Anda mungkin juga menyukai

- Bookkeeping Video Training: (Handout)Dokumen22 halamanBookkeeping Video Training: (Handout)Yusuf RaharjaBelum ada peringkat

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDari Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsBelum ada peringkat

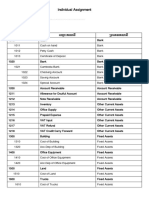

- Chart of AccountsDokumen11 halamanChart of AccountsTrisha Panaligan100% (1)

- Sample Chart of AccountsDokumen12 halamanSample Chart of AccountsjeffryBelum ada peringkat

- Standard Chart of AccountsDokumen6 halamanStandard Chart of AccountsAArif SShuvrooBelum ada peringkat

- Descriptions For NAHB COA AccountsDokumen67 halamanDescriptions For NAHB COA AccountsdumpBelum ada peringkat

- Chart of AccountDokumen5 halamanChart of AccountJamie ZuritaBelum ada peringkat

- Standard Chart of Accounts: Company NameDokumen52 halamanStandard Chart of Accounts: Company NameNiña Rica PunzalanBelum ada peringkat

- GL Ac ListDokumen6 halamanGL Ac ListshrirangkattiBelum ada peringkat

- Fin Acc Part 2Dokumen6 halamanFin Acc Part 2Jolina cunananBelum ada peringkat

- Peachtree Notes 2Dokumen28 halamanPeachtree Notes 2Tamiru Beyene100% (1)

- ANSWER KEY - CHARLOTTE SERVICES - Classification of Account and Balances of The AccountsDokumen11 halamanANSWER KEY - CHARLOTTE SERVICES - Classification of Account and Balances of The AccountsAnne MiguelBelum ada peringkat

- Hospital Chart of AccountsDokumen14 halamanHospital Chart of AccountsEphraim Boadu100% (1)

- Statement of Financial Position Notes Chapter 22Dokumen3 halamanStatement of Financial Position Notes Chapter 22tafadzwa mutandiroBelum ada peringkat

- Introduction To Fundamentals Of: Accountancy, Business and Management IIDokumen23 halamanIntroduction To Fundamentals Of: Accountancy, Business and Management IIAlbert Gaddiel CobicoBelum ada peringkat

- Budget Control Check: SAP FM BCS Business BlueprintDokumen17 halamanBudget Control Check: SAP FM BCS Business BlueprintÖmerFarukTekinBelum ada peringkat

- Asset AccountsDokumen7 halamanAsset AccountslaronrichelleeBelum ada peringkat

- Chart of Accounts: Account Type Income Tax LineDokumen4 halamanChart of Accounts: Account Type Income Tax LineNak VanBelum ada peringkat

- Grade 12 1st Quarter Fabm 2. Statement of Financial PositionDokumen5 halamanGrade 12 1st Quarter Fabm 2. Statement of Financial Positionjemima manzanoBelum ada peringkat

- Current AssetsDokumen1 halamanCurrent AssetsSara AlnahdiBelum ada peringkat

- Uniform System of Accounts Balance Sheet Accounts: Current AssetsDokumen153 halamanUniform System of Accounts Balance Sheet Accounts: Current AssetsUsama AhmadBelum ada peringkat

- Fundamentals of Accountancy, Business and Management 1Dokumen25 halamanFundamentals of Accountancy, Business and Management 1Worship Songs / Choreo / LyricsBelum ada peringkat

- Cooperative Chart of AccountsDokumen37 halamanCooperative Chart of AccountsGianena MarieBelum ada peringkat

- Company OverviewDokumen12 halamanCompany OverviewHaezel Santos VillanuevaBelum ada peringkat

- Book 1Dokumen10 halamanBook 1Majed AliBelum ada peringkat

- Balance Sheet Accounts CompressDokumen4 halamanBalance Sheet Accounts CompressBuhia, Alexandra DeniceBelum ada peringkat

- Individual AISDokumen3 halamanIndividual AISLe LaBelum ada peringkat

- 3660incom From BusinessDokumen19 halaman3660incom From BusinessWaqar AhmadBelum ada peringkat

- Master Chart of Account September 7 2018Dokumen340 halamanMaster Chart of Account September 7 2018Aman EdaoBelum ada peringkat

- LecDokumen12 halamanLecLorenaTuazonBelum ada peringkat

- Charts of AccountsDokumen7 halamanCharts of Accountszindabhaag100% (1)

- NGAS - NPOS - With AnswersDokumen10 halamanNGAS - NPOS - With AnswersDardar Alcantara100% (1)

- Accounting Terms Accounting: AssetsDokumen5 halamanAccounting Terms Accounting: AssetsediwowBelum ada peringkat

- Financials MF - TB & BSDokumen42 halamanFinancials MF - TB & BSAriel SpallettiBelum ada peringkat

- Fabm1 Module 7Dokumen26 halamanFabm1 Module 7Randy Magbudhi100% (10)

- Lesson 2.1Dokumen6 halamanLesson 2.1crisjay ramosBelum ada peringkat

- Uadc Financial Statements 2019. 123119.10PM - JonaDokumen263 halamanUadc Financial Statements 2019. 123119.10PM - JonaYameteKudasaiBelum ada peringkat

- CTAA 031 - 2023 Special DeductionsDokumen20 halamanCTAA 031 - 2023 Special DeductionsZwivhuya MaimelaBelum ada peringkat

- Account TitlesDokumen5 halamanAccount TitlesJosh BustamanteBelum ada peringkat

- SPECTRAN Corpo-LiquidationDokumen11 halamanSPECTRAN Corpo-LiquidationJhon RenomeronBelum ada peringkat

- FAR - Module 2 - The Accounting EquationDokumen5 halamanFAR - Module 2 - The Accounting EquationEva Katrina R. Lopez100% (1)

- CCPL BLDokumen14 halamanCCPL BLRana7540Belum ada peringkat

- Financial Accounting & Analysis AssignmentDokumen4 halamanFinancial Accounting & Analysis AssignmentDhanshree Thorat AmbavleBelum ada peringkat

- Hanad General Trading Financial Statements 2023Dokumen8 halamanHanad General Trading Financial Statements 2023Nyakwar Leoh NyabayaBelum ada peringkat

- Worktext Fabm1 Q4 W1-WokDokumen19 halamanWorktext Fabm1 Q4 W1-WokQuincy Lawrence DimaanoBelum ada peringkat

- 01 - Accounting For Trades and Other ReceivablesDokumen5 halaman01 - Accounting For Trades and Other ReceivablesCatherine CaleroBelum ada peringkat

- Entries On Construction in ProgressDokumen8 halamanEntries On Construction in ProgressRomyleen WennaBelum ada peringkat

- 17 Lecture 1 Bookkeeping and AccountingDokumen11 halaman17 Lecture 1 Bookkeeping and AccountingCrisceldette ApostolBelum ada peringkat

- Chapter 2 - HandoutsDokumen9 halamanChapter 2 - HandoutsKarysse Arielle Noel JalaoBelum ada peringkat

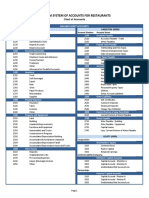

- Uniform System of Accounts Restaurant USARDokumen15 halamanUniform System of Accounts Restaurant USARHector RiveraBelum ada peringkat

- Contabilidad Gerencial Taller Individual N°3Dokumen4 halamanContabilidad Gerencial Taller Individual N°3Hernando JPBelum ada peringkat

- Chapter 4 Accounting Information SystemDokumen3 halamanChapter 4 Accounting Information SystemFlordeliza HalogBelum ada peringkat

- Business Ethics Reviewer 1Dokumen10 halamanBusiness Ethics Reviewer 1Marinette Valencia MedranoBelum ada peringkat

- Day Care Center - Chart of AccountsDokumen6 halamanDay Care Center - Chart of AccountsArif Masood100% (6)

- CH 4 (Income Statement)Dokumen40 halamanCH 4 (Income Statement)Study OuoBelum ada peringkat

- Myob 13-5-2022Dokumen3 halamanMyob 13-5-2022Mora MdlnBelum ada peringkat

- Basic Elements of AccountingDokumen19 halamanBasic Elements of AccountingMonique DanielleBelum ada peringkat

- Wa0000 PDFDokumen12 halamanWa0000 PDFsipheleleBelum ada peringkat

- Expenses 2 PDFDokumen2 halamanExpenses 2 PDFDumpp Acc.3Belum ada peringkat

- REGULATIONSDokumen4 halamanREGULATIONSMuhammad Ilyas ShafiqBelum ada peringkat

- 2017LHC3575Dokumen6 halaman2017LHC3575Muhammad Ilyas ShafiqBelum ada peringkat

- Procedure: Association Not For ProfitDokumen49 halamanProcedure: Association Not For ProfitWaqar MughalBelum ada peringkat

- Guide On Conversion of Status of Companies: Securities and Exchange Commission of PakistanDokumen16 halamanGuide On Conversion of Status of Companies: Securities and Exchange Commission of PakistanzuunaBelum ada peringkat

- Agreement TilesSupply 20150726Dokumen6 halamanAgreement TilesSupply 20150726Muhammad Ilyas ShafiqBelum ada peringkat

- Guideon Conversionof Stausof Companiesnov 222010Dokumen12 halamanGuideon Conversionof Stausof Companiesnov 222010Muhammad Ilyas ShafiqBelum ada peringkat

- Agreement TilesSupply 20150726Dokumen6 halamanAgreement TilesSupply 20150726Muhammad Ilyas ShafiqBelum ada peringkat

- Companies Act 2017Dokumen430 halamanCompanies Act 2017Abdul MuneemBelum ada peringkat

- Annual Report 2013Dokumen120 halamanAnnual Report 2013Muhammad Ilyas ShafiqBelum ada peringkat

- Pra 5%Dokumen2 halamanPra 5%Muhammad Ilyas ShafiqBelum ada peringkat

- Guide On Conversion of Status of Companies: Securities and Exchange Commission of PakistanDokumen16 halamanGuide On Conversion of Status of Companies: Securities and Exchange Commission of PakistanzuunaBelum ada peringkat

- W.P. 758 Vincraft Vs - FBR, Etc 1.6.2017 DBDokumen14 halamanW.P. 758 Vincraft Vs - FBR, Etc 1.6.2017 DBMuhammad Ilyas ShafiqBelum ada peringkat

- 2015 LHC 5713Dokumen11 halaman2015 LHC 5713Muhammad Ilyas ShafiqBelum ada peringkat

- Noon SML App GeneDokumen29 halamanNoon SML App GeneMuhammad Ilyas ShafiqBelum ada peringkat

- C A 876-879of2005 PDFDokumen79 halamanC A 876-879of2005 PDFMuhammad Ilyas ShafiqBelum ada peringkat

- 2011 PTD (Trib.) 936 PDFDokumen13 halaman2011 PTD (Trib.) 936 PDFMuhammad Ilyas ShafiqBelum ada peringkat

- C A 876-879of2005 PDFDokumen79 halamanC A 876-879of2005 PDFMuhammad Ilyas ShafiqBelum ada peringkat

- MCB ChallanDokumen4 halamanMCB ChallanMuhammad Ilyas Shafiq71% (7)

- Syllabus LLBDokumen26 halamanSyllabus LLBshahbaztahir92% (12)

- Deed of PartnershipDokumen5 halamanDeed of PartnershipMuhammad Ilyas ShafiqBelum ada peringkat

- HuddocDokumen15 halamanHuddocMuhammad Ilyas ShafiqBelum ada peringkat

- Cyprus QuestionDokumen9 halamanCyprus QuestionMuhammad Ilyas ShafiqBelum ada peringkat

- Adeyemi Adeola CV1 - 1620243247000Dokumen2 halamanAdeyemi Adeola CV1 - 1620243247000abrahamdavidchukwuma1Belum ada peringkat

- (Jefferies) 2-14 ChinaTheYearoftheRamDokumen158 halaman(Jefferies) 2-14 ChinaTheYearoftheRamNgô Xuân TùngBelum ada peringkat

- NO2 Kampung Kuak Hulu 33100 Pengkalan Hulu Perak: Abdul Arif Bin Mahamad HanafiahDokumen1 halamanNO2 Kampung Kuak Hulu 33100 Pengkalan Hulu Perak: Abdul Arif Bin Mahamad HanafiahMuhammad ikmail KhusaimiBelum ada peringkat

- Bill of Exchange 078Dokumen1 halamanBill of Exchange 078trung2iBelum ada peringkat

- Idea Cloud Kitchen ChainDokumen6 halamanIdea Cloud Kitchen ChainVAIBHAV WADHWABelum ada peringkat

- Steampunk Settlement: Cover Headline Here (Title Case)Dokumen16 halamanSteampunk Settlement: Cover Headline Here (Title Case)John DeeBelum ada peringkat

- Agreement 2006 Bank of AmericaDokumen19 halamanAgreement 2006 Bank of AmericaNora WellerBelum ada peringkat

- Notes On UlpDokumen10 halamanNotes On UlppatrixiaBelum ada peringkat

- Quiz Ibm 530 (Ans 13-18) ZammilDokumen5 halamanQuiz Ibm 530 (Ans 13-18) Zammilahmad zammilBelum ada peringkat

- Consumer Durables December 2023Dokumen33 halamanConsumer Durables December 2023raghunandhan.cvBelum ada peringkat

- E0079 Rewards and Recognition - DR ReddyDokumen88 halamanE0079 Rewards and Recognition - DR ReddywebstdsnrBelum ada peringkat

- Arnel SambajonDokumen2 halamanArnel SambajonAnonymous 1lYUUy5TBelum ada peringkat

- Forces of Excellence in Kanji S Business Excellence Model PDFDokumen15 halamanForces of Excellence in Kanji S Business Excellence Model PDFChar AzBelum ada peringkat

- JetBlue Airways Starting From Scratch Group 4Dokumen8 halamanJetBlue Airways Starting From Scratch Group 4Fadhila Nurfida HanifBelum ada peringkat

- New Employee Onboarding Process in An OrganizationDokumen3 halamanNew Employee Onboarding Process in An OrganizationNishan ShettyBelum ada peringkat

- 111 0404Dokumen36 halaman111 0404api-27548664Belum ada peringkat

- P&GDokumen10 halamanP&GSameed RiazBelum ada peringkat

- Cape Elizabeth School Board Response To Citizens ConcernsDokumen10 halamanCape Elizabeth School Board Response To Citizens ConcernsJocelyn Van SaunBelum ada peringkat

- SAD 5 Feasiblity Analysis and System ProposalDokumen10 halamanSAD 5 Feasiblity Analysis and System ProposalAakash1994sBelum ada peringkat

- Tata Consultancy Services Ltd. Company AnalysisDokumen70 halamanTata Consultancy Services Ltd. Company AnalysisPiyush ThakarBelum ada peringkat

- UNESCO Toolkit PDFs Guide 2CDokumen12 halamanUNESCO Toolkit PDFs Guide 2CBabak D.V. DaraniBelum ada peringkat

- 01 TFS PresentationDokumen23 halaman01 TFS PresentationShardul ManjrekarBelum ada peringkat

- Course Code: CET 408 Gths/Rs - 19 / 7604 Eighth Semester B. E. (Civil Engineering) ExaminationDokumen3 halamanCourse Code: CET 408 Gths/Rs - 19 / 7604 Eighth Semester B. E. (Civil Engineering) ExaminationRajput Ayush ThakurBelum ada peringkat

- Values and Mission of Coca ColaDokumen2 halamanValues and Mission of Coca ColaUjjwal AryalBelum ada peringkat

- What Is A Business Model?Dokumen9 halamanWhat Is A Business Model?Analyn SolitoBelum ada peringkat

- A Project Report On "Service Quality AND Customer Satisfaction" inDokumen65 halamanA Project Report On "Service Quality AND Customer Satisfaction" inswayam anandBelum ada peringkat

- Banking Awareness October Set 2Dokumen7 halamanBanking Awareness October Set 2Madhav MishraBelum ada peringkat

- Static FilesDokumen27 halamanStatic FilesMariano CarranzaBelum ada peringkat

- Black Money Act 2015Dokumen16 halamanBlack Money Act 2015Dharshini AravamudhanBelum ada peringkat

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyDari EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyBelum ada peringkat

- How to get US Bank Account for Non US ResidentDari EverandHow to get US Bank Account for Non US ResidentPenilaian: 5 dari 5 bintang5/5 (1)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyDari EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyPenilaian: 4 dari 5 bintang4/5 (52)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProDari EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProPenilaian: 4.5 dari 5 bintang4.5/5 (43)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsDari EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsBelum ada peringkat

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesDari EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesPenilaian: 4 dari 5 bintang4/5 (9)

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionDari EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionPenilaian: 5 dari 5 bintang5/5 (27)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderDari EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderBelum ada peringkat

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCDari EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCPenilaian: 4 dari 5 bintang4/5 (5)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDari EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesBelum ada peringkat

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationDari EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationBelum ada peringkat

- The Great Multinational Tax Rort: how we’re all being robbedDari EverandThe Great Multinational Tax Rort: how we’re all being robbedBelum ada peringkat

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012Dari EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012Belum ada peringkat

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessDari EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessPenilaian: 5 dari 5 bintang5/5 (5)

- The Hidden Wealth of Nations: The Scourge of Tax HavensDari EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensPenilaian: 4 dari 5 bintang4/5 (11)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipDari EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipBelum ada peringkat

- Bookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesDari EverandBookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesBelum ada peringkat

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingDari EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingPenilaian: 5 dari 5 bintang5/5 (3)

- Taxes Have Consequences: An Income Tax History of the United StatesDari EverandTaxes Have Consequences: An Income Tax History of the United StatesBelum ada peringkat

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionDari EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionBelum ada peringkat

- Decrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationDari EverandDecrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationBelum ada peringkat

- U.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadDari EverandU.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadBelum ada peringkat

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsDari EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsPenilaian: 3.5 dari 5 bintang3.5/5 (9)