Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Banned Occult Secrets of the Vril SocietyDokumen8 halamanBanned Occult Secrets of the Vril SocietyShoniqua Johnson75% (4)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- 24 Directions of Feng ShuiDokumen9 halaman24 Directions of Feng Shuitoml88Belum ada peringkat

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Ngo Burca Vs RP DigestDokumen1 halamanNgo Burca Vs RP DigestIvy Paz100% (1)

- AWS D14.1 - 1997 Specification For Welding of Industrial and Mill Crane and Material Handling EqDokumen141 halamanAWS D14.1 - 1997 Specification For Welding of Industrial and Mill Crane and Material Handling EqRicardo Contzen Rigo-Righi50% (2)

- Apollo 11tech Crew DebriefDokumen467 halamanApollo 11tech Crew DebriefBob AndrepontBelum ada peringkat

- Special Educational Needs, Inclusion and DiversityDokumen665 halamanSpecial Educational Needs, Inclusion and DiversityAndrej Hodonj100% (1)

- How K P Pinpoint Events Prasna PDFDokumen129 halamanHow K P Pinpoint Events Prasna PDFRavindra ChandelBelum ada peringkat

- VA 2010 2014 Strategic PlanDokumen112 halamanVA 2010 2014 Strategic PlanmaxwizeBelum ada peringkat

- Eep306 Assessment 1 FeedbackDokumen2 halamanEep306 Assessment 1 Feedbackapi-354631612Belum ada peringkat

- Construct Basic Sentence in TagalogDokumen7 halamanConstruct Basic Sentence in TagalogXamm4275 SamBelum ada peringkat

- Audit of Allocations to LGUsDokumen7 halamanAudit of Allocations to LGUsRhuejane Gay MaquilingBelum ada peringkat

- Fe en Accion - Morris VendenDokumen734 halamanFe en Accion - Morris VendenNicolas BertoaBelum ada peringkat

- Foreign Interference in US ElectionsDokumen21 halamanForeign Interference in US Electionswmartin46Belum ada peringkat

- US Veterans Affairs 2013 Annual ReportDokumen338 halamanUS Veterans Affairs 2013 Annual Reportwmartin46Belum ada peringkat

- Researching WWII and Military HistoryDokumen15 halamanResearching WWII and Military Historywmartin46Belum ada peringkat

- Online Genealogical Search For Missing WWII GIs.Dokumen15 halamanOnline Genealogical Search For Missing WWII GIs.wmartin46Belum ada peringkat

- Comments To Palo Alto (CA) City Council About Public Records Requests ProcessingDokumen7 halamanComments To Palo Alto (CA) City Council About Public Records Requests Processingwmartin46Belum ada peringkat

- TFS Healthcare Resource File #1Dokumen8 halamanTFS Healthcare Resource File #1wmartin46Belum ada peringkat

- Pension Basics - Relationship Between Salaries and Pensions in Palo Alto, CADokumen13 halamanPension Basics - Relationship Between Salaries and Pensions in Palo Alto, CAwmartin46Belum ada peringkat

- City of Palo Alto Prioritization MatrixDokumen44 halamanCity of Palo Alto Prioritization Matrixwmartin46Belum ada peringkat

- Ad Encouraging A NO Vote To Measure E - Palo Alto TOT Tax Increase (2018)Dokumen1 halamanAd Encouraging A NO Vote To Measure E - Palo Alto TOT Tax Increase (2018)wmartin46Belum ada peringkat

- Researching in The Digital AgeDokumen8 halamanResearching in The Digital Agewmartin46Belum ada peringkat

- TFS Healthcare Resource File #3Dokumen12 halamanTFS Healthcare Resource File #3wmartin46Belum ada peringkat

- Pension Benefit Guarantee Corporation Report (PBGC) (2013)Dokumen54 halamanPension Benefit Guarantee Corporation Report (PBGC) (2013)wmartin46Belum ada peringkat

- Questions For Palo Alto City Council Candidates in Fall 2018 Election.Dokumen1 halamanQuestions For Palo Alto City Council Candidates in Fall 2018 Election.wmartin46Belum ada peringkat

- TFS Healthcare Resource File #2.Dokumen8 halamanTFS Healthcare Resource File #2.wmartin46Belum ada peringkat

- Friendly Fire: Death, Delay, and Dismay at The VADokumen124 halamanFriendly Fire: Death, Delay, and Dismay at The VAFedSmith Inc.Belum ada peringkat

- US Veterans Affairs 2014 2020 Strategic Plan DraftDokumen45 halamanUS Veterans Affairs 2014 2020 Strategic Plan Draftwmartin46Belum ada peringkat

- City of Palo Alto (CA) Housing Element Draft (2015-2023)Dokumen177 halamanCity of Palo Alto (CA) Housing Element Draft (2015-2023)wmartin46Belum ada peringkat

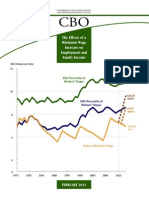

- The Effects of A Minimum-Wage Increase On Employment and Family IncomeDokumen43 halamanThe Effects of A Minimum-Wage Increase On Employment and Family IncomeJeffrey DunetzBelum ada peringkat

- Santa Clara County (CA) Grand Jury Report On Lack of Transparency in City of Palo Alto (CA) Government (May, 2014)Dokumen18 halamanSanta Clara County (CA) Grand Jury Report On Lack of Transparency in City of Palo Alto (CA) Government (May, 2014)wmartin46Belum ada peringkat

- Napa County (CA) Civil Grand Jury Report: A Review of County Public Employee Retirement Benefits (2014)Dokumen14 halamanNapa County (CA) Civil Grand Jury Report: A Review of County Public Employee Retirement Benefits (2014)wmartin46Belum ada peringkat

- VA Office of Inspector General Interim ReportDokumen35 halamanVA Office of Inspector General Interim ReportArthur BarieBelum ada peringkat

- News Articles From Regional California Newspapers About Palo Alto (CA) /stanford (1885-1922)Dokumen16 halamanNews Articles From Regional California Newspapers About Palo Alto (CA) /stanford (1885-1922)wmartin46Belum ada peringkat

- Law Suits Involving The City of Palo Alto (CA) From 1982 To The Present - Source: Santa Clara County Superior Court.Dokumen49 halamanLaw Suits Involving The City of Palo Alto (CA) From 1982 To The Present - Source: Santa Clara County Superior Court.wmartin46Belum ada peringkat

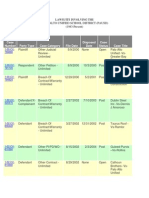

- Lawsuits Involving The Palo Alto Unified School District (PAUSD) (Palo Alto, CA) (1983-Present)Dokumen10 halamanLawsuits Involving The Palo Alto Unified School District (PAUSD) (Palo Alto, CA) (1983-Present)wmartin46Belum ada peringkat

- California Legislative Analyst's Office Presentation: Nonprofits Property Tax (2014)Dokumen8 halamanCalifornia Legislative Analyst's Office Presentation: Nonprofits Property Tax (2014)wmartin46Belum ada peringkat

- Center For Disease Control National Vital Statistics Reports: Births: Final Data For 2012Dokumen87 halamanCenter For Disease Control National Vital Statistics Reports: Births: Final Data For 2012wmartin46Belum ada peringkat

- California Student Suspension/Expulsion Data (2011-2012)Dokumen23 halamanCalifornia Student Suspension/Expulsion Data (2011-2012)wmartin46Belum ada peringkat

- Los Angeles 2020 Commission Report #1: A Time For Truth.Dokumen50 halamanLos Angeles 2020 Commission Report #1: A Time For Truth.wmartin46Belum ada peringkat

- 5 8 Pe Ola) CSL, E Quranic WondersDokumen280 halaman5 8 Pe Ola) CSL, E Quranic WondersMuhammad Faizan Raza Attari QadriBelum ada peringkat

- Iso Mps Least LearnedDokumen6 halamanIso Mps Least LearnedBon FreecsBelum ada peringkat

- IMRANADokumen4 halamanIMRANAAji MohammedBelum ada peringkat

- Taylor Swift Tagalig MemesDokumen34 halamanTaylor Swift Tagalig MemesAsa Zetterstrom McFly SwiftBelum ada peringkat

- 1Dokumen1 halaman1MariaMagubatBelum ada peringkat

- Bushnell / Companion To Tragedy 1405107359 - 4 - 001 Final Proof 8.2.2005 9:58amDokumen1 halamanBushnell / Companion To Tragedy 1405107359 - 4 - 001 Final Proof 8.2.2005 9:58amLeonelBatistaParenteBelum ada peringkat

- Irregular verbs guideDokumen159 halamanIrregular verbs guideIrina PadureanuBelum ada peringkat

- Client Portfolio Statement: %mkvalDokumen2 halamanClient Portfolio Statement: %mkvalMonjur MorshedBelum ada peringkat

- Online Applicaiton Regulations Under CQ (MBBS&BDS) ChangedDokumen23 halamanOnline Applicaiton Regulations Under CQ (MBBS&BDS) Changedyamini susmitha PBelum ada peringkat

- Applied Crypto HardeningDokumen111 halamanApplied Crypto Hardeningadr99Belum ada peringkat

- List of Presidents of Pakistan Since 1947 (With Photos)Dokumen4 halamanList of Presidents of Pakistan Since 1947 (With Photos)Humsafer ALiBelum ada peringkat

- AIS 10B TimetableDokumen1 halamanAIS 10B TimetableAhmed FadlallahBelum ada peringkat

- Website Vulnerability Scanner Report (Light)Dokumen6 halamanWebsite Vulnerability Scanner Report (Light)Stevi NangonBelum ada peringkat

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Dokumen6 halamanBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Doughty IncBelum ada peringkat

- Overtime Request Form 加班申请表: Last Name First NameDokumen7 halamanOvertime Request Form 加班申请表: Last Name First NameOlan PrinceBelum ada peringkat

- TallerDokumen102 halamanTallerMarie RodriguezBelum ada peringkat

- Management of HBLDokumen14 halamanManagement of HBLAnnaya AliBelum ada peringkat

- A Practical Guide To The 1999 Red & Yellow Books, Clause8-Commencement, Delays & SuspensionDokumen4 halamanA Practical Guide To The 1999 Red & Yellow Books, Clause8-Commencement, Delays & Suspensiontab77zBelum ada peringkat

- Case Study Format Hvco Srce UhvDokumen2 halamanCase Study Format Hvco Srce Uhvaayushjn290Belum ada peringkat