Anda mungkin juga menyukai

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- Branding Proposal SummaryDokumen3 halamanBranding Proposal SummaryAna Ckala33% (3)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Mastering The Covered Call FinalDokumen65 halamanMastering The Covered Call Finaljenna100% (1)

- At - (14) Internal ControlDokumen13 halamanAt - (14) Internal ControlLorena Joy Aggabao100% (2)

- Strength and WeaknessesDokumen6 halamanStrength and WeaknessesylevolBelum ada peringkat

- Vintage Boutique Business PlanDokumen12 halamanVintage Boutique Business PlanKirubashini S TTGI190112100% (2)

- Paper - 1 - MARK SCHEME and EXAMINER COMMENTS - SLDokumen44 halamanPaper - 1 - MARK SCHEME and EXAMINER COMMENTS - SLlarry wangBelum ada peringkat

- Province of Camarines Sur vs. Bodega Glassware, 821 SCRA 295, March 22, 2017Dokumen22 halamanProvince of Camarines Sur vs. Bodega Glassware, 821 SCRA 295, March 22, 2017Kath OBelum ada peringkat

- F-Change: A Concise Review of Medical Negligence and Board AccountabilityDokumen21 halamanF-Change: A Concise Review of Medical Negligence and Board AccountabilityKath OBelum ada peringkat

- PesoNet InstaPay FAQsDokumen4 halamanPesoNet InstaPay FAQsTom SBelum ada peringkat

- Notes - Salvacion CaseDokumen3 halamanNotes - Salvacion CaseKath OBelum ada peringkat

- Province of Camarines Sur vs. Bodega Glassware, 821 SCRA 295, March 22, 2017Dokumen22 halamanProvince of Camarines Sur vs. Bodega Glassware, 821 SCRA 295, March 22, 2017Kath OBelum ada peringkat

- Republic vs. Guzman, 326 SCRA 90, February 18, 2000Dokumen10 halamanRepublic vs. Guzman, 326 SCRA 90, February 18, 2000Kath OBelum ada peringkat

- Republic vs. CuetoDokumen18 halamanRepublic vs. CuetoCA DTBelum ada peringkat

- Republic vs. CuetoDokumen18 halamanRepublic vs. CuetoCA DTBelum ada peringkat

- Republic vs. Guzman, 326 SCRA 90, February 18, 2000Dokumen10 halamanRepublic vs. Guzman, 326 SCRA 90, February 18, 2000Kath OBelum ada peringkat

- Gonzales vs. Court of Appeals, 358 SCRA 598, June 18, 2001Dokumen12 halamanGonzales vs. Court of Appeals, 358 SCRA 598, June 18, 2001Kath OBelum ada peringkat

- Eduarte vs. Court of Appeals, 253 SCRA 391, February 09, 1996Dokumen15 halamanEduarte vs. Court of Appeals, 253 SCRA 391, February 09, 1996Kath OBelum ada peringkat

- Heirs of Jose Mariano and Helen S. Mariano vs. City of Naga, 858 SCRA 179, March 12, 2018Dokumen55 halamanHeirs of Jose Mariano and Helen S. Mariano vs. City of Naga, 858 SCRA 179, March 12, 2018Kath OBelum ada peringkat

- Imperial vs. Court of Appeals, 316 SCRA 393, October 08, 1999Dokumen15 halamanImperial vs. Court of Appeals, 316 SCRA 393, October 08, 1999Kath OBelum ada peringkat

- Gonzales vs. Court of Appeals, 358 SCRA 598, June 18, 2001Dokumen12 halamanGonzales vs. Court of Appeals, 358 SCRA 598, June 18, 2001Kath OBelum ada peringkat

- Heirs of Jose Mariano and Helen S. Mariano vs. City of Naga, 858 SCRA 179, March 12, 2018Dokumen55 halamanHeirs of Jose Mariano and Helen S. Mariano vs. City of Naga, 858 SCRA 179, March 12, 2018Kath OBelum ada peringkat

- 9 Gestopa vs. Court of AppealsDokumen12 halaman9 Gestopa vs. Court of Appealsshlm bBelum ada peringkat

- 9 Gestopa vs. Court of AppealsDokumen12 halaman9 Gestopa vs. Court of Appealsshlm bBelum ada peringkat

- F3 Study NotesDokumen132 halamanF3 Study NotesKath OBelum ada peringkat

- Araullo vs. Aquino III, 749 SCRA 283, February 03, 2015Dokumen169 halamanAraullo vs. Aquino III, 749 SCRA 283, February 03, 2015Kath OBelum ada peringkat

- Auditing The Revenue Cycle: IT Auditing & Assurance, 2e, Hall & SingletonDokumen29 halamanAuditing The Revenue Cycle: IT Auditing & Assurance, 2e, Hall & SingletonKath OBelum ada peringkat

- Construction and Interpretation of The ConstitutionDokumen2 halamanConstruction and Interpretation of The ConstitutionKath OBelum ada peringkat

- The Senate I. Composition: He Intends To Return and Remain)Dokumen5 halamanThe Senate I. Composition: He Intends To Return and Remain)Kath OBelum ada peringkat

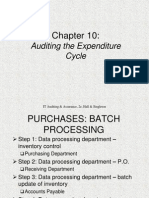

- Ch10 - Auditing Expenditure CycleDokumen21 halamanCh10 - Auditing Expenditure CycleRizka FurqorinaBelum ada peringkat

- Computer Security: Gremar T. CacachoDokumen5 halamanComputer Security: Gremar T. CacachoKath OBelum ada peringkat

- Statement of Financial Accounting Standards No. 2: Accounting For Research and Development CostsDokumen19 halamanStatement of Financial Accounting Standards No. 2: Accounting For Research and Development CostsKath OBelum ada peringkat

- SDLCDokumen1 halamanSDLCKath OBelum ada peringkat

- RR 10-2010 PDFDokumen4 halamanRR 10-2010 PDFKath OBelum ada peringkat

- Standard Costs and Variance AnalysisDokumen14 halamanStandard Costs and Variance Analysisboen jayme0% (1)

- Chapter 17 Audits ReportDokumen48 halamanChapter 17 Audits ReportKath OBelum ada peringkat

- GFGC - K. R. Pet - Preliminary Exam For Business Quiz - 2019Dokumen2 halamanGFGC - K. R. Pet - Preliminary Exam For Business Quiz - 2019Kiran A SBelum ada peringkat

- Summer Internship Report: at Edelweiss Financial ServicesDokumen7 halamanSummer Internship Report: at Edelweiss Financial ServicesJatin GuptaBelum ada peringkat

- Chapter 9-Cooperative StrategyDokumen36 halamanChapter 9-Cooperative StrategySomya TyagiBelum ada peringkat

- Project-Baumol Sales Revenue Maximization ModelDokumen10 halamanProject-Baumol Sales Revenue Maximization ModelSanjana BhabalBelum ada peringkat

- Assessment 4 Mark 1Dokumen29 halamanAssessment 4 Mark 1Devaky_Dealish_182Belum ada peringkat

- InvoiceDokumen1 halamanInvoicedhaval100% (1)

- Ai Trading ApplicationDokumen28 halamanAi Trading ApplicationAbhijeet PradhanBelum ada peringkat

- CCIDokumen35 halamanCCIAnonymous H1TW3YY51KBelum ada peringkat

- Daily Equity Market Report - 11.05.2022Dokumen1 halamanDaily Equity Market Report - 11.05.2022Fuaad DodooBelum ada peringkat

- CFAP 2 CL Summer 2023Dokumen3 halamanCFAP 2 CL Summer 2023HARIS MUKHTIARBelum ada peringkat

- Impact of Digital MarketingDokumen13 halamanImpact of Digital MarketingdheaBelum ada peringkat

- MP 14 Project Procurement Management 2020Dokumen68 halamanMP 14 Project Procurement Management 2020wulanpipi9Belum ada peringkat

- Chapter 17 Questions V1Dokumen4 halamanChapter 17 Questions V1lyellBelum ada peringkat

- STP For Rural MarketsDokumen16 halamanSTP For Rural MarketsDhivya Sermiah100% (1)

- Lesson 4 Evaluating A Firm S Internal CapabilitiesDokumen5 halamanLesson 4 Evaluating A Firm S Internal Capabilitiesintan renitaBelum ada peringkat

- Carrier: Delhivery: Deliver To FromDokumen1 halamanCarrier: Delhivery: Deliver To FromMohd ShanBelum ada peringkat

- LIBOR Role and Interest Rate SwapsDokumen2 halamanLIBOR Role and Interest Rate SwapsWOP INVESTBelum ada peringkat

- SSRN Id2206253Dokumen28 halamanSSRN Id2206253Alisha BhatnagarBelum ada peringkat

- CF Unit GuideDokumen3 halamanCF Unit GuideLinh Vo KhanhBelum ada peringkat

- Ready Willing and Able (Rwa) : Date: TODokumen3 halamanReady Willing and Able (Rwa) : Date: TONyangaya BaguéwamaBelum ada peringkat

- LinearEquationsInOneVariable InvestmentDokumen3 halamanLinearEquationsInOneVariable InvestmentKurt Byron AngBelum ada peringkat

- Econ 202 Interview Consumption Paper 1Dokumen3 halamanEcon 202 Interview Consumption Paper 1api-479844980Belum ada peringkat

- Ecojen Holdings LimitedDokumen1 halamanEcojen Holdings LimitedABOBO 254Belum ada peringkat

- Irrometer Ghana PDFDokumen17 halamanIrrometer Ghana PDFSarita JacksonBelum ada peringkat

- Introduction To Strategy Management External and Internal Analysis ST101X - W01 - C05Dokumen2 halamanIntroduction To Strategy Management External and Internal Analysis ST101X - W01 - C05Sanjay PawarBelum ada peringkat