Anda mungkin juga menyukai

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)Dari EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)Belum ada peringkat

- Continuous Random Variables ExplainedDokumen39 halamanContinuous Random Variables ExplainedJose Leonardo Simancas GarciaBelum ada peringkat

- Tables of The Legendre Functions P—½+it(x): Mathematical Tables SeriesDari EverandTables of The Legendre Functions P—½+it(x): Mathematical Tables SeriesBelum ada peringkat

- TranscribeDokumen5 halamanTranscribeSoumyadip MondalBelum ada peringkat

- Random Signals: EE 524, Fall 2004, # 7 1Dokumen22 halamanRandom Signals: EE 524, Fall 2004, # 7 1Md. Mizanur RahmanBelum ada peringkat

- Section06 SolutionsDokumen15 halamanSection06 SolutionsMuhammad asafBelum ada peringkat

- Continuous Random Variables: Probability Distribution Function PDFDokumen2 halamanContinuous Random Variables: Probability Distribution Function PDFStrixBelum ada peringkat

- Indicator functions and expected values explainedDokumen10 halamanIndicator functions and expected values explainedPatricio Antonio VegaBelum ada peringkat

- Lecture 4-5-6 - Random VariablesDokumen29 halamanLecture 4-5-6 - Random Variablesalmeesbar opsBelum ada peringkat

- Random Variables: Presented by in Stochastic Analysis and Inverse ModellingDokumen21 halamanRandom Variables: Presented by in Stochastic Analysis and Inverse ModellingAndres Pino100% (1)

- Math 3215 Homework 3 Probability Distributions and StatisticsDokumen3 halamanMath 3215 Homework 3 Probability Distributions and StatisticsPei JingBelum ada peringkat

- Guide to Probability Theory ElementsDokumen12 halamanGuide to Probability Theory ElementsivanmrnBelum ada peringkat

- Section06 SolutionsDokumen11 halamanSection06 SolutionsKarimaBelum ada peringkat

- OptimalLinearFilters PDFDokumen107 halamanOptimalLinearFilters PDFAbdalmoedAlaiashyBelum ada peringkat

- Ma2261 Probability And Random Processes: ω: X (ω) ≤ x x ∈ RDokumen17 halamanMa2261 Probability And Random Processes: ω: X (ω) ≤ x x ∈ RSivabalanBelum ada peringkat

- Chebysev Inequality: Suppose and VarianceDokumen13 halamanChebysev Inequality: Suppose and VarianceMuthusivaramapandian MuthurajBelum ada peringkat

- Stat NotesDokumen14 halamanStat NotesTreanungkur MalBelum ada peringkat

- P2 SolDokumen24 halamanP2 SolTest EmailBelum ada peringkat

- Review-of-Random-VariablesDokumen8 halamanReview-of-Random-Variableselifeet123Belum ada peringkat

- PROBABILITY 03 Rv-Dist-Moments 5 8Dokumen21 halamanPROBABILITY 03 Rv-Dist-Moments 5 8DeepanshuBelum ada peringkat

- Engineering Mathematics II - RemovedDokumen90 halamanEngineering Mathematics II - RemovedMd TareqBelum ada peringkat

- STSnewDokumen96 halamanSTSnewPatryk MartyniakBelum ada peringkat

- Probability & Random Process: FormulasDokumen10 halamanProbability & Random Process: FormulasSree RethanyaBelum ada peringkat

- Chapter 3Dokumen27 halamanChapter 3KamiBelum ada peringkat

- Chapter 0Dokumen13 halamanChapter 0nargizireBelum ada peringkat

- STAT 340/CS 437 PROBLEM SOLUTIONS UNDER 40 CHARACTERSDokumen66 halamanSTAT 340/CS 437 PROBLEM SOLUTIONS UNDER 40 CHARACTERSChristian DiazBelum ada peringkat

- Random Vectors: An Overview: Master INVESTMAT 2018-2019 Unit 2Dokumen40 halamanRandom Vectors: An Overview: Master INVESTMAT 2018-2019 Unit 2Ainhoa AzorinBelum ada peringkat

- Lecture 20Dokumen5 halamanLecture 20Ritik KumarBelum ada peringkat

- Engineering Probability and Statistics Statistics: Mathematical ExpectationDokumen18 halamanEngineering Probability and Statistics Statistics: Mathematical ExpectationDinah Jane MartinezBelum ada peringkat

- CSE 383M Midterm Exam Solution AnalysisDokumen5 halamanCSE 383M Midterm Exam Solution AnalysisMarabatalha McBelum ada peringkat

- XSTKE Chapter 2Dokumen18 halamanXSTKE Chapter 2K60 Đỗ Khánh NgânBelum ada peringkat

- Chapter 5Dokumen21 halamanChapter 5ashytendaiBelum ada peringkat

- 2021 - Week - 3 - Ch.2 Random ProcessDokumen11 halaman2021 - Week - 3 - Ch.2 Random ProcessAdibBelum ada peringkat

- 8 A. K. MajeeDokumen13 halaman8 A. K. MajeetarungajjuwaliaBelum ada peringkat

- 4mmpdensityfunct AnnotatedDokumen9 halaman4mmpdensityfunct AnnotatedAntal TóthBelum ada peringkat

- Introduction To Mathematics of Finance: Module III (Probability Theory) Session 14Dokumen23 halamanIntroduction To Mathematics of Finance: Module III (Probability Theory) Session 14Mehroze ElahiBelum ada peringkat

- 8mmpjoint AnnotatedDokumen25 halaman8mmpjoint AnnotatedAntal TóthBelum ada peringkat

- UntitledDokumen17 halamanUntitledSITHESWARAN SELVAMBelum ada peringkat

- Mathematical Statistics (MA212M) : Lecture SlidesDokumen8 halamanMathematical Statistics (MA212M) : Lecture SlidesakshayBelum ada peringkat

- Problem Solving II: Experimental Methods: 1 Basic ProbabilityDokumen14 halamanProblem Solving II: Experimental Methods: 1 Basic ProbabilityTest EmailBelum ada peringkat

- Chapitre 2Dokumen6 halamanChapitre 2chihabhliwaBelum ada peringkat

- Discrete, Continuous and Mixed Random VariablesDokumen9 halamanDiscrete, Continuous and Mixed Random VariablesIrma DenaBelum ada peringkat

- Random Variable Modified PDFDokumen19 halamanRandom Variable Modified PDFIMdad HaqueBelum ada peringkat

- Parameter EstimationDokumen34 halamanParameter EstimationJose Leonardo Simancas GarciaBelum ada peringkat

- CT2ADokumen5 halamanCT2ABugsBelum ada peringkat

- HW1: Continuous Random Variables (1) - SolutionsDokumen6 halamanHW1: Continuous Random Variables (1) - SolutionsKarimaBelum ada peringkat

- BayesianDokumen26 halamanBayesiantwqtwtw6Belum ada peringkat

- 02-Random VariablesDokumen51 halaman02-Random VariablesGetahun Shanko KefeniBelum ada peringkat

- QueueingPart1 Rev5 WinDokumen83 halamanQueueingPart1 Rev5 WinBini YamBelum ada peringkat

- Probability and StatisticsDokumen20 halamanProbability and StatisticsamolaaudiBelum ada peringkat

- Lec 07Dokumen6 halamanLec 07Sai Vikyath KomatireddyBelum ada peringkat

- Lecture 7Dokumen6 halamanLecture 7Agha Zeeshan Khan SoomroBelum ada peringkat

- Convergence Notes: Random Samples and StatisticsDokumen12 halamanConvergence Notes: Random Samples and StatisticsVishal SharmaBelum ada peringkat

- Chapter IIDokumen62 halamanChapter IIKamalpreet SinghBelum ada peringkat

- Business Stat & Emetrics101Dokumen38 halamanBusiness Stat & Emetrics101kasimBelum ada peringkat

- 18.650 Statistics For ApplicationsDokumen15 halaman18.650 Statistics For ApplicationsbobBelum ada peringkat

- QM Notes: The Wave FunctionDokumen11 halamanQM Notes: The Wave Functionmiyuki shiroganeBelum ada peringkat

- Formula PDFDokumen7 halamanFormula PDFPramit BhattacharyaBelum ada peringkat

- SSP4SE AppaDokumen10 halamanSSP4SE AppaÖzkan KaleBelum ada peringkat

- Probability Concepts in SimulationDokumen8 halamanProbability Concepts in SimulationHussein Turi HtgBelum ada peringkat

- Objective Fact SheetDokumen6 halamanObjective Fact SheetspellbindguyBelum ada peringkat

- Prefab House ProfileDokumen25 halamanPrefab House ProfilespellbindguyBelum ada peringkat

- Ultimate Guide To The PTE Academic SampleDokumen15 halamanUltimate Guide To The PTE Academic SampleRaghunath Reddy61% (38)

- 2008 AugustDokumen12 halaman2008 AugustspellbindguyBelum ada peringkat

- Ielts 42 Topics For Speaking Part 1Dokumen32 halamanIelts 42 Topics For Speaking Part 1Zaryab Nisar100% (1)

- Digital Comms Ch 5 OverviewDokumen24 halamanDigital Comms Ch 5 OverviewspellbindguyBelum ada peringkat

- Structure of School-ModelDokumen1 halamanStructure of School-ModelspellbindguyBelum ada peringkat

- Dinesh Jee PlanDokumen1 halamanDinesh Jee PlanspellbindguyBelum ada peringkat

- A2 Ket Vocabulary List PDFDokumen33 halamanA2 Ket Vocabulary List PDFAdriana BialisBelum ada peringkat

- 20171005011Dokumen1 halaman20171005011spellbindguyBelum ada peringkat

- Originally Posted byDokumen2 halamanOriginally Posted byspellbindguyBelum ada peringkat

- For Those Who Are Struggling With CDRDokumen2 halamanFor Those Who Are Struggling With CDRspellbindguyBelum ada peringkat

- Prefab School Cost EstimateDokumen1 halamanPrefab School Cost EstimatespellbindguyBelum ada peringkat

- Detailed Specification/ Estimate and Costing: Prefab House Nepal Pvt. LTDDokumen1 halamanDetailed Specification/ Estimate and Costing: Prefab House Nepal Pvt. LTDspellbindguyBelum ada peringkat

- Error Coding: 18-849b Dependable Embedded Systems Charles P. Shelton February 9, 1999Dokumen15 halamanError Coding: 18-849b Dependable Embedded Systems Charles P. Shelton February 9, 1999spellbindguyBelum ada peringkat

- ECEN 5682 Theory and Practice of Error Control CodesDokumen56 halamanECEN 5682 Theory and Practice of Error Control CodesspellbindguyBelum ada peringkat

- Salary CitizenDokumen5 halamanSalary CitizenspellbindguyBelum ada peringkat

- O - 3S XDC.T LCL Is A &/0/) IJ - :LDokumen4 halamanO - 3S XDC.T LCL Is A &/0/) IJ - :LspellbindguyBelum ada peringkat

- Salary LettersDokumen4 halamanSalary LettersspellbindguyBelum ada peringkat

- Socio-economic impacts of public land agroforestryDokumen75 halamanSocio-economic impacts of public land agroforestryspellbindguyBelum ada peringkat

- Clear Air Cargo Customs MontserratDokumen4 halamanClear Air Cargo Customs MontserratspellbindguyBelum ada peringkat

- Housing Tender for 2 Bed 4 Person HomeDokumen149 halamanHousing Tender for 2 Bed 4 Person Homefaiqkhoso89% (9)

- Earthquake damage details letterDokumen1 halamanEarthquake damage details letterspellbindguyBelum ada peringkat

- Concept Note Nepal PanaromicDokumen20 halamanConcept Note Nepal PanaromicspellbindguyBelum ada peringkat

- Hotel Asset Management - Pricipals & PracticesDokumen30 halamanHotel Asset Management - Pricipals & PracticesTrungHa NgoBelum ada peringkat

- Proposal TemplateDokumen15 halamanProposal TemplateFaaiz ShabbirBelum ada peringkat

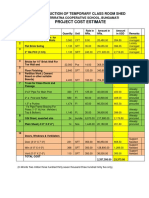

- Construction of Temporary Class Room ShedDokumen2 halamanConstruction of Temporary Class Room ShedspellbindguyBelum ada peringkat

- ContentsDokumen7 halamanContentsspellbindguyBelum ada peringkat

- AWFP Livestock Rehabilitation ProjectDokumen12 halamanAWFP Livestock Rehabilitation ProjectkopljanikBelum ada peringkat

- Propagating Trees and Fruit Trees: Sonny V. Matias TLE - EA - TeacherDokumen20 halamanPropagating Trees and Fruit Trees: Sonny V. Matias TLE - EA - TeacherSonny MatiasBelum ada peringkat

- Impact of Social Media in Tourism MarketingDokumen16 halamanImpact of Social Media in Tourism MarketingvidhyabalajiBelum ada peringkat

- Voice of The RainDokumen4 halamanVoice of The RainShriya BharadwajBelum ada peringkat

- Object Oriented Assignment GuideDokumen10 halamanObject Oriented Assignment GuideThiviyaa DarshiniBelum ada peringkat

- SWR SRB Product SheetDokumen2 halamanSWR SRB Product SheetCarlo AguiluzBelum ada peringkat

- Motenergy Me1507 Technical DrawingDokumen1 halamanMotenergy Me1507 Technical DrawingHilioBelum ada peringkat

- Trigonometry Ted Sundstrom and Steven SchlickerDokumen430 halamanTrigonometry Ted Sundstrom and Steven SchlickerhibiskusologjiaBelum ada peringkat

- Learning OrganizationDokumen104 halamanLearning Organizationanandita28100% (2)

- Probability Problems With A Standard Deck of 52 CardsByLeonardoDVillamilDokumen5 halamanProbability Problems With A Standard Deck of 52 CardsByLeonardoDVillamilthermopolis3012Belum ada peringkat

- E F Schumacher - Small Is BeautifulDokumen552 halamanE F Schumacher - Small Is BeautifulUlrichmargaritaBelum ada peringkat

- Assessment of Knowledge, Attitude Andpractice Toward Sexually Transmitteddiseases in Boditi High School StudentsDokumen56 halamanAssessment of Knowledge, Attitude Andpractice Toward Sexually Transmitteddiseases in Boditi High School StudentsMinlik-alew Dejenie88% (8)

- 103EXP3 SpectrophotometerDokumen5 halaman103EXP3 SpectrophotometeralperlengerBelum ada peringkat

- Test Bank For Environmental Science For A Changing World Canadian 1St Edition by Branfireun Karr Interlandi Houtman Full Chapter PDFDokumen36 halamanTest Bank For Environmental Science For A Changing World Canadian 1St Edition by Branfireun Karr Interlandi Houtman Full Chapter PDFelizabeth.martin408100% (16)

- Welcome To Word GAN: Write Eloquently, With A Little HelpDokumen8 halamanWelcome To Word GAN: Write Eloquently, With A Little HelpAkbar MaulanaBelum ada peringkat

- Abdul Azim Resume NewDokumen9 halamanAbdul Azim Resume NewSayed WafiBelum ada peringkat

- FeminismDokumen8 halamanFeminismismailjuttBelum ada peringkat

- Oracle Database Utilities OverviewDokumen6 halamanOracle Database Utilities OverviewraajiBelum ada peringkat

- Sfnhs Form 138 & 137 No LinkDokumen9 halamanSfnhs Form 138 & 137 No LinkZaldy TabugocaBelum ada peringkat

- Beyond Firo-B-Three New Theory-Derived Measures-Element B: Behavior, Element F: Feelings, Element S: SelfDokumen23 halamanBeyond Firo-B-Three New Theory-Derived Measures-Element B: Behavior, Element F: Feelings, Element S: SelfMexico BallBelum ada peringkat

- Scheduling BODS Jobs Sequentially and ConditionDokumen10 halamanScheduling BODS Jobs Sequentially and ConditionwicvalBelum ada peringkat

- Jesd51 13Dokumen14 halamanJesd51 13truva_kissBelum ada peringkat

- SPM Literature in English Tips + AdviseDokumen2 halamanSPM Literature in English Tips + AdviseJessica NgBelum ada peringkat

- Pagdaragdag (Adding) NG Bilang Na May 2-3 Digit Na Bilang Na May Multiples NG Sandaanan Antas 1Dokumen5 halamanPagdaragdag (Adding) NG Bilang Na May 2-3 Digit Na Bilang Na May Multiples NG Sandaanan Antas 1Teresita Andaleon TolentinoBelum ada peringkat

- A105972 PDFDokumen42 halamanA105972 PDFKelvin XuBelum ada peringkat

- Background and Introduction of The ProblemDokumen48 halamanBackground and Introduction of The ProblemElizebethBelum ada peringkat

- Chapter 1Dokumen9 halamanChapter 1Ibrahim A. MistrahBelum ada peringkat

- Installing OpenSceneGraphDokumen9 halamanInstalling OpenSceneGraphfer89chopBelum ada peringkat

- Wjec A Level Maths SpecificationDokumen50 halamanWjec A Level Maths SpecificationastargroupBelum ada peringkat

- What Is A Political SubjectDokumen7 halamanWhat Is A Political SubjectlukaBelum ada peringkat

- Galletto 1250 User GuideDokumen9 halamanGalletto 1250 User Guidesimcsimc1Belum ada peringkat