Anda mungkin juga menyukai

- Pak-Qatar LNGDokumen14 halamanPak-Qatar LNGShahzaib KhanBelum ada peringkat

- Advanced Reservoir and Production Engineering for Coal Bed MethaneDari EverandAdvanced Reservoir and Production Engineering for Coal Bed MethanePenilaian: 1 dari 5 bintang1/5 (1)

- US LNG Sector Pause in US LNG Exports But Impact Will Come After 2030Dokumen37 halamanUS LNG Sector Pause in US LNG Exports But Impact Will Come After 2030zesmemBelum ada peringkat

- XojomixedawokukuvisavaneDokumen2 halamanXojomixedawokukuvisavanehamdi maidisonBelum ada peringkat

- Moving Natural Gas Stranded Reserves To Market in PolandDokumen7 halamanMoving Natural Gas Stranded Reserves To Market in PolandMarcelo Varejão CasarinBelum ada peringkat

- Investment in LNG Supply Chain Infrastructure Estimation: February 2018Dokumen15 halamanInvestment in LNG Supply Chain Infrastructure Estimation: February 2018mardiradBelum ada peringkat

- LNG Supply Chain Infrasructure ConfigurationDokumen15 halamanLNG Supply Chain Infrasructure ConfigurationpadangiringBelum ada peringkat

- Extended Abstract - Joana Antunes - MEGEDokumen10 halamanExtended Abstract - Joana Antunes - MEGEMarcosGonzalezBelum ada peringkat

- Blue Corridor NGV Rally 2013: LNG As Future Bunkering Fuel in EuropeDokumen14 halamanBlue Corridor NGV Rally 2013: LNG As Future Bunkering Fuel in EuropeBlue Corridor Natural Gas Vehicle Rally 2014Belum ada peringkat

- Commercial Use of STranded GasDokumen6 halamanCommercial Use of STranded GasaidanBelum ada peringkat

- Liquefied Natural Gas (LNG) Outlook in PakistanDokumen7 halamanLiquefied Natural Gas (LNG) Outlook in PakistanihllhmBelum ada peringkat

- LNG Terminals in IndiaDokumen20 halamanLNG Terminals in IndiaJyotishko BanerjeeBelum ada peringkat

- Pipeline - The Best & Most Efficient Mode of Transport of HydrocarbonDokumen3 halamanPipeline - The Best & Most Efficient Mode of Transport of HydrocarbonsdmaityBelum ada peringkat

- Assessment of Gas Supply SystemDokumen23 halamanAssessment of Gas Supply SystemfayzaBelum ada peringkat

- CNG Alternative To LNGDokumen7 halamanCNG Alternative To LNGSundar Kumar Vasantha GovindarajuluBelum ada peringkat

- CGD AssignmentDokumen14 halamanCGD AssignmentKuldeep ParmarBelum ada peringkat

- Floating Regasification Legal IsuesDokumen4 halamanFloating Regasification Legal IsuesAndres GarciaBelum ada peringkat

- CNG-An Alternative Transport For Natural GasDokumen10 halamanCNG-An Alternative Transport For Natural GasLuisBlandónBelum ada peringkat

- Design of A Typical LNG Plant For South-Pars Gas FieldDokumen4 halamanDesign of A Typical LNG Plant For South-Pars Gas FieldHassan HassanpourBelum ada peringkat

- 118WikipediaLNG PDFDokumen6 halaman118WikipediaLNG PDFanishBelum ada peringkat

- Fluxys TariffsDokumen17 halamanFluxys Tariffsjbalbas6307Belum ada peringkat

- Power OptionsDokumen25 halamanPower OptionsNasir AliBelum ada peringkat

- Infrastructure and Gas MonetisationDokumen22 halamanInfrastructure and Gas MonetisationRasholeenBelum ada peringkat

- Cygnus Energy LNG News Weekly 04th June 2021Dokumen20 halamanCygnus Energy LNG News Weekly 04th June 2021Sandesh Tukaram GhandatBelum ada peringkat

- (Polish Maritime Research) Development of New Technologies For Shipping Natural Gas by SeaDokumen9 halaman(Polish Maritime Research) Development of New Technologies For Shipping Natural Gas by SeafarshidianBelum ada peringkat

- Energy Law HungryDokumen9 halamanEnergy Law HungrySerhiiBelum ada peringkat

- Cyprus LNG Terminal EngDokumen12 halamanCyprus LNG Terminal Engapi-252576407100% (1)

- T1 Site - Economic Alternatives ReportDokumen8 halamanT1 Site - Economic Alternatives ReportMatthew KellyBelum ada peringkat

- (Published in Part - III Section 4 of The Gazette of India, Extraordinary) Tariff Authority For Major PortsDokumen43 halaman(Published in Part - III Section 4 of The Gazette of India, Extraordinary) Tariff Authority For Major PortsBalasubramanian SingaraveluBelum ada peringkat

- Overview LNG Central Java V.1.2.REV1Dokumen10 halamanOverview LNG Central Java V.1.2.REV1sigit l.prabowoBelum ada peringkat

- Energies: Workflow For Probabilistic Resource Estimation: Jafurah Basin Case Study (Saudi Arabia)Dokumen24 halamanEnergies: Workflow For Probabilistic Resource Estimation: Jafurah Basin Case Study (Saudi Arabia)SaidBelum ada peringkat

- Liquefied Natural Gas ChainDokumen11 halamanLiquefied Natural Gas Chaintsar mitchelBelum ada peringkat

- Petronet Corporate Presentation Jan11Dokumen31 halamanPetronet Corporate Presentation Jan11Ganesh DivekarBelum ada peringkat

- LNG - PVG NewsDokumen16 halamanLNG - PVG NewsAn Phạm ThànhBelum ada peringkat

- LNG Gas Station ProjectDokumen40 halamanLNG Gas Station ProjectMirzaMohtashimBelum ada peringkat

- Summary of Oil and Gas in IndonesiaDokumen5 halamanSummary of Oil and Gas in IndonesiasynolaBelum ada peringkat

- Brief On Thar Coal PotentialDokumen10 halamanBrief On Thar Coal PotentialKashifBelum ada peringkat

- LP PG Conversion To Thar CoalDokumen3 halamanLP PG Conversion To Thar CoalRaja Zeeshan100% (1)

- Presentation On LNG For Pip Seminar in Pso HouseDokumen26 halamanPresentation On LNG For Pip Seminar in Pso HouseRASHID AHMED SHAIKHBelum ada peringkat

- Bontang Future 3rd LNG-LPG - A Design Which Achieves Very High Levels of Flexibility, Safety and ReliabilityDokumen25 halamanBontang Future 3rd LNG-LPG - A Design Which Achieves Very High Levels of Flexibility, Safety and Reliabilitywebwormcpt100% (1)

- LNG Business Plan 20130220Dokumen50 halamanLNG Business Plan 20130220milham0975% (8)

- A New Consideration About Floating Storage and RegDokumen5 halamanA New Consideration About Floating Storage and RegerdemBelum ada peringkat

- A New Consideration About Floating Storage and Regasification Unit For Liquid Natural GasDokumen6 halamanA New Consideration About Floating Storage and Regasification Unit For Liquid Natural GasGak Ada NamaBelum ada peringkat

- FSRU Vs PipelineDokumen7 halamanFSRU Vs PipelineAnkurSrivastavBelum ada peringkat

- Press Release - Indian Gas Transmission Business: Sun Is Shining, The Weather Is SweetDokumen10 halamanPress Release - Indian Gas Transmission Business: Sun Is Shining, The Weather Is Sweetanzin_87Belum ada peringkat

- 2019 Olwatobi Ajagbe PublicationDokumen19 halaman2019 Olwatobi Ajagbe PublicationRonald Alex Chata YauriBelum ada peringkat

- Floating Transhipment SystemDokumen42 halamanFloating Transhipment SystemFnudarman FnudarmanBelum ada peringkat

- A New Business Approach To ConventionalDokumen42 halamanA New Business Approach To ConventionalAlberipaBelum ada peringkat

- Cygnus Energy LNG News Weekly 17th SEPTEMBER 2021Dokumen14 halamanCygnus Energy LNG News Weekly 17th SEPTEMBER 2021Sandesh Tukaram GhandatBelum ada peringkat

- Otc 20683 MS PDFDokumen11 halamanOtc 20683 MS PDFRamesh NairBelum ada peringkat

- 12 Mar 2019 162146807ULX2MK6XBriefsummaryofJaipurTRUDokumen3 halaman12 Mar 2019 162146807ULX2MK6XBriefsummaryofJaipurTRUrenger20150303Belum ada peringkat

- Cygnus Energy LNG News Weekly 29th October 2021Dokumen10 halamanCygnus Energy LNG News Weekly 29th October 2021Sandesh Tukaram GhandatBelum ada peringkat

- Cygnus Energy LNG News Weekly 29th October 2021Dokumen10 halamanCygnus Energy LNG News Weekly 29th October 2021Sandesh Tukaram GhandatBelum ada peringkat

- Gas ImportDokumen6 halamanGas ImportSundas ImranBelum ada peringkat

- Cygnus Energy LNG News Weekly 12th Feb 2021Dokumen19 halamanCygnus Energy LNG News Weekly 12th Feb 2021Sandesh Tukaram GhandatBelum ada peringkat

- Abbas - Bilgrami CNG Transportation Trans CanadaDokumen48 halamanAbbas - Bilgrami CNG Transportation Trans CanadaMustafa100% (1)

- Energy Science Engineering - 2019 - ShaoDokumen15 halamanEnergy Science Engineering - 2019 - ShaoYoon SDBelum ada peringkat

- LNG Regasification - Technology Evaluation and Cold Energy UtilisationDokumen9 halamanLNG Regasification - Technology Evaluation and Cold Energy UtilisationGSBelum ada peringkat

- Estimating Capital Cost of Small Scale LNG CarrierDokumen5 halamanEstimating Capital Cost of Small Scale LNG CarrierccelesteBelum ada peringkat

- CIPPDokumen3 halamanCIPPMirza Aatir SalmanBelum ada peringkat

- Book Review: The Year 2100 by Dr. Michio KakuDokumen2 halamanBook Review: The Year 2100 by Dr. Michio KakuMirza Aatir SalmanBelum ada peringkat

- Memo GM (HR) Format ABDokumen1 halamanMemo GM (HR) Format ABMirza Aatir SalmanBelum ada peringkat

- Commisioning of RLNG-II Contingency PlanDokumen5 halamanCommisioning of RLNG-II Contingency PlanMirza Aatir SalmanBelum ada peringkat

- KGM Working 18 01 12Dokumen3 halamanKGM Working 18 01 12Mirza Aatir SalmanBelum ada peringkat

- Report On Data CNGDokumen2 halamanReport On Data CNGMirza Aatir SalmanBelum ada peringkat

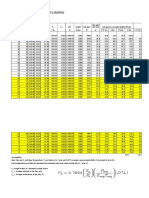

- Sui Southern Gas Company Limited Internal Audit Department: Avg Avg Avg 3 3Dokumen15 halamanSui Southern Gas Company Limited Internal Audit Department: Avg Avg Avg 3 3Mirza Aatir Salman0% (1)

- Explosive Rules 1940 PDFDokumen36 halamanExplosive Rules 1940 PDFalvinBelum ada peringkat

- Regas Rates Till Feb, 2017Dokumen1 halamanRegas Rates Till Feb, 2017Mirza Aatir SalmanBelum ada peringkat

- Confucius - QuotesDokumen13 halamanConfucius - QuotesAatir SalmanBelum ada peringkat

- Minimum Maximum LPG Energy Content (Btu/f)Dokumen5 halamanMinimum Maximum LPG Energy Content (Btu/f)Mirza Aatir SalmanBelum ada peringkat

- (If Known) : Appendix - "A"Dokumen21 halaman(If Known) : Appendix - "A"Mirza Aatir SalmanBelum ada peringkat

- Abraham Lincoln - QuotesDokumen8 halamanAbraham Lincoln - QuotesAatir SalmanBelum ada peringkat

- Annexures EA Tor 2-12-11Dokumen27 halamanAnnexures EA Tor 2-12-11Mirza Aatir SalmanBelum ada peringkat

- 10 Things Erp ImplementationDokumen4 halaman10 Things Erp ImplementationMirza Aatir SalmanBelum ada peringkat

- LPG Air Mix/Sng Plant Operations - Communique # 1 Functional Re-Organization at Head Office and Other Directives About State of Affairs at PlantsDokumen3 halamanLPG Air Mix/Sng Plant Operations - Communique # 1 Functional Re-Organization at Head Office and Other Directives About State of Affairs at PlantsMirza Aatir SalmanBelum ada peringkat

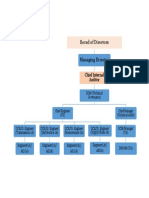

- Borad of Directors: Chief Internal AuditorDokumen1 halamanBorad of Directors: Chief Internal AuditorMirza Aatir SalmanBelum ada peringkat

- Concept Paper ETA IA 10 April 2015Dokumen4 halamanConcept Paper ETA IA 10 April 2015Mirza Aatir SalmanBelum ada peringkat

- Efrigeration IR Ryer: RD SeriesDokumen5 halamanEfrigeration IR Ryer: RD Seriesshanu vermaBelum ada peringkat

- Understanding Details of Cavitation:, IncludingDokumen10 halamanUnderstanding Details of Cavitation:, IncludingKriz Hor Jiunn ShyangBelum ada peringkat

- G 2-7 FF 265L DimensionalDokumen1 halamanG 2-7 FF 265L DimensionalHugo José Abreu de SouzaBelum ada peringkat

- Breathable Compressed Air BrochureDokumen11 halamanBreathable Compressed Air BrochuremuppetscrapBelum ada peringkat

- Series TD: Type TDL Type TDMDokumen16 halamanSeries TD: Type TDL Type TDMAhmadBelum ada peringkat

- Air VentsDokumen16 halamanAir VentsGuillermo CorderoBelum ada peringkat

- Thermodynamic Properties, Internal Energy, Specific Heat & Ideal Gas ModelsDokumen13 halamanThermodynamic Properties, Internal Energy, Specific Heat & Ideal Gas ModelsMel RSBelum ada peringkat

- How To Use This Catalog: Eearo-Orones 1soso0oDokumen46 halamanHow To Use This Catalog: Eearo-Orones 1soso0omk saravananBelum ada peringkat

- Refining Process of Crude Oil (PPT Details)Dokumen4 halamanRefining Process of Crude Oil (PPT Details)Angel Anne AlcantaraBelum ada peringkat

- 15ME53Dokumen2 halaman15ME53karl100% (1)

- Ledeen Actuator General Catalogue - Entire LineDokumen24 halamanLedeen Actuator General Catalogue - Entire LineJair LamasBelum ada peringkat

- (1976-1) Minimum Thickness of A Liquid Film Flowing Vertically Down A Solid SurfaceDokumen6 halaman(1976-1) Minimum Thickness of A Liquid Film Flowing Vertically Down A Solid SurfaceClarissa OlivierBelum ada peringkat

- Valve Sizing and SelectionDokumen7 halamanValve Sizing and SelectionDevendra BangarBelum ada peringkat

- SET 8 65-127 With AnswersDokumen4 halamanSET 8 65-127 With AnswersKian WinterskyBelum ada peringkat

- Open Channel Hydraulics Topic SyllabusDokumen1 halamanOpen Channel Hydraulics Topic SyllabusnidhalsaadaBelum ada peringkat

- Physics 101 Chapter 14 GasesDokumen35 halamanPhysics 101 Chapter 14 GasesAndrew GoolsbyBelum ada peringkat

- SMEA1303Dokumen11 halamanSMEA1303Sambhaji GhutugadeBelum ada peringkat

- As 3961-2005 The Storage and Handling of Liquefied Natural GasDokumen12 halamanAs 3961-2005 The Storage and Handling of Liquefied Natural GasSAI Global - APACBelum ada peringkat

- Datasheet ZE 150-500Dokumen1 halamanDatasheet ZE 150-500Rahmat Budi HartantoBelum ada peringkat

- Basic Hydraulic SystemDokumen72 halamanBasic Hydraulic SystemFahmy MohazBelum ada peringkat

- Coal Fired Power PlantDokumen23 halamanCoal Fired Power PlantLily CruzBelum ada peringkat

- Calorific Test of Gaseous FuelDokumen12 halamanCalorific Test of Gaseous FuelJohn Reantaso33% (3)

- Bingshan Screw CompressorDokumen36 halamanBingshan Screw CompressorGustavo Gramuglia Fávero100% (1)

- JPE CO2 Transportation by Pipeline Special IssueDokumen94 halamanJPE CO2 Transportation by Pipeline Special Issueargentino_ar01Belum ada peringkat

- AFT BrochureDokumen4 halamanAFT BrochurenkouhiBelum ada peringkat

- Pump 150918161223 Lva1 App6891 PDFDokumen325 halamanPump 150918161223 Lva1 App6891 PDFJohn RajBelum ada peringkat

- Operating Instructions Linear Flow Control LFC: DK S N P GR D GB F NL I E TR CZ PL RUS HDokumen4 halamanOperating Instructions Linear Flow Control LFC: DK S N P GR D GB F NL I E TR CZ PL RUS HmohamedwalyBelum ada peringkat

- Pressure Recovery in A Centrifugal Blower CasingDokumen7 halamanPressure Recovery in A Centrifugal Blower CasingBensinghdhasBelum ada peringkat

- Heat Exchanger Design - ProcessDokumen42 halamanHeat Exchanger Design - Processalokbdas100% (1)

- Agitator Power Requirement and Mixing Intensity CalculationDokumen27 halamanAgitator Power Requirement and Mixing Intensity Calculation황종서100% (1)