Anda mungkin juga menyukai

- Prospect Theory and Stock Market PremiumDokumen6 halamanProspect Theory and Stock Market PremiumromanaBelum ada peringkat

- STI - Daily PricesDokumen44 halamanSTI - Daily PricesromanaBelum ada peringkat

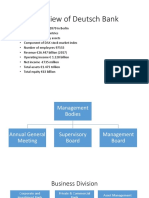

- Overview of Deutsch BankDokumen9 halamanOverview of Deutsch BankromanaBelum ada peringkat

- Deutsch BankDokumen1 halamanDeutsch BankromanaBelum ada peringkat

- Noble GroupDokumen2 halamanNoble GroupromanaBelum ada peringkat

- A Case Study Groupe Ariel SDokumen1 halamanA Case Study Groupe Ariel SromanaBelum ada peringkat

- Yield CurveDokumen7 halamanYield CurveromanaBelum ada peringkat

- Internship Report DraftDokumen13 halamanInternship Report DraftromanaBelum ada peringkat

- Noble GroupDokumen3 halamanNoble GroupromanaBelum ada peringkat

- Hermalin 2004Dokumen85 halamanHermalin 2004romanaBelum ada peringkat

- ModelingDokumen41 halamanModelingromanaBelum ada peringkat

- Ch-01 (English-2014) Final DraftDokumen15 halamanCh-01 (English-2014) Final DraftromanaBelum ada peringkat

- Financial ModelingDokumen4 halamanFinancial ModelingromanaBelum ada peringkat

- AssignmentDokumen11 halamanAssignmentromanaBelum ada peringkat

- Savings (In Billion TK.)Dokumen4 halamanSavings (In Billion TK.)romanaBelum ada peringkat

- Format of Internship ReportDokumen2 halamanFormat of Internship ReportromanaBelum ada peringkat

- ModelingDokumen41 halamanModelingromanaBelum ada peringkat

- Appendix 1.1: Macro-Economic Indicator: 1993-94-2004-05: ConsumptionDokumen52 halamanAppendix 1.1: Macro-Economic Indicator: 1993-94-2004-05: ConsumptionromanaBelum ada peringkat

- Budget Deficits and Inflation: Evidence From Turkey: Vietnam Khieu Van HoangDokumen1 halamanBudget Deficits and Inflation: Evidence From Turkey: Vietnam Khieu Van HoangromanaBelum ada peringkat

- Bangladeshi FoodDokumen1 halamanBangladeshi FoodromanaBelum ada peringkat

- Data SetDokumen8 halamanData SetromanaBelum ada peringkat

- Appendix 2008Dokumen53 halamanAppendix 2008romanaBelum ada peringkat

- JKDokumen15 halamanJKromanaBelum ada peringkat

- Presentation On: Comparison Between Islamic Banks and Conventional BanksDokumen11 halamanPresentation On: Comparison Between Islamic Banks and Conventional BanksromanaBelum ada peringkat

- Producing B2B Customer Case Studies IBeam MarketingDokumen16 halamanProducing B2B Customer Case Studies IBeam MarketingromanaBelum ada peringkat

- Country Report BangladeshDokumen74 halamanCountry Report BangladeshNahid Ali Mosleh JituBelum ada peringkat

- We Have Visited A Very Beautiful Hotel inDokumen16 halamanWe Have Visited A Very Beautiful Hotel inFarhana RomanaBelum ada peringkat

- Havard RefrencingDokumen18 halamanHavard RefrencingNatalieTanBelum ada peringkat

- One of The Luxurious Hotel in CoxDokumen13 halamanOne of The Luxurious Hotel in CoxromanaBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

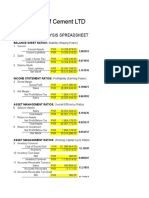

- Maple Leaf CementDokumen2 halamanMaple Leaf CementChampyBelum ada peringkat

- GST in India - An IntroductionDokumen24 halamanGST in India - An IntroductionMehak KaushikkBelum ada peringkat

- Estate and Donor Rrs and RamoDokumen12 halamanEstate and Donor Rrs and Ramocmv mendozaBelum ada peringkat

- Adopt-A-School Program Kit 2019Dokumen30 halamanAdopt-A-School Program Kit 2019Winny FelipeBelum ada peringkat

- Tds On Provison of Expenses (Tax Gls Open For Direct Manual Posting On 17.04.23 & 18.04.23 Only by Corporate Office) Urgent & Statuary ComplianceDokumen1 halamanTds On Provison of Expenses (Tax Gls Open For Direct Manual Posting On 17.04.23 & 18.04.23 Only by Corporate Office) Urgent & Statuary ComplianceArvind Kumar GuptaBelum ada peringkat

- UP vs. City Treasurer of Quezon City, GR No. 214044, 19 Jun 2019Dokumen2 halamanUP vs. City Treasurer of Quezon City, GR No. 214044, 19 Jun 2019Bernalyn Domingo AlcanarBelum ada peringkat

- STD Viii Maths Sample Paper - 2023-24Dokumen6 halamanSTD Viii Maths Sample Paper - 2023-24Monalisa PattnaikBelum ada peringkat

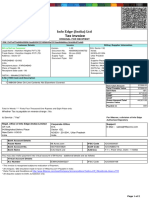

- Tax Invoice: Address: B-315, Shree Nand Dham, Sector-11, Plot.59, CBD Belapur, Navi Mumbai - 400614, MaharashtraDokumen1 halamanTax Invoice: Address: B-315, Shree Nand Dham, Sector-11, Plot.59, CBD Belapur, Navi Mumbai - 400614, MaharashtraSHANTANU PATHAKBelum ada peringkat

- Lease Deed: Ara Law Standard TemplateDokumen24 halamanLease Deed: Ara Law Standard TemplateAmit Kumar MauryaBelum ada peringkat

- Crossword MoneyDokumen3 halamanCrossword MoneyÁgnes JassóBelum ada peringkat

- SRC Income Tax Drop Off FormDokumen2 halamanSRC Income Tax Drop Off FormArvind MishraBelum ada peringkat

- Resume Lama AngahDokumen7 halamanResume Lama AngahFasiha MarkhadiBelum ada peringkat

- SG 2Dokumen29 halamanSG 2creatine2Belum ada peringkat

- March BIR RulingsDokumen13 halamanMarch BIR Rulingscarlee014Belum ada peringkat

- Declaration en Douane: Sender Customs Reference (If Any)Dokumen1 halamanDeclaration en Douane: Sender Customs Reference (If Any)NUR SAIDBelum ada peringkat

- 3.09 Set 3 Mock Exam ReaDokumen5 halaman3.09 Set 3 Mock Exam Reabhobot riveraBelum ada peringkat

- Tax Invoice: Created by Https://bizanalyst - inDokumen1 halamanTax Invoice: Created by Https://bizanalyst - inSavera DixitBelum ada peringkat

- Step 6 - ConfirmationDokumen2 halamanStep 6 - ConfirmationTori SmallBelum ada peringkat

- Custom Declaration: (Postal Administration)Dokumen6 halamanCustom Declaration: (Postal Administration)Malau JuanBelum ada peringkat

- Accountancy Mock Pre Board XIIDokumen12 halamanAccountancy Mock Pre Board XIIAmanbir SinghBelum ada peringkat

- Requisites of Valid AssessmentDokumen63 halamanRequisites of Valid AssessmentHazel Reyes-Alcantara100% (2)

- Manila Race Horse Association Inc., vs. Dela Fuente, 88 Phil 60Dokumen3 halamanManila Race Horse Association Inc., vs. Dela Fuente, 88 Phil 60MonikkaBelum ada peringkat

- 99 BillDokumen2 halaman99 BillLive lifeBelum ada peringkat

- Narrative Report - AdrianDokumen8 halamanNarrative Report - AdrianTimpug Crystal JeanBelum ada peringkat

- Prospectus Mod en YQFFpDokumen421 halamanProspectus Mod en YQFFpSalvator LevisBelum ada peringkat

- Professional Indemnity Zurich PolicyDokumen16 halamanProfessional Indemnity Zurich Policykalih krisnareindraBelum ada peringkat

- Consti ProjectDokumen8 halamanConsti ProjectShivansh PariharBelum ada peringkat

- IFM TB ch16Dokumen9 halamanIFM TB ch16Faizan Ch100% (1)

- Oregon Urban Renewal HistoryDokumen70 halamanOregon Urban Renewal Historyনূরুন্নাহার চাঁদনীBelum ada peringkat

- Chapter No.51psDokumen12 halamanChapter No.51psKamal SinghBelum ada peringkat