dari 5 bintang5/5 (1)

- Green Products A Complete Guide - 2020 EditionDari EverandGreen Products A Complete Guide - 2020 EditionPenilaian: 5 dari 5 bintang5/5 (1)

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorDari EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorBelum ada peringkat

- Chapter - 1: Meaning and DefinitionDokumen12 halamanChapter - 1: Meaning and DefinitionShilpa S RaoBelum ada peringkat

- Amalgmation, Absorbtion, External ReconstructionDokumen9 halamanAmalgmation, Absorbtion, External Reconstructionpijiyo78Belum ada peringkat

- AmalgamationDokumen41 halamanAmalgamationZooBelum ada peringkat

- 5) Amalgamation of CompaniesDokumen82 halaman5) Amalgamation of CompaniesShiv ShivBelum ada peringkat

- 74719bos60485 Inter p1 cp13Dokumen92 halaman74719bos60485 Inter p1 cp13Aniruddh SoniBelum ada peringkat

- Amalgmation of CompanyDokumen83 halamanAmalgmation of CompanySuryaBelum ada peringkat

- Summer Training ReportDokumen21 halamanSummer Training Reportkhuranaamanpreet7gmailcomBelum ada peringkat

- Success Solutions Care: WelcomeDokumen7 halamanSuccess Solutions Care: Welcomekhuranaamanpreet7gmailcomBelum ada peringkat

- 1 To 10 (All Subjects) +1, +2 Commerce, Arts (All Subjects)Dokumen1 halaman1 To 10 (All Subjects) +1, +2 Commerce, Arts (All Subjects)khuranaamanpreet7gmailcomBelum ada peringkat

- Solved Long Division Problems With Step-By-Step Walkthrough: Solutions Are On Page 2Dokumen2 halamanSolved Long Division Problems With Step-By-Step Walkthrough: Solutions Are On Page 2khuranaamanpreet7gmailcomBelum ada peringkat

- Aman Unit 4Dokumen50 halamanAman Unit 4khuranaamanpreet7gmailcomBelum ada peringkat

- Aman Unit 4Dokumen81 halamanAman Unit 4khuranaamanpreet7gmailcomBelum ada peringkat

- Trade UnionDokumen8 halamanTrade Unionkhuranaamanpreet7gmailcomBelum ada peringkat

- Collective BargainingDokumen27 halamanCollective Bargainingkhuranaamanpreet7gmailcomBelum ada peringkat

- Payment of Gratuity Act 1972Dokumen15 halamanPayment of Gratuity Act 1972khuranaamanpreet7gmailcomBelum ada peringkat

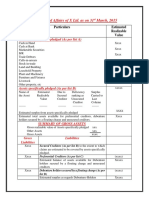

- Statement of Affairs-1Dokumen5 halamanStatement of Affairs-1khuranaamanpreet7gmailcomBelum ada peringkat

- Statement of AffairsDokumen2 halamanStatement of Affairskhuranaamanpreet7gmailcom100% (1)

- Holding and Subsidiary CompaniesDokumen33 halamanHolding and Subsidiary Companieskhuranaamanpreet7gmailcomBelum ada peringkat

- PD 1034 - Offshore BankingDokumen5 halamanPD 1034 - Offshore BankingSZBelum ada peringkat

- 1.guess Questions - Theory - Questions and AnswersDokumen44 halaman1.guess Questions - Theory - Questions and AnswersKrishnaKorada100% (14)

- Respondents Memorial - RDokumen37 halamanRespondents Memorial - RNiteshMaheshwariBelum ada peringkat

- Steve Advanced Courses Part 3Dokumen16 halamanSteve Advanced Courses Part 3Manuel NadeauBelum ada peringkat

- VIX As A PredictorInsightsDokumen9 halamanVIX As A PredictorInsightsSandipBelum ada peringkat

- Financial Transcations Analysis: Under The Guidance of Dr. Nisha ShankarDokumen4 halamanFinancial Transcations Analysis: Under The Guidance of Dr. Nisha ShankarRUTVIKA DHANESHKUMARKUNDAGOLBelum ada peringkat

- 94dd PATH Basemap 2023 12 FINALDokumen1 halaman94dd PATH Basemap 2023 12 FINALeoin01Belum ada peringkat

- The Role, History, and Direction of Management AccountingDokumen18 halamanThe Role, History, and Direction of Management AccountingRavi DesaiBelum ada peringkat

- Ug Scholarships at Iit KGPDokumen5 halamanUg Scholarships at Iit KGPPriyank AgrawalBelum ada peringkat

- Resume Jurnal AdelDokumen5 halamanResume Jurnal AdelMuhamad SyarifBelum ada peringkat

- FM12 CH 02 ShowDokumen88 halamanFM12 CH 02 ShowIbrahim AbdallahBelum ada peringkat

- BA 114.1 - Module2 - Receivables - Exercise 1 PDFDokumen4 halamanBA 114.1 - Module2 - Receivables - Exercise 1 PDFKurt Orfanel0% (1)

- Mega Lifesciences Mega TB: Growing in ASEANDokumen12 halamanMega Lifesciences Mega TB: Growing in ASEANAshokBelum ada peringkat

- Lobal Investments: Discover Your Real Cost of Capital-And Your Real RiskDokumen6 halamanLobal Investments: Discover Your Real Cost of Capital-And Your Real RiskAdamSmith1990Belum ada peringkat

- Insurance and Risk Management AssignmentDokumen14 halamanInsurance and Risk Management AssignmentKazi JunayadBelum ada peringkat

- AMUL Case Study in Context of Financial Management, Cost and Management Accounting, Production & Operation ManagementDokumen26 halamanAMUL Case Study in Context of Financial Management, Cost and Management Accounting, Production & Operation ManagementtwinkalBelum ada peringkat

- Create Scan Old Candlestick P&F Realtime & Alerts WatchlistsDokumen5 halamanCreate Scan Old Candlestick P&F Realtime & Alerts WatchlistsSushobhan DasBelum ada peringkat

- VCF Stock AnalysisDokumen36 halamanVCF Stock Analysisruh cinBelum ada peringkat

- Csis Scheme2Dokumen1 halamanCsis Scheme2Gopalakrishnan KBelum ada peringkat

- Saturn Retrograde Will Trigger Global RecessionDokumen26 halamanSaturn Retrograde Will Trigger Global RecessionmichaBelum ada peringkat

- Chapter 7 - Dynamics of Financial Crises in Emerging Economies and ApplicationsDokumen49 halamanChapter 7 - Dynamics of Financial Crises in Emerging Economies and ApplicationsJane KotaishBelum ada peringkat

- City-Sample Copy of BbaDokumen25 halamanCity-Sample Copy of BbaKuldeep ShuklaBelum ada peringkat

- FA1 Basic MCQsDokumen8 halamanFA1 Basic MCQsamir100% (3)

- From Disaster To Diversity: What's Next For New York City's Economy?Dokumen81 halamanFrom Disaster To Diversity: What's Next For New York City's Economy?Drum Major InstituteBelum ada peringkat